Can Ulta Beauty Stock Bounce Back Amid Changing Market Dynamics?

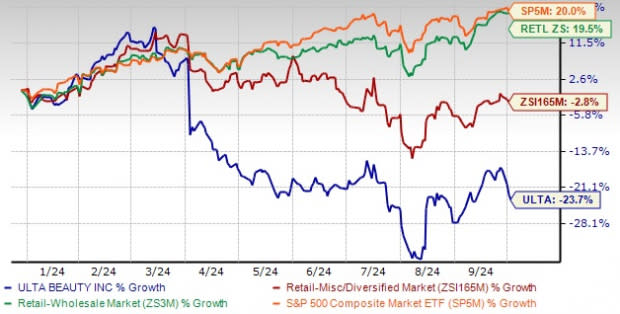

Ulta Beauty, Inc. ULTA experienced significant volatility, with shares dropping 23.7% year to date compared with the industry’s decline of 2.8%. The Retail and Wholesale sector and the S&P 500 registered increases of 19.5% and 20%, respectively, highlighting ULTA’s underperformance during this period.

The company has long been a powerhouse in the beauty retail industry, offering a wide array of products. However, it faces significant challenges stemming from changing consumer preferences and heightened competition. The beauty industry is undergoing a transformation as shoppers continue to prioritize value-driven purchases. This is a challenge for ULTA’s traditional market position. Competitors are ramping up their presence, offering a wider selection of premium beauty products and the company is feeling the impact.

As it navigates these headwinds, ULTA’s ability to adapt to the evolving landscape will be critical. With consumers leaning toward affordable options and competitors aggressively targeting the prestige beauty segment, the company is at a crossroads. The question remains — can Ulta Beauty effectively balance these dynamics to regain its momentum to sustain long-term growth?

Image Source: Zacks Investment Research

Shifts in Consumer Spending Impact ULTA’s Performance

Ulta Beauty is facing challenges as consumer behavior shifts toward value-driven spending, combined with rising competition from new beauty distribution channels, which is eroding its market share. Its transition to a new Enterprise Resource Planning (ERP) system caused operational disruptions. Also, promotional efforts have failed to boost in-store sales as expected.

The beauty industry's growth has also slowed, with U.S. beauty sales increasing 3% in the first half of 2024. This normalization, after years of rapid growth, has hit the company hard, as inflation and economic uncertainty push consumers to prioritize affordable products over premium ones. This shift poses long-term risks for ULTA’s high-end product lines, historically a major profit driver. Increased competition in the prestige beauty segment is further impacting its market share.

These challenges were evident in Ulta Beauty’s second-quarter fiscal 2024 results, with revenues and earnings missing the Zacks Consensus Estimate and earnings per share (EPS) falling year over year. Comparable sales dropped 1.2%, with a 1.8% decline in transactions, in spite of a slight rise in average ticket size. These results underscore the headwinds it faces in an increasingly competitive, value-driven market.

Rising Costs Weigh on ULTA’s Profitability

Ulta Beauty has been battling rising selling, general and administrative (SG&A) expenses. In the fiscal second quarter, SG&A costs rose 7.3% year over year, expanding 160 basis points (bps) to 25.3% of net sales. The rise in such costs can be attributed to the deleveraging of store payroll and benefits, higher corporate overhead from strategic investments and increased store and marketing expenses.

These rising costs are squeezing profitability, contributing to a 1% decline in gross margins during the second quarter. Promotional activities, a weaker brand mix, and higher fixed costs have eroded the merchandise margin, with management forecasting further pressure for the remainder of the fiscal year. Management expects the gross margin to contract 70-90 bps in the fiscal 2024 due to lower merchandise margins and higher store fixed costs.

Prestige Beauty Hurdles Poses Risks For ULTA

Ulta Beauty is facing considerable challenges in its high-margin prestige beauty segment, which has been a key driver of profitability. One of the major hurdles is increased competition, with more than 1,000 new points of distribution for prestige beauty opening in the last three years. This influx of competitors, ranging from specialty stores to large retailers, diluted its market share, especially in key categories like makeup and hair care. Consumer behavior is shifting toward value-driven spending, with many opting for mass-market beauty products over premium offerings due to inflationary pressures.

According to Circana data for the 13 weeks ended Aug. 3, the company maintained its market share in the mass beauty segment but lost ground in prestige beauty, driven by weakness in makeup and hair care categories. Despite efforts to introduce new brands and exclusive products, these external pressures are causing ULTA to lose share in the prestige beauty space, making it harder to maintain growth and profitability in this segment.

Road Ahead Looks Tough for ULTA

Considering the performance in the first half and a more cautious perspective, the company recently revised its full-year expectations downward. Ulta Beauty expects the fiscal 2024 net sales in the band of $11-$11.2 billion compared with the earlier mentioned $11.5-$11.6 billion range. The company reported net sales of $11.2 billion in the fiscal 2023. Comparable sales are expected to remain flat to down 2% year over year. The metric was earlier anticipated to rise 2-3%. The revised forecast accounts for the first-half performance and anticipates that it will take additional time for the company’s growth initiatives to impact sales positively.

Stores facing multiple competitive openings are expected to experience continued pressure compared to the rest of the fleet. The operating environment remains dynamic, suggesting further strain on consumer spending. Management expects an operating margin to be between 12.7% and 13% compared with the previously mentioned 13.7-14%. For the fiscal 2024, earnings are envisioned in the $22.60-$23.50 band per share, lower than the earlier stated $25.20-$26 band.

Investors Guide for ULTA

Ulta Beauty is facing significant pressure from shifting consumer preferences, operational disruptions, and increased competition. Challenges in its premium beauty segment are adding to the company's struggles. With management lowering fiscal 2024 guidance, the short-term outlook appears cautious. Investors should closely monitor the company’s ability to navigate headwinds to regain momentum. At present, ULTA carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Better-Ranked Retail Stocks

Build-A-Bear Workshop BBW is the leading and only national company providing a make-your-own stuffed animal interactive retail entertainment experience. BBW currently has a Zacks Rank #2 (Buy). It has a trailing four-quarter negative earnings surprise of 3.9%, on average.

The Zacks Consensus Estimate for BBW’s current financial-year sales and earnings suggests growth of 1.2% and 8.8%, respectively, from the year-ago reported figures.

Burlington Stores, Inc. BURL operates as a retailer of branded merchandise in the United States and has a Zacks Rank of 2. BURL has a trailing four-quarter earnings surprise of 18.4%, on average.

The Zacks Consensus Estimate for Burlington Stores’ current financial year’s sales and earnings implies a rise of 10.1% and 30.5%, respectively, from the year-earlier reported figures.

Boot Barn BOOT operates as a lifestyle retail chain devoted to western and work-related footwear, apparel and accessories. BOOT currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales and earnings indicates growth of 11.5% and 10.5%, respectively, from the year-earlier actuals. BOOT has a trailing four-quarter earnings surprise of 7.1%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ulta Beauty Inc. (ULTA) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

Build-A-Bear Workshop, Inc. (BBW) : Free Stock Analysis Report

Burlington Stores, Inc. (BURL) : Free Stock Analysis Report