Vertex And 2 Other Stocks That May Be Trading Below Estimated Fair Value On US Exchanges

As the U.S. stock market stabilizes following a recent selloff, major indexes have shown slight gains, reflecting cautious optimism among investors amid ongoing geopolitical tensions and economic data releases. In this environment, identifying stocks that may be trading below their estimated fair value can present intriguing opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

Name | Current Price | Fair Value (Est) | Discount (Est) |

Peoples Financial Services (NasdaqGS:PFIS) | $44.77 | $87.03 | 48.6% |

First Internet Bancorp (NasdaqGS:INBK) | $31.37 | $62.52 | 49.8% |

Phibro Animal Health (NasdaqGM:PAHC) | $21.76 | $42.63 | 49% |

Veritex Holdings (NasdaqGM:VBTX) | $24.85 | $48.31 | 48.6% |

California Resources (NYSE:CRC) | $52.68 | $104.27 | 49.5% |

Symbotic (NasdaqGM:SYM) | $24.175 | $47.74 | 49.4% |

Tenable Holdings (NasdaqGS:TENB) | $40.74 | $79.11 | 48.5% |

Vitesse Energy (NYSE:VTS) | $24.77 | $49.03 | 49.5% |

EVERTEC (NYSE:EVTC) | $33.82 | $66.16 | 48.9% |

SunOpta (NasdaqGS:STKL) | $6.46 | $12.65 | 48.9% |

Let's take a closer look at a couple of our picks from the screened companies.

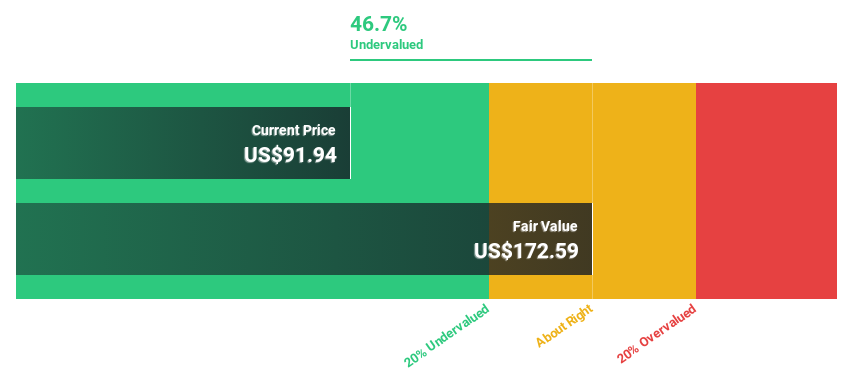

Vertex

Overview: Vertex, Inc. offers enterprise tax technology solutions for the retail trade, wholesale trade, and manufacturing industries both in the United States and internationally, with a market cap of approximately $6.10 billion.

Operations: The company's revenue is primarily derived from its Software & Programming segment, which generated $617.83 million.

Estimated Discount To Fair Value: 38.8%

Vertex is trading at US$41.1, significantly below its estimated fair value of US$67.18, making it highly undervalued based on discounted cash flow analysis. Despite recent insider selling and shareholder dilution, Vertex's earnings are projected to grow 36.8% annually over the next three years—outpacing the broader US market growth forecast of 15.2%. Recent initiatives like integrating with Salesforce Revenue Cloud could enhance revenue processes and compliance for businesses, potentially supporting future growth.

The growth report we've compiled suggests that Vertex's future prospects could be on the up.

Click to explore a detailed breakdown of our findings in Vertex's balance sheet health report.

Amer Sports

Overview: Amer Sports, Inc. is a company that designs, manufactures, markets, distributes, and sells sports equipment, apparel, footwear, and accessories across Europe, the Middle East, Africa, the Americas, China, and the Asia Pacific with a market cap of approximately $8.31 billion.

Operations: The company's revenue segments include Technical Apparel at $1.85 billion, Outdoor Performance at $1.72 billion, and Ball & Racquet Sports at $1.07 billion.

Estimated Discount To Fair Value: 15%

Amer Sports is trading at US$16.57, approximately 15% below its estimated fair value of US$19.49, suggesting it may be undervalued based on cash flow analysis. The company reported a significant reduction in net loss for Q2 2024 compared to the previous year and anticipates revenue growth of up to 17% for the full year. Earnings are forecasted to grow annually by 46.68%, with profitability expected within three years, surpassing average market growth rates.

Navigate through the intricacies of Amer Sports with our comprehensive financial health report here.

Live Nation Entertainment

Overview: Live Nation Entertainment, Inc. is a global live entertainment company with a market cap of approximately $25.48 billion.

Operations: The company generates revenue through its Concerts segment at $19.72 billion, Ticketing at $3.03 billion, and Sponsorship & Advertising at $1.15 billion.

Estimated Discount To Fair Value: 41.6%

Live Nation Entertainment is trading at US$111.53, significantly below its estimated fair value of US$190.95, indicating potential undervaluation based on discounted cash flow analysis. Despite a modest revenue increase to US$6.02 billion in Q2 2024, net income rose slightly to US$297.97 million from the previous year. Earnings are projected to grow annually by 29.32%, outpacing the broader market's growth rate and supported by a very high forecasted return on equity of 65.4%.

Make It Happen

Embark on your investment journey to our 193 Undervalued US Stocks Based On Cash Flows selection here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGM:VERX NYSE:AS and NYSE:LYV.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com