October Budget predictions: What taxes could Labour increase?

With just a few weeks to go until the Government’s first Budget, the public is waiting to see how it follows through on its manifesto promises – and whether there will be any nasty surprises.

The party’s refusal to rule out several potential tax changes, plus Sir Keir Starmer’s stark warning that his party’s first Budget “is going to be painful”, means rumours are rife.

From increasing capital gains tax rates to targeting tax-free lump sums, Telegraph Money takes you through what Labour could have in store.

What will Labour do in the Budget?

Much of Labour’s plans are still relatively unknown, as the party has so far been tight-lipped on its tax plans.

Ministers have confirmed its manifesto pledge to help “working people”, and therefore ruling out hikes to income tax rates, National Insurance and VAT.

However, this doesn’t necessarily mean these taxes will be completely left alone, as the Government could tinker around the edges of its manifesto promises.

Here are some of the taxes that could be in Labour’s sights.

The nine taxes Labour could target

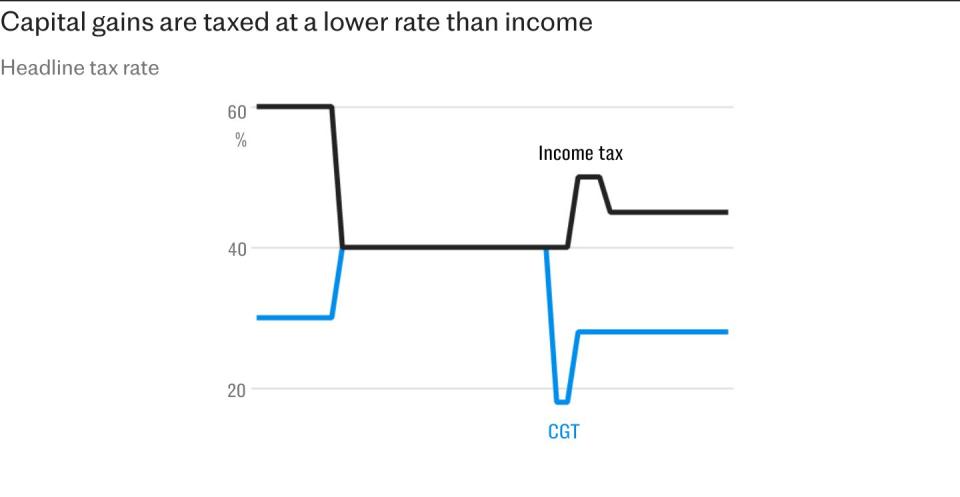

1. Capital gains tax

It’s looking increasingly likely that capital gains tax will be caught up in the crosshairs of Labour’s tax raises.

Sir Keir Starmer has ruled out charging capital gains on someone’s first home, which is exempt under the current system, but stopped short of extending that to any rises.

According to reports in The Times, the rate charged for higher-rate taxpayers selling a second home will remain at 24pc, but the 20pc tax when selling shares or other valuable assets is likely to rise by “several percentage points”.

It’s unclear whether the rate paid by basic-rate taxpayers, which is currently 10pc, would also be in line for an increase.

The Government could also choose to look at the current £3,000 threshold at which the tax becomes due. This has been reduced in successive tax years under the previous Conservative government, from £12,300 in 2022-23, and £6,000 in 2023-24.

Sarah Coles, of Hargreaves Lansdown, said: “Labour hasn’t ruled out raising capital gains tax. It would enable the Government to deliver on the promise not to raise taxes for ‘working people’, because it’s a tax on wealth. However, it’s a tough balancing act, because it doesn’t sit well with its plans to be a government that helps people create wealth. If they were to make changes, they’d have a wide range of options.”

The chart below shows how capital gains tax rates currently compare to income tax.

Chris Rudden, head of UK investment consultants at Moneyfarm, added: “Labour pledged that it wouldn’t go after income tax or National Insurance and I don’t think they would renege on that straight away. However, I have a sneaking suspicion that capital gains tax is not safe.

“However, the Treasury still hasn’t seen the full effect of the windfall that was created by Jeremy Hunt cutting the CGT allowance to £3,000. They might find that the increase in capital gains receipts will be plenty and so they don’t have to go after it further.

“In a world where it’s widely considered that the UK population doesn’t invest enough to support their future, putting a higher tax burden on investments puts a greater obstacle to getting people started.”

2. Inheritance tax

Possible changes could be in store for inheritance tax, as Ms Reeves is said to be considering a change to the headline rate or tax-free exemptions in plans first reported by the BBC.

