Unveiling 3 Top Undervalued Small Caps In United States With Insider Buying

The market is up 3.6% in the last 7 days, with all sectors gaining ground. In the last year, the market has climbed 20%, and earnings are forecast to grow by 15% annually. In this thriving environment, identifying undervalued small-cap stocks with insider buying can offer unique opportunities for investors looking to capitalize on growth potential and strong internal confidence.

Top 10 Undervalued Small Caps With Insider Buying In The United States

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Ramaco Resources | 12.5x | 0.9x | 33.68% | ★★★★★★ |

Columbus McKinnon | 20.3x | 0.9x | 44.16% | ★★★★★★ |

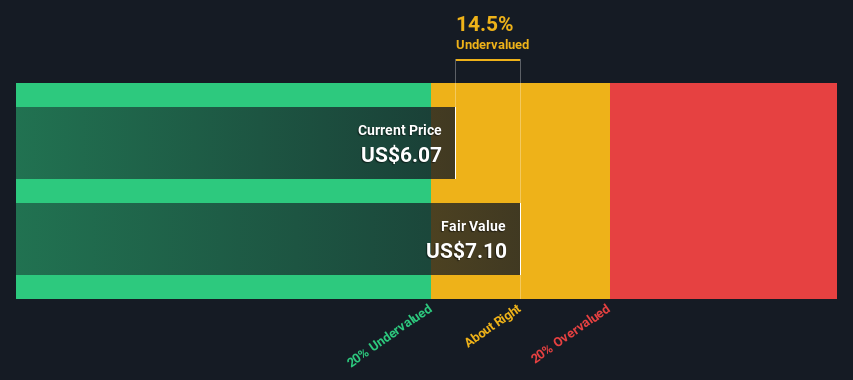

Thryv Holdings | NA | 0.7x | 26.22% | ★★★★★☆ |

AtriCure | NA | 2.5x | 43.47% | ★★★★★☆ |

Titan Machinery | 3.7x | 0.1x | 35.49% | ★★★★★☆ |

Chatham Lodging Trust | NA | 1.2x | 32.93% | ★★★★★☆ |

Franklin Financial Services | 9.6x | 1.9x | 40.35% | ★★★★☆☆ |

Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

American Vanguard | NA | 0.3x | -109.19% | ★★★☆☆☆ |

Alta Equipment Group | NA | 0.1x | -51.18% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

Chimera Investment

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Chimera Investment operates by investing, on a leveraged basis, in a diversified portfolio of mortgage assets and has a market cap of approximately $1.49 billion.

Operations: Chimera Investment's revenue primarily comes from its diversified portfolio of mortgage assets, with recent quarterly revenue at $306.43 million. The company has experienced fluctuations in net income margin, notably achieving a peak of 1.52% and a low of -1.98% over the analyzed periods.

PE: 8.2x

Chimera Investment Corporation, a small-cap stock, has seen insider confidence with recent share purchases. Despite earnings forecasted to decline by 5.8% annually over the next three years, Q2 2024 net income rose to US$56.66 million from US$36.02 million last year. The company announced a fixed-income offering of senior unsecured notes due August 2029 and declared multiple preferred dividends payable in September 2024. Their debt remains poorly covered by operating cash flow, indicating potential financial risk ahead.

Delek US Holdings

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Delek US Holdings operates in the energy sector, focusing on refining, logistics, and retail operations with a market cap of $1.90 billion.

Operations: The company generates revenue primarily from its refining segment, which contributes $14.98 billion, followed by logistics at $1.05 billion, and retail at $854.60 million. In the latest quarter ending 2024-06-30, it reported a gross profit of $835.50 million with a gross profit margin of 5.41%.

PE: -13.0x

Delek US Holdings, a small cap energy company, recently provided guidance for Q3 2024 with expected crude throughput between 290,000 and 305,000 bpd. Despite reporting a net loss of US$37.2 million in Q2 2024 compared to US$8.3 million the previous year, insider confidence is evident with recent share purchases by executives in July and August. The company also increased its quarterly dividend to US$0.255 per share, reflecting commitment to shareholder returns amidst challenging financials.

Delve into the full analysis valuation report here for a deeper understanding of Delek US Holdings.

Understand Delek US Holdings' track record by examining our Past report.

Granite Ridge Resources

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Granite Ridge Resources focuses on the development, exploration, and production of oil and natural gas with a market cap of approximately $1.25 billion.

Operations: The company derives its revenue primarily from oil and natural gas development, exploration, and production. Over recent periods, the gross profit margin has shown fluctuations, with the latest being 82.21%.

PE: 15.0x

Granite Ridge Resources, a small-cap stock, recently reported a net income of US$5.1 million for Q2 2024, down from US$8.74 million the previous year. Despite lower profit margins at 15.3%, the company forecasts earnings growth of 22.17% annually and maintains production guidance between 23,250 to 25,250 BOE per day for 2024. Insider confidence is evident with recent share purchases in July and August. The firm declared a quarterly dividend of US$0.11 per share payable on September 13, indicating steady shareholder returns amidst financial fluctuations.

Dive into the specifics of Granite Ridge Resources here with our thorough valuation report.

Explore historical data to track Granite Ridge Resources' performance over time in our Past section.

Make It Happen

Embark on your investment journey to our 57 Undervalued US Small Caps With Insider Buying selection here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NYSE:CIM NYSE:DK and NYSE:GRNT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com