Undervalued Small Caps In United Kingdom With Insider Buying October 2024

The United Kingdom's stock market has faced headwinds recently, with the FTSE 100 and FTSE 250 indices both closing lower amid concerns over weak trade data from China and its impact on global demand. As broader market sentiment remains cautious, particularly for companies tied to international economies, investors may find opportunities in small-cap stocks that exhibit strong fundamentals and insider buying trends, signaling potential resilience in uncertain times.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Bytes Technology Group | 26.0x | 5.9x | 6.53% | ★★★★★☆ |

NWF Group | 8.8x | 0.1x | 34.30% | ★★★★★☆ |

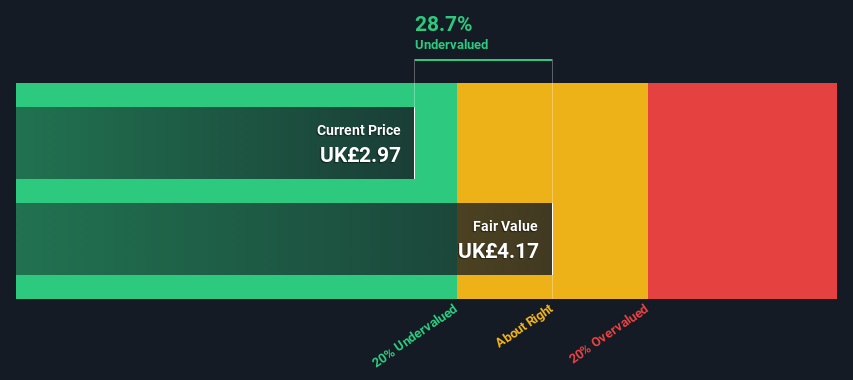

Learning Technologies Group | 15.7x | 1.4x | 36.55% | ★★★★★☆ |

Headlam Group | NA | 0.2x | 25.54% | ★★★★★☆ |

CVS Group | 28.9x | 1.2x | 37.42% | ★★★★☆☆ |

Essentra | 720.4x | 1.4x | 38.19% | ★★★★☆☆ |

Genus | 171.0x | 2.0x | -2.10% | ★★★★☆☆ |

Marlowe | NA | 0.7x | 40.41% | ★★★★☆☆ |

Optima Health | NA | 1.2x | 42.63% | ★★★★☆☆ |

Oxford Instruments | 22.7x | 2.4x | -27.00% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Domino's Pizza Group

Simply Wall St Value Rating: ★★★★★☆

Overview: Domino's Pizza Group operates as a leading pizza delivery and carryout chain, generating income through sales to franchisees, corporate stores, advertising and ecommerce, rental income on properties, and various franchise fees, with a market capitalization of £1.54 billion.

Operations: The company's revenue streams include significant income from sales to franchisees, royalties, franchise fees, and national advertising. Operating expenses are primarily driven by general and administrative costs and sales & marketing expenses. The gross profit margin has shown an upward trend reaching 47.48% in recent periods.

PE: 15.2x

Domino's Pizza Group, a smaller UK company, faces high debt levels with all liabilities stemming from external borrowing. Despite this, insider confidence is evident through recent share purchases. The company repurchased 25.3 million shares for £90.1 million by May 2024 and announced further buybacks in August 2024. Although profits dipped to £42.3 million for H1 2024 from £80.2 million the previous year, strategic initiatives aim to boost sales and order growth throughout the year.

Take a closer look at Domino's Pizza Group's potential here in our valuation report.

Evaluate Domino's Pizza Group's historical performance by accessing our past performance report.

Genel Energy

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Genel Energy is an independent oil and gas exploration and production company with operations primarily in the Kurdistan Region of Iraq, and it has a market cap of approximately £0.38 billion.

Operations: Genel Energy's revenue primarily comes from production activities, with the latest figures showing $74.40 million. The gross profit margin has fluctuated significantly, reaching as high as 102.26% and recently standing at 80.11%. Operating expenses and non-operating expenses have consistently impacted net income, which has been negative in recent periods.

PE: -8.3x

Genel Energy, a smaller player in the UK market, has recently seen insider confidence with Yetik Mert purchasing 107,000 shares valued at US$91,774. This move suggests belief in the company's potential despite recent challenges. In H1 2024, Genel reported sales of US$37.6 million and a net loss of US$21.9 million; however, production increased to 19,510 bopd from 13,440 bopd year-on-year. Recent board appointments and leadership changes could offer strategic direction for future growth prospects.

Click here to discover the nuances of Genel Energy with our detailed analytical valuation report.

Gain insights into Genel Energy's historical performance by reviewing our past performance report.

Genus

Simply Wall St Value Rating: ★★★★☆☆

Overview: Genus is a leading global animal genetics company specializing in bovine and porcine breeding, with a market cap of approximately £1.71 billion.

Operations: Genus generates revenue primarily from Genus ABS and Genus PIC, with a notable gross profit margin trend reaching as high as 68.02% in March 2024. The company's operating expenses have varied significantly over time, with recent figures showing £614.90 million in June 2024.

PE: 171.0x

Genus, a UK-based company, has seen insider confidence with recent share purchases. Despite facing challenges in the past year, including net income dropping to £7.9 million from £33.3 million and earnings per share declining significantly, the company's forecasted 37% annual earnings growth suggests potential for recovery. While profit margins have shrunk to 1.2%, Genus maintains consistent dividends and relies solely on external borrowing for funding, which carries inherent risks but also opportunities if managed well in future strategies.

Unlock comprehensive insights into our analysis of Genus stock in this valuation report.

Review our historical performance report to gain insights into Genus''s past performance.

Turning Ideas Into Actions

Navigate through the entire inventory of 25 Undervalued UK Small Caps With Insider Buying here.

Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LSE:DOM LSE:GENL and LSE:GNS.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com