Twilio Stock Trades at Low P/E Multiple: What Should You Do Now?

Twilio Inc. TWLO is currently trading at a low price-to-earnings (P/E) multiple, far below the broader tech sector and S&P 500 averages. Twilio’s forward 12-month P/E ratio sits at 15.34, significantly lower than the Zacks Computer and Technology sector’s average of 24.76 and the S&P 500’s average of 20.88.

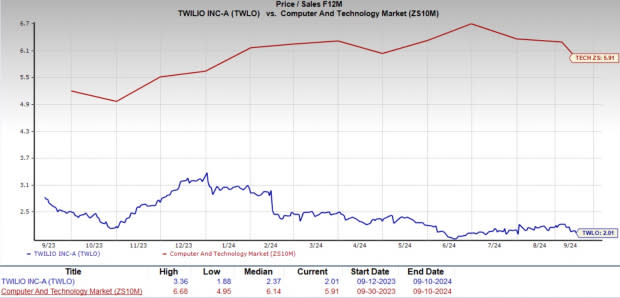

Twilio's price-to-sales (P/S) ratio is also on the low end, reflecting investor concerns. But the real question for investors is whether this low valuation makes Twilio a bargain, or whether it reflects deeper issues that could hold the stock down.

Image Source: Zacks Investment Research

Slowing Sales Growth Weighs Heavily on TWLO Stock

Twilio's stock price has taken a significant hit in the year-to-date (YTD) period. The stock has declined by approximately 25% since the start of 2024, which brought down its valuation metrics significantly. TWLO stock has also underperformed the Zacks Internet – Software industry’s YTD growth of 11%. The broader tech sector and the S&P 500 have soared 14.6% and 15%, respectively, YTD.

YTD Price Return Performance

Image Source: Zacks Investment Research

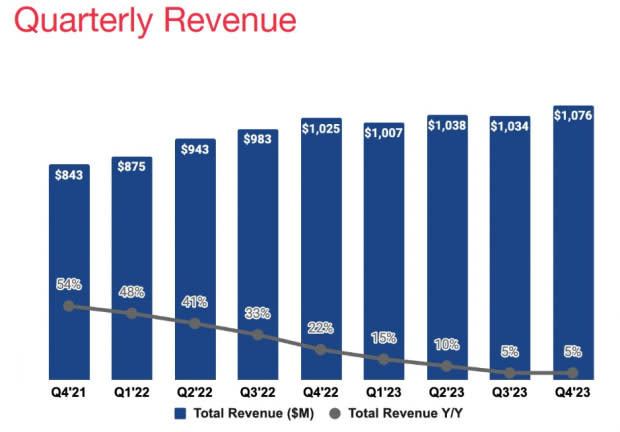

The primary reason for this underperformance is its decelerating revenue growth, which has raised concerns about its future potential. Twilio was once celebrated as a high-growth tech star, but the company’s revenue expansion has slowed. In the first and second quarters of 2024, Twilio posted a year-over-year revenue increase of 4% and 7%, respectively. This compares unfavorably with the high-double-digit growth rates Twilio experienced just a few years ago.

Back in 2021, Twilio’s annual revenues surged more than 50%, fueled by digital transformation trends during the pandemic. However, in 2024, growth has decelerated. Its Communications segment, a key revenue driver, has been especially impacted, as businesses are exercising caution with marketing and customer engagement budgets amid macroeconomic uncertainty. The transition from pandemic-era demand to more conservative spending has created headwinds for Twilio’s growth.

Quarterly Revenue Trend

Image Source: Twilio Inc.

Twilio’s Long-Term Prospects Remain Strong

Despite short-term challenges, Twilio’s long-term potential remains solid. The company has consistently positioned itself as a leader in the customer engagement and communications space, offering a platform that powers real-time, personalized experiences for businesses around the world.

One of Twilio’s most promising growth drivers moving forward is its increasing focus on artificial intelligence (AI). Twilio has integrated AI-driven solutions into its customer engagement platform, enabling businesses to automate and personalize interactions at scale. Products like Twilio Verify and Voice Intelligence are expected to grow in importance as businesses prioritize enhancing customer experiences with AI-driven personalization and operational efficiency.

Twilio’s Segment business, which provides customer data platforms, is becoming a key player in the company’s growth strategy. Segment enables organizations to consolidate customer data from multiple touchpoints, allowing for more personalized and effective marketing efforts. As more industries rely on data-driven customer insights, Twilio’s Segment could evolve into a major revenue generator.

By combining its robust communication tools with AI-powered solutions and data analytics, Twilio differentiates itself in a crowded market. The demand for personalized, efficient customer engagement tools is not going away, and Twilio is well-positioned to capitalize on this growing trend.

Twilio is Positioned Strongly Against Competitors

In a highly competitive space, Twilio faces stiff competition from tech giants like Cisco Systems CSCO, Microsoft MSFT and Amazon AMZN, all of whom offer similar communication solutions. Cisco's Webex Connect, Microsoft’s Azure Communication Services and Amazon's AWS Communication Developer Services are formidable rivals, but Twilio has managed to carve out a unique space for itself.

Twilio’s developer-friendly platform and extensive API ecosystem have made it a preferred choice for companies looking to build custom communication solutions. Its ability to offer highly customizable communication tools, alongside its extensive global reach in more than 180 countries, gives Twilio a competitive edge. In contrast, competitors often offer more regionalized or standardized services.

Twilio’s API-first approach has attracted a broad range of clients, from startups to large enterprises, solidifying its market position. While its competitors benefit from broader cloud service offerings, Twilio’s focus on communications allows it to innovate quickly and cater directly to the needs of its clients. This agility is crucial as Twilio adapts to the fast-evolving landscape of customer engagement technology.

Conclusion: Hold TWLO Stock for Now

While Twilio’s low P/E multiple may make the stock appear undervalued, the company faces real challenges, particularly regarding slowing sales growth. Broader market volatility and cautious corporate spending have weighed on Twilio’s stock performance, but the company’s fundamentals remain strong. Its long-term prospects, driven by AI integration and customer data platforms like Segment, are promising.

For investors currently holding Twilio stock, its low valuation presents an opportunity to stay on the course as the company navigates short-term headwinds. Twilio’s leadership in the customer engagement space, combined with its AI-driven innovations, positions it well for future growth. While this Zacks Rank #3 (Hold) company may experience further volatility in the near term, the long-term growth story remains intact, making it a reasonable hold for now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Cisco Systems, Inc. (CSCO) : Free Stock Analysis Report

Twilio Inc. (TWLO) : Free Stock Analysis Report