Williams Stock Hits 52-Week High: Is the Bull Run Over?

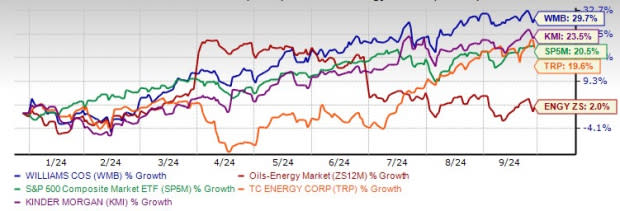

The Williams Companies WMB, a premier energy infrastructure provider in North America, continues its uptrend. The stock closed Friday’s session at $45.16 after setting a new 52-week high of $46.48 earlier in the week. As shown in this chart, with the advance, WMB shares are up almost 30% since the start of the year, handily outperforming the sector and the S&P 500. The company has also fared better than other midstream operators like TC Energy TRP and Kinder Morgan KMI.

WMB, TRP and KMI Stock Performance Comparison

Image Source: Zacks Investment Research

Given this impressive year-to-date performance, can investors still consider buying WMB stock, or should you book profits? Let’s delve deeper into the company’s fundamentals.

5 Reasons to Like Williams Stock

Robust Asset Portfolio With Growth Opportunities: Williams Companies boasts a robust infrastructure, including 32.3 billion cubic feet/day (Bcf/d) of gas transmission capacity and 28.5 Bcf/d of gathering capacity. This network is supported by significant processing and storage capacities, enabling WMB to handle growing demand. With a backlog of 11.5 Bcf/d in projects through 2032, WMB is well-positioned for mid-to-high single-digit growth, ensuring future shareholder returns through infrastructure expansion.

Strong Execution and Project Expansions: Williams has successfully executed several key projects across multiple regions, including placing the Transco Regional Energy Access into full service ahead of schedule and under budget. The company's ability to deliver projects like the Marcellus gathering expansion and the fully contracted Basin transmission expansion in the Northeast, West, and Gulf of Mexico positions it well for continued earnings growth.

Reliable Dividend Growth: Williams Companies has consistently grown its dividend, recently increasing it by 6% to 47.50 cents per share. Backed by a strong dividend coverage ratio, the firm’s ability to pay and grow dividends remains robust. Over the last five years, Williams has outperformed its midstream peers in dividend growth, hiking its payout by more than 4% over the last five years. As a result, WMB is seen as an attractive choice for income-seeking investors, given the stability of its cash flow.

Strategic Acquisitions and Portfolio Optimization: Williams is optimizing its asset portfolio through strategic moves such as selling its stake in the Aux Sable joint venture and consolidating its ownership in the Gulf of Mexico Discovery system. These actions are expected to enhance long-term growth prospects. The acquisition of an additional interest in Discovery is anticipated to boost EBITDA, driven by Chevron's Anchor development and Beacon's Winterfell program. These efforts not only strengthen Williams’ asset base but also enhance its ability to capitalize on near-term and long-term growth opportunities.

Impressive Earnings History: The Williams Companies has surpassed earnings estimates in each of the last four quarters. Back in August, the company reported second-quarter earnings of 43 cents per share, a 10.3% surprise over the 39 cents per share consensus estimate. WMB has delivered a trailing four-quarter average earnings surprise of 11.3%.

While Williams Companies has strong long-term potential, the current market conditions and specific challenges facing the company cannot be ignored.

Red Flags for WMB Stock

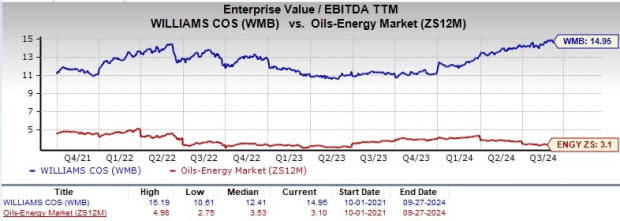

Overvaluation Concerns: Williams Companies’ stock is currently trading at a 20% premium to its three-year average EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) multiple of 12.41, with a valuation of 14.95. This suggests the stock might be overvalued compared to its industry peers, which average 12.57. The premium valuation limits near-term upside potential.

Image Source: Zacks Investment Research

Lower Natural Gas Prices: Despite a 3.5% year-over-year increase in adjusted EBITDA during the second quarter, Williams' earnings are heavily exposed to natural gas price fluctuations, which fell about 5% year over year. This company's revenue and profitability targets might suffer if fuel prices remain depressed or volatile. Continued weak prices could slow the projected 8% CAGR in EBITDA through 2025, dampening the stock’s performance.

High Debt: Williams Companies' debt burden is a concern for investors and restricts its credit profile. In fact, the company's debt-to-capitalization at the end of second quarter of 2024 was 62% - quite high compared to peers. Elevated debt levels increase financial risk and could strain the company's balance sheet, especially if there are adverse market conditions or unexpected operational issues.

Execution Risks in Growth Projects: Williams Companies has an ambitious growth pipeline, with projects like the $1.5 billion SSE pipeline slated for completion by 2027. However, execution delays or cost overruns could hamper profitability and strain cash flow. With a backlog of 11.5 Bcf/d of projects, any missteps in execution or lower-than-expected capacity utilization could reduce future returns and put pressure on stock performance.

Final Thoughts on Willliams Stock: Hold it for Now

The Williams Companies presents a compelling long-term investment case with its robust business model, strategic acquisitions and consistent dividend growth. However, WMB’s elevated valuation suggests that the market may have already priced in much of the company's potential growth. As a result, any negative developments or earnings disappointments could trigger a sharp decline in the stock price as investors reassess its overvaluation. Given these mixed factors, a prudent approach would be to wait for a more favorable entry point before committing to a position in The Williams Companies. Till then, holding onto your shares could pay off.

WMB carries a Zacks Rank #3 (Hold) at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Williams Companies, Inc. (The) (WMB) : Free Stock Analysis Report

TC Energy Corporation (TRP) : Free Stock Analysis Report

Kinder Morgan, Inc. (KMI) : Free Stock Analysis Report