Where Will Chevron Be in 10 Years?

Chevron (NYSE: CVX) has basically decided to stick pretty close to its core, continuing to produce oil and natural gas instead of shifting toward cleaner alternatives as some European energy giants have done. Some investors might view that as a mistake, given the ongoing growth of renewable power. The fear is that oil and natural gas will eventually become obsolete. History suggests that's not likely to happen and it almost certainly won't happen in the next 10 years.

What does Chevron do?

Chevron is an integrated energy company, which means that its operations span across the entire energy sector. It produces oil and natural gas in its upstream operations, transports these vital fuels in its midstream business, and processes them into chemicals and fuels in its refining segment. Although the price of oil and natural gas are the driving force behind revenues and earnings, having a diversified portfolio of assets helps to soften the industry's commodity-driven volatility.

In this way, Chevron is something of a through-the-cycle choice in the energy sector. With a generous 4.5% dividend yield it might even interest income investors today, though during deep oil downturns that yield can get up to 6% or more. Clearly, for those with a value bias, taking a contrarian stance and buying when most are selling will be more appropriate. That said, Chevron has increased its dividend annually for 37 consecutive years, so buying today, given the measly 1.2% dividend yield on offer from the S&P 500 index, isn't necessarily a bad call.

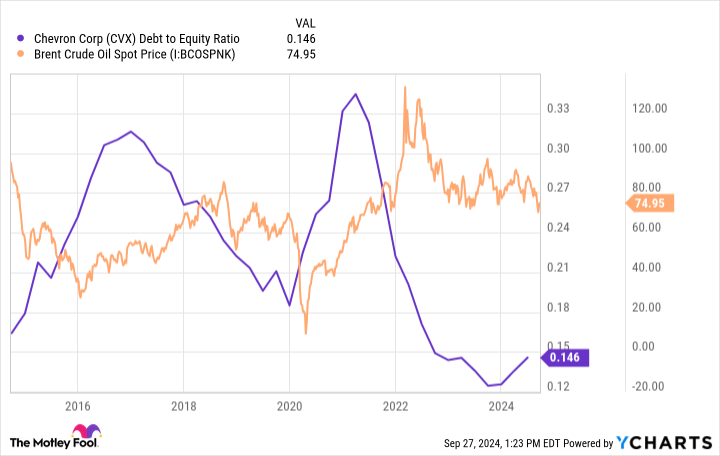

One of the key selling points here, however, is Chevron's balance sheet. Indeed, Chevron's debt-to-equity ratio is lower than any of its closest peers at just 0.15 times. That gives it the leeway to add leverage during difficult periods so that it can continue to support its business and dividend. When energy markets recover, as they always have historically, it reduces leverage in preparation for the next industry downturn.

What about the clean energy threat to Chevron's business?

That's all well and good, but there's a long-term threat that many investors are worried about here: The growth of clean energy. That's definitely an issue worth watching, but it isn't likely to be as big an issue as some investors may fear, particularly not over as short a period as 10 years.

About 200 years ago biomass (burning things like wood) was the primary source of energy. It is still in wide use today even though coal became the more dominant fuel source about 100 years ago. Coal is still in wide use today even though it was overtaken by oil and natural gas as an energy source in the mid-1900s.

Given this track record, it seems likely that oil and natural gas will remain important to the energy mix even as the use of solar and wind increase. Note, however, these two clean energy options are just tiny pieces of the global energy pie today. So it will likely be a long time before oil and natural gas are displaced from their perch atop the energy pile.

In fact, if you examine the forecasts from some of the most important energy industry watchers, like OPEC, the Energy Information Administration (EIA), and the International Energy Agency (IEA), they all predict that oil and natural gas will remain vital to the world through the end of their projection periods, which range from 2045 to 2050. Even in the worst case scenario offered up by the IEA, oil and natural gas will continue to be vitally important a decade from now.

Given Chevron's scale, global reach, and financial strength, it seems highly unlikely that Chevron won't be able to successfully navigate the next decade while continuing to reward income investors with dividend growth.

Chevron is helping the world grow

The real key here is that the world's population continues to expand and, at the same time, move higher up on the socioeconomic ladder. That fuels energy demand of all kinds. To put a number on it, China's energy use increased 357% between 1990 and 2021, while India's use increased 158%. Not only is there more room for India to keep growing its energy use, but the energy use of both nations grew right along with their average education levels and life expectancy. More energy means better lives, which is particularly true for the world's poorest inhabitants.

While you can look down on Chevron for creating carbon-based fuels, it is those very fuels that have underpinned the improvement in the lives of people around the world. As China and India, and more alongside them, grow and expand their economic might, they will increasingly use renewable power while continuing to rely on the oil and natural gas backbone that has supported them for decades. This is why Chevron is continuing to produce oil and natural gas and why its business has at least a decade, but probably many decades, of solid performance ahead of it.

Should you invest $1,000 in Chevron right now?

Before you buy stock in Chevron, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chevron wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $744,197!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 30, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron. The Motley Fool has a disclosure policy.

Where Will Chevron Be in 10 Years? was originally published by The Motley Fool