ZUMZ Stock Trading Above 200 & 100-Day SMA: What's Next for Investors?

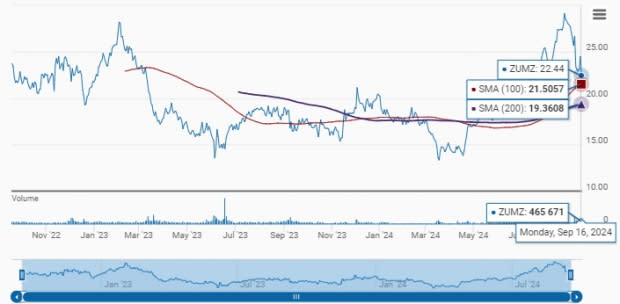

Zumiez Inc. ZUMZ has demonstrated strong upward momentum, consistently trading above both its 200-day and 100-day simple moving averages (SMA), which are important indicators of price stability and long-term bullish trends. As of Friday, ZUMZ was trading at $22.44, which surpassed both its 200-day SMA of $19.36 and its 100-day SMA of $21.51, highlighting a continued uptrend.

SMA is a key tool in technical analysis used to assess price trends by smoothing out short-term fluctuations, offering a clearer view of the stock's longer-term direction. This technical strength, along with the stock's sustained momentum, reflects positive market sentiment and investor confidence in Zumiez's financial health and growth prospects.

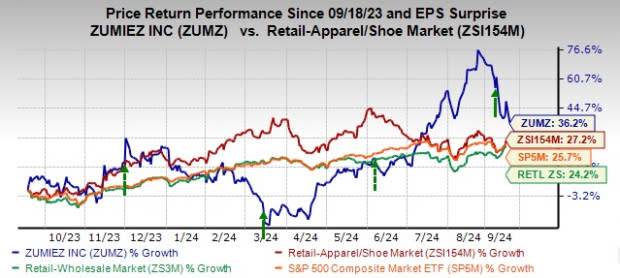

The company has seen a substantial 36.2% jump in its stock price over the past year compared with the Zacks Retail-Apparel and Shoes industry’s 27.2% growth. Also, it outpaced the broader Retail-Wholesale sector's 24.2% growth and the S&P 500 index's 25.7% rise over the said period. Currently, ZUMZ is trading 28.5% below its 52-week high of $31.37, reached on Sept. 6, 2024.

Image Source: Zacks Investment Research

From a valuation perspective, Zumiez’s shares present an attractive opportunity, trading at a discount relative to industry benchmarks. With a forward 12-month price-to-sales ratio of 0.47, which is below the five-year median of 0.58 and the industry’s average of 1.12, the stock offers value for investors seeking exposure to the sector. Moreover, ZUMZ’s current Value Score of A bodes well.

Zumiez Gains on Customer-Centric Focus, Cost Management

Zumiez’s strategic emphasis on a customer-centric business model, strong brand partnerships and careful cost management drove positive results in the second quarter of fiscal 2024. The company has invested in advanced technology to improve the shopping experience across all channels, enhancing its logistics and omnichannel capabilities, which has further solidified its competitive position.

In the second quarter, total sales grew 8.1% year over year to $210.2 million, primarily fueled by the strength of the North American market, where sales rose 10.4%. Comparable sales increased 3.6%, supported by higher average unit retail prices and a greater number of units sold per transaction. The early back-to-school season also played a role, contributing around 530 basis points to net sales growth.

Zumiez’s private label brands, which made up 23% of sales in fiscal 2023, continue to capture market share, appealing to value-conscious consumers. With plans to expand its private-label offerings in 2024, the company is well-positioned for sustained revenue growth. Gross profit improved to $71.8 million in the second quarter. The gross margin was 34.2%, up 250 basis points from the previous year, due to reduced store occupancy and distribution costs, among other factors.

In Europe, Zumiez has shifted from rapid store expansion to existing store productivity optimization, with a strategic push toward full-price selling. This change has already improved merchandising margins in the region. Additionally, the company has been closing underperforming stores in North America while expanding in key markets globally, alongside initiatives to optimize labor and reduce logistics costs to enhance long-term profitability.

Image Source: Zacks Investment Research

ZUMZ’s International Sales Under Pressure

Despite strong results in North America, Zumiez's international sales, particularly in Europe, declined 2.6% year over year to $33.9 million in the second quarter, with a 7.6% drop in international comparable sales. The shift to full-price selling in a tough retail environment has pressured growth, raising concerns about the company's ability to improve performance in key international markets. Continued weakness is likely to impact overall revenue growth.

Zumiez Q3 & Fiscal 2024 Guidance

Nonetheless, Zumiez remains optimistic about its third-quarter and full-year performance. The company forecasts third-quarter sales to be between $221 million and $225 million, reflecting a 2-4% year-over-year increase, with comparable sales up 12.1% through Sept. 2. Despite macroeconomic uncertainties, it anticipates low single-digit sales growth for fiscal 2024, driven by stable revenue and ongoing cost efficiencies, supporting positive operating margins.

Final Thoughts

Investors should consider ZUMZ as a promising stock due to its strong technical performance and positive financial outlook. The company's ability to trade above key moving averages, along with consistent growth in North American sales and expansion in private label offerings, positions it well for growth.

While international sales, particularly in Europe, remain a challenge, Zumiez’s strategic focus on cost management, efficiency improvements and omnichannel capability expansion provides a solid foundation for sustained profitability. Trading at a discount relative to industry benchmarks and with a strong Value Score, ZUMZ offers an attractive opportunity for investors seeking both stability and growth potential. The company currently carries a Zacks Rank #3 (Hold).

Key Picks

Some better-ranked stocks are Boot Barn Holdings, Inc. BOOT, Abercrombie & Fitch Co. ANF and Steven Madden, Ltd. SHOO.

Boot Barn operates as a lifestyle retail chain devoted to western and work-related footwear, apparel and accessories. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Boot Barn’s fiscal 2025 earnings and sales indicates growth of 10.7% and 11.6%, respectively, from the fiscal 2024 reported figures. BOOT has a trailing four-quarter average earnings surprise of 7.1%.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It sports a Zacks Rank of 1 at present. ANF delivered a 16.8% earnings surprise in the last reported quarter.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and sales indicates growth of 63.4% and 12.6%, respectively, from the fiscal 2024 reported levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Steven Madden designs, sources, markets and sells fashion-forward name-brand and private-label footwear. It currently has a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Steven Madden’s 2024 earnings and sales indicates growth of 6.9% and 12.6%, respectively, from the year-ago actuals. SHOO has a trailing four-quarter average earnings surprise of 9.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zumiez Inc. (ZUMZ) : Free Stock Analysis Report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

Steven Madden, Ltd. (SHOO) : Free Stock Analysis Report