Thermon (NYSE:THR) Misses Q2 Revenue Estimates

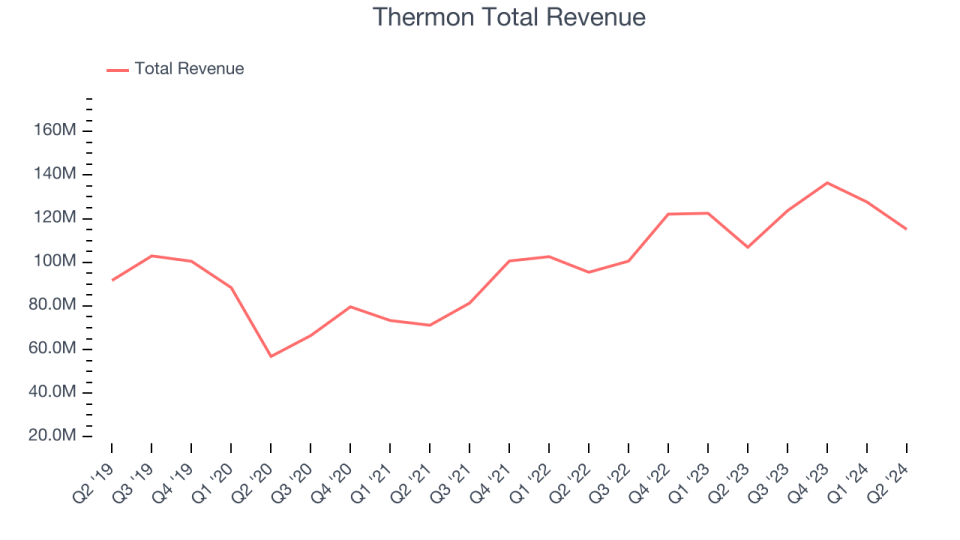

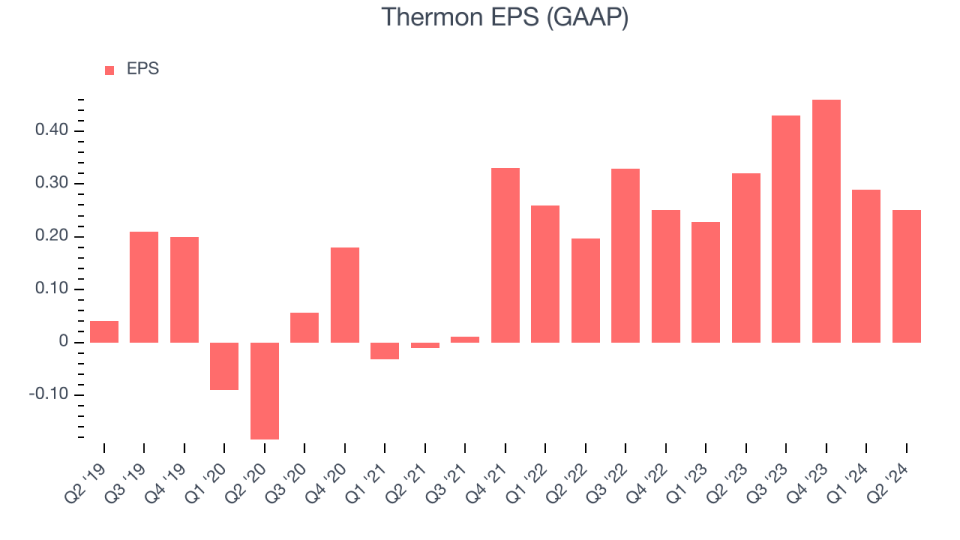

Industrial process heating solutions provider Thermon (NYSE:THR) missed analysts' expectations in Q2 CY2024, with revenue up 7.7% year on year to $115.1 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $540 million at the midpoint. It made a GAAP profit of $0.25 per share, down from its profit of $0.32 per share in the same quarter last year.

Is now the time to buy Thermon? Find out in our full research report.

Thermon (THR) Q2 CY2024 Highlights:

Revenue: $115.1 million vs analyst estimates of $116 million (small miss)

EPS: $0.25 vs analyst estimates of $0.21 (20.5% beat)

EBITDA guidance for the full year is $116 million at the midpoint, in line with analyst expectations

Gross Margin (GAAP): 43.8%, in line with the same quarter last year

EBITDA Margin: 20.1%, up from 16.9% in the same quarter last year

Free Cash Flow of $8.74 million, down 74.5% from the previous quarter

Market Capitalization: $988.1 million

"I am extremely proud of our strong execution during the first quarter, highlighted by favorable momentum in our diversified end markets, the successful integration and positive contribution from our Vapor Power acquisition, and disciplined financial management leading to solid free cash flow conversion," stated Bruce Thames, President and CEO of Thermon.

Creating the first packaged tracing systems, Thermon (NYSE:THR) is a leading provider of engineered industrial process heating solutions for process industries.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

A company's long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last five years, Thermon grew its sales at a weak 3.1% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Thermon's annualized revenue growth of 15% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Thermon's revenue grew 7.7% year on year to $115.1 million, missing Wall Street's estimates. We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates. This signals Thermon could be a hidden gem because it doesn't get attention from professional brokers.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Thermon has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.2%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Thermon's annual operating margin rose by 8.5 percentage points over the last five years, showing its efficiency has meaningfully improved.

In Q2, Thermon generated an operating profit margin of 11.9%, down 3 percentage points year on year. Since Thermon's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Thermon's EPS grew at a remarkable 13.2% compounded annual growth rate over the last five years, higher than its 3.1% annualized revenue growth. This tells us the company became more profitable as it expanded.

We can take a deeper look into Thermon's earnings to better understand the drivers of its performance. As we mentioned earlier, Thermon's operating margin declined this quarter but expanded by 8.5 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For Thermon, its two-year annual EPS growth of 34.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q2, Thermon reported EPS at $0.25, down from $0.32 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. We also like to analyze expected EPS growth based on Wall Street analysts' consensus projections, but there is insufficient data. This signals Thermon could be a hidden gem because it doesn't have much coverage among professional brokers.

Key Takeaways from Thermon's Q2 Results

We were impressed by how significantly Thermon blew past analysts' EPS expectations this quarter. On the other hand, its revenue unfortunately missed. Zooming out, we think this was still a mixed. The stock remained flat at $29.18 immediately following the results.

So should you invest in Thermon right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.