Fears about the levy being targeted have been around for a while. Back in July, a leaked recording of a shadow frontbencher has raised fears that Labour could be planning a raid on family wealth after death. Darren Jones, the shadow chief secretary to the Treasury, told a public meeting in March that inheritance tax (IHT) could be used to “redistribute wealth” and address “intergenerational inequality”.

This has prompted concern that Labour could attack various reliefs that allow families to pay less inheritance tax.

Homeowners can pass on £500,000 – or £1m if they are a couple – as long as they leave their house to their children. Labour could choose to cut or lower this exemption, widening the scope of inheritance tax.

Alternatively Labour could attack various reliefs that allow people to give away their wealth earlier, without paying death duties.

Britain already has one of the highest inheritance tax rates in the OECD at 40pc.

If your estate is worth more £325,000 when you die, then your beneficiaries will pay this charge on everything above the threshold, called the nil-rate band. The tax-free exemption has been frozen at £325,000 since 2009, dragging thousands into the death duty net as house prices have soared.

According to official forecasts, the number of families paying the charge will hit nearly 44,000 a year by 2028-29, up from 33,000 this year. In total, almost 200,000 estates will pay the tax over the next five years.

3. Tax on pensions

Labour has so far failed to rule out potential changes to the 25pc tax-free lump sum, and is reportedly considering cutting the tax-free amount to £100,000, down from £268,275. This follows recommendations from think tanks to reduce the limit, which could raise around £2bn.

It’s not clear how this might work in practice, and some experts have raised the possibility that such a change may attract legal challenges.

Mike Ambery, of the pension firm Standard Life, said: “Operationally, it would be complicated. That’s because pension funds are normally written under trust and also you can’t really retrospectively make changes to benefits that people have already built up. It could be subject to a legal challenge.”

Charging inheritance tax on pensions is another option. Currently, pensions are not considered part of your estate when you die, meaning IHT is not due.

However, some fear that Labour might change this, which analysis shows could cost grieving families tens of thousands of pounds. It could also lower the maximum amount people can contribute to their pensions without losing tax relief, the so-called annual allowance.

Andrew Tully, of Nucleus Financial, added: “Labour appears to have ruled out any reintroduction of the lifetime allowance, at least in the short term, but they could consider changing the current very attractive rules on passing on pension wealth tax-efficiently to families. One way to do this would be to include pension wealth within the estate for IHT purposes.”

When it comes to the state pension, Labour has committed to maintaining the triple lock, ensuring the state pension will continue to increase by the highest of inflation, wages or 2.5pc. However, under current plans this would see it become taxable by 2028 as it will exceed the personal allowance, leaving some pensioners with a three-figure tax bill by the end of the current Parliament.

Labour has not revealed any plans to protect the state pension from tax. Currently, more than a million households rely solely on the state pension and benefits as their only income.

4. Employers National Insurance contributions

While Labour has said it’s not intending to raise National Insurance contributions (NICs) for “working people”, it has not ruled out a rise for employers.

Employers currently pay 13.8pc in NICs on employees’ salaries. If this was raised by one percentage point to 14.8pc, it would bring in an estimated extra £8.5bn a year.

Reeves could go further, though. It’s been suggested that employer NICs could also be introduced on the money contributed to staff pensions, which would generate an extra £17bn for the Treasury.

While workers wouldn’t pay these taxes, the consensus is that the extra costs would eventually be passed to staff in the form of lower pay and fewer job benefits, such as salary sacrifice schemes and above-statutory pension contributions.

5. Stamp duty

The tax due after the purchase of a property is set to increase from April, as Labour is reportedly set to lift the current Truss-era exemptions that have saved the average home buyer £2,500.

For those in England and Northern Ireland, currently, first-time buyers can claim stamp duty relief, which means paying 0pc in stamp duty on property values up to £425,000, with a 5pc charge kicking in on values between £425,001 to £625,000.

If the extra exemption is lifted in April, it would mean paying 5pc on the the portion of the property value between £300,001 and £500,000. First-time buyers purchasing properties valued higher than these upper limits cannot get the relief, and would have to pay home mover rates.

Home movers pay 0pc up to £250,000, 5pc on the value between £250,001 and £925,000, 10pc on £925,001 to £1.5m, and 12pc on the value over this. From April, an additional 2pc could be charged on the value between £125,001 and £250,000.

Those purchasing second homes or buy-to-let properties pay a 3pc surcharge on all of these rates.

