Synopsys Dips 18% in 3 Months: Should You Buy, Sell or Hold the Stock?

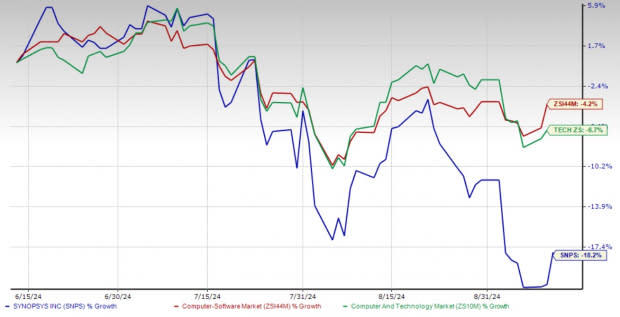

Synopsys Inc. SNPS has seen a sharp decline of more than 18% in its stock price over the past three months, underperforming both its industry and the broader technology sector. During this period, the Zacks Computer – Software industry declined 4.2%, and the Zacks Computer and Technology sector fell by 6.7%.

Several factors have contributed to this decline, including mounting fears over a potential U.S. recession and a slowdown in the company's growth within its key design automation segment. Despite these headwinds, Synopsys' long-term outlook remains positive due to its strategic moves like the pending acquisition of ANSYS and its strong positioning in the AI-driven semiconductor market.

But with all these factors in mind, should investors buy, sell or hold Synopsys stock?

3-Month Price Return Performance

Image Source: Zacks Investment Research

Slowing Growth in Synopsys' Design Automation Segment

Synopsys’ Design Automation segment, the backbone of its business, is showing signs of slowing growth. In the third quarter of fiscal 2024, revenues from this segment grew by 6% year over year, reaching $1.06 billion. While positive, this growth is significantly lower than the double-digit rates the company had been posting in prior years.

The slowdown in this critical segment raises concerns because Synopsys' Electronic Design Automation tools are fundamental to the semiconductor design process. Any deceleration in this area could signal challenges in maintaining the company's competitive edge. The decline can be attributed, in part, to economic uncertainties, as semiconductor companies cut on research and development spending due to fears of a potential recession.

This slowdown has become a key factor driving Synopsys' recent stock price decline and has left investors questioning whether the company can sustain its past growth trajectory.

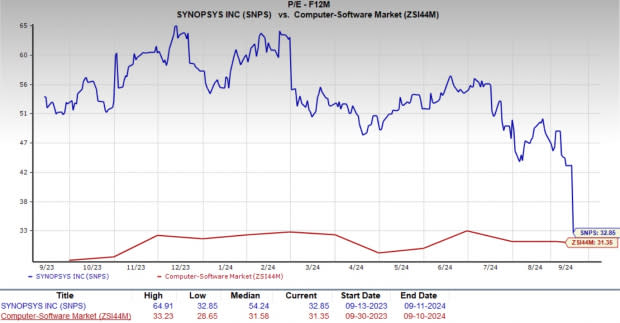

Valuation and Technical Indicators: A Concern for SNPS Stock

Despite the recent drop in Synopsys' stock price, the company still trades at a high forward 12-month price-to-earnings (P/E) ratio compared to the industry. The lofty P/E multiple reflects the high expectations for the company’s future growth. However, the deceleration in revenue growth in the Design Automation segment raises concern that the stock's current valuation is too high to be justified.

Image Source: Zacks Investment Research

Synopsys' technical indicators suggest that further downside could be ahead. The stock has been trading below the 50-day moving average, a key technical level often used by traders to gauge short-term momentum. The combination of a high valuation and negative technical indicators suggests that Synopsys may face more volatility in the near term.

50-Day Moving Average Signals Bearish Trend

Image Source: Zacks Investment Research

Synopsys’ Long-Term Growth Prospects Remain Robust

Despite the short-term challenges, Synopsys remains well-positioned for long-term growth. It is tapping into several major trends that should drive demand for its products over the next few years, particularly the growing need for artificial intelligence (AI)-driven semiconductor design.

The rise of AI has created an enormous demand for more sophisticated chips, which drives the need for advanced design tools. Synopsys excels in this area with its AI-powered tools like VSO.ai, which provide faster verification times and improved design accuracy. As companies continue to adopt AI, Synopsys stands to benefit from the growing demand for its design automation solutions.

Another major growth driver for Synopsys is its pending acquisition of ANSYS Inc. ANSS, a leader in engineering simulation. This acquisition, expected to close in the first half of 2025, will broaden Synopsys' product portfolio and open up new markets in system-level design.

ANSYS’ deep expertise in physics simulation will complement Synopsys’ electronics design capabilities, enabling the company to offer an integrated suite of tools for industries that require highly complex system simulations, such as automotive, aerospace and industrial sectors.

Synopsys’ Strong Competitive Positioning

In the highly competitive EDA and semiconductor space, Synopsys faces strong competition from industry heavyweights like Cadence Design Systems CDNS and Arm Holdings ARM.

Cadence is Synopsys' closest competitor in the design automation market and has made significant strides with its own AI-powered tools and cloud-based offerings. While Cadence poses a strong challenge, Synopsys holds an edge with its more diverse product portfolio, which spans both EDA tools and intellectual property (IP) offerings. This diversity allows Synopsys to target a broader range of customers and markets.

Arm Holdings, known for its dominance in mobile and Internet of Things chip architectures, presents a different kind of competition. While Arm focuses more on low-power applications, Synopsys has a stronger position in high-performance computing and advanced chip designs, particularly for AI and data center applications. This allows Synopsys to tap into high-growth markets that require cutting-edge semiconductor solutions.

Conclusion: Hold Synopsys Stock for Now

While Synopsys has experienced a sharp 18% decline in its stock price over the past three months, the company’s long-term prospects remain promising. The slowing growth in its Design Automation segment and its current bearish technical indicators present some near-term challenges. However, Synopsys' strong positioning in AI-driven semiconductor design and the potential boost from the pending ANSYS acquisition provide compelling reasons to hold on to the stock.

For current investors, holding Synopsys stock makes sense, given its leadership in key growth areas and its ability to innovate in semiconductor design. However, with the stock trading at a high valuation and negative technical signals looming, it may be wise to wait for signs of stabilization before considering adding more shares of this Zacks Rank #3 (Hold) company. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ARM Holdings PLC Sponsored ADR (ARM) : Free Stock Analysis Report

Synopsys, Inc. (SNPS) : Free Stock Analysis Report

Cadence Design Systems, Inc. (CDNS) : Free Stock Analysis Report

ANSYS, Inc. (ANSS) : Free Stock Analysis Report