6. Savings tax

Cuts to the Isa allowance and also the personal savings allowance are among the options open to Labour.

The Resolution Foundation, a think tank, has previously urged the Government to cap the amount that can be saved into an Isa at £100,000.

Savers can pay in £20,000 per year, but there is currently no limit on how much they can stash away over their lifetime. The Resolution Foundation argued this mainly benefits those with high levels of disposable income.

Returns on cash Isas do not trigger a tax bill, but tax can be owed on interest earned from ordinary savings accounts if it exceeded the personal savings allowance.

The allowance is £1,000 for basic-rate taxpayers and £500 for those in the higher-rate band. Additional-rate taxpayers get no allowance.

Yet frozen tax thresholds have dragged millions into higher tax brackets, slashing their personal saving allowance dramatically.

As savings rates have soared as high as 5pc, a higher-rate taxpayer now needs just £10,000 in savings to exceed their personal savings allowance.

As a result, people are expected to pay a record-breaking £10.3bn in tax on their savings in 2024-25, according to HM Revenue and Customs – up about £1bn since last year.

7. Council tax

Sir Keir Starmer has refused to rule out a potential council tax reform, leaving all options on the table for a future shake-up.

In a leaked recording, Darren Jones, shadow chief secretary to the Treasury, also told a constituency meeting that the bands were “out-of-date”, hinting at a tax raid on wealthy people’s homes.

The Fairer Share think tank has proposed replacing the current system with a “proportional” council tax.

Instead of bands, the bill would be a flat percentage, such as 0.5pc, of a property’s value and it would be uprated annually, to reflect changing values.

However, under this system, council tax bills would rise by an average of £1,230 for more than four million households in England, according to the Institute for Fiscal Studies (IFS) think tank.

Reevaluating bands could also be on the cards. In England, council tax bands are based on 1991 property values, despite house prices rising eightfold in some areas.

In Wales, Labour has already pledged to reevaluate council tax with higher bands and higher rates to address “property wealth” and “rebalance” the current system.

Re-evaluating the bands to current house prices would spark bills to rise in 119 of the 325 local authority areas in England, the IFS said.

The average household would see their tax bill rise by £82, but those in 32 local authorities would suffer increases of more than £100.

8. Alcohol duty

The Chancellor has not ruled out increasing tax on beer, wine and spirits, after being presented with forecasts that suggested an increase to alcohol duty could raise an extra £800m next year.

Alcohol duty is levied on all drinks that are more than 1.2pc ABV strength, either at the point of production or when they are imported into the UK.

It automatically rises every year in line with the Retail Price Index (RPI) measure of inflation, unless a decision is taken to freeze it.

The drinks industry says such a move would have a “catastrophic” impact on pubs.

It comes as a report by the Institute for Public Policy Research urged the Chancellor to raise taxes on unhealthy food, gambling, alcohol and tobacco, which could help curb the number of British workers currently signed off with long-term sickness.

9. Fuel duty

Motorists could be handed higher costs should Labour choose to target fuel duty in its Budget.

Fuel duty has been frozen since 2011-12, and the Conservative government cut the rate by a further 5p in 2022 as prices rocketed following the beginning of the war in Ukraine.

The RAC said that the 5p cut was likely to be scrapped, which is estimated to increase drivers’ costs of filling up their tanks by an average of £3.30.

The Government could increase the duty further.

What has Labour cut to make savings?

The Government has already announced changes to help fund its plans and plug the £22bn “hole”.

Winter fuel payments

In what was seen as bombshell announcement, Labour has said it will limit winter fuel payments to those on certain benefits. It means that around 90pc of British pensioners will now not qualify for this payment.

Only households with someone aged over state pension age, currently 66 years old, receiving pension credit, Universal Credit, Income Support, income-based Jobseeker’s Allowance and income-related Employment and Support Allowance will continue to receive winter fuel payments. The Chancellor said this will save £1.5bn annually.

Social care

In addition, Ms Reeves said she will not go ahead with the Conservatives’ plan for adult social care charging reforms. The proposed changes had been planned to cap individual personal care costs at £86,000.

It was also set to allow those with less than £100,000 in assets and savings to access state support for eligible social care costs. Currently only those with less than £23,250 are eligible. Ms Reeves said ending these reforms will save the Government £4bn by 2029-30.

Private school VAT

Labour has been very clear that it will remove the VAT and business rates exemption from private schools. It means 20pc in tax will become due on tuition and boarding fees.

It has said the change will come into effect from January 1 2025 and will apply to any fees paid in advance as of July 29, the day Ms Reeves announced the policy.

It is expected that most schools will pass the costs on to fee-payers, meaning some children could be withdrawn from school as families struggle with rising costs. An exodus of private school students could overwhelm local state schools.

Further, Ms Reeves has scrapped Tory plans for an Advanced British Standard qualification that was set to bring together A-levels and T-levels into a single qualification framework. Cancelling this reform will save £185m next year.

What has Labour promised to deliver?

Labour has said it will accept the independent Pay Review Body recommendations and increase public sector salaries by an average of 5.5pc. This will cost around £9bn a year.

Labour will seek to enhance job security by banning zero hours contracts and ending the practice of “fire and rehire”, while workers will get parental leave and statutory sick pay from day one of a new job.

Low earners will get a boost with minimum pay that is a “genuine living wage”, regardless of age.

Families will benefit from expanded childcare and free breakfast clubs in every primary school. Communities will regain control of their bus routes and first-time buyers will get more support to get on the housing ladder, Labour says.

The Government wants to also tighten energy market regulation, which its manifesto says will reduce bills and hold providers to account for wrongdoing.

It will also take aim at non-doms by abolishing the status “once and for all” – but perhaps in a more softened way than first planned.

The Tories scrapped non-doms’ special status in the Budget, but Labour had been intending to go one step further and close a “loophole” that allows non-doms to move their money into an offshore trust before the ban comes into place in April 2025.

However, after Treasury officials voiced fears that the measures would backfire if they forced non-doms to leave the country, government officials have said they would consider changing the details of the policy to make it less punishing to non-doms. Reducing the amount of inheritance tax they would have to pay is one of the options under consideration.

With a convincing mandate and comfortable majority, Labour should find it easy to deliver on these quickly. The Salisbury Convention will also nullify any potential opposition in the House of Lords, as peers do not vote down Bills mentioned in a manifesto.

What is Labour committed to that is less clear?

Some of Labour’s commitments are low on detail, leaving the door open to speculation. As more detail is released, this article will be updated accordingly.

A pensions review

Labour has previously committed to a pensions review. Its manifesto said this would aim to “improve security in retirement” and deliver better returns for savers.

With detail scarce on what this could mean in reality, however, speculation ran riot during the election campaign.

Ms Reeves previously suggested that tax relief on pension contributions should be set at a flat rate for everyone, rather than relief granted at your highest rate of income tax as it is currently. However, the Chancellor has reportedly abandoned the move due to concerns it could disproportionately affect up to a million public sector workers

Helen Morrissey, of Hargreaves Lansdown, said: “Labour’s promised review of the pension landscape is sorely needed to ensure people continue to get good outcomes from retirement.

“The Government is running out of road when it comes to deploying strategies like raising the state pension age. People need certainty in terms of what they are going to get from the state pension and when, so the state pension needs to be sustainable in the long term.”

Labour’s review will also look at how to increase investment in the UK market by pension funds, which had a mixed reaction from experts.

Mr Tully said: “A new Labour government is likely to want to encourage more investment within the UK from pensions, and potentially wider savings such as Isas. That sounds sensible given the significant funds held within UK pensions which could be helping grow the UK economy.

“But if any new rules require a portion of people’s pensions to be invested in certain, possibly high risk, assets, that may not be the best outcome for an individual.”

Now in government, Labour is highly likely to move forward with the review – but it’s unclear where that may lead and how it might affect savers.

Can Labour afford all of its plans?

Experts have already warned that Labour might struggle to keep to its spending rules and deliver on its promises in the current economic climate.

The Conservatives say that Labour’s plan has a £22bn black hole – which reportedly could have actually grown to £40bn – that early tax increases will need to fill, while think tanks the Institute for Fiscal Studies and the Resolution Foundation have both suggested tax rises could be needed to balance the books.

Ms Coles said: “Labour made some expensive commitments during the campaign, including sticking with the pensions triple lock and ruling out rises in income tax, National Insurance or VAT.

“However, money will be tight. All the maths in the manifesto factored in planned cuts by the former government, so it will be pinning its hopes on squeezing more growth from the economy to help make the numbers stack up. If it doesn’t get the growth, it’s going to need to make some tough choices between spending cuts or additional taxes.”

There are potential revenue-raising opportunities that could be announced during a Budget should a cash injection be needed – and Labour has failed to rule many of these out.