Is SUN's Premium Valuation Justified? Time to Buy, Sell, or Hold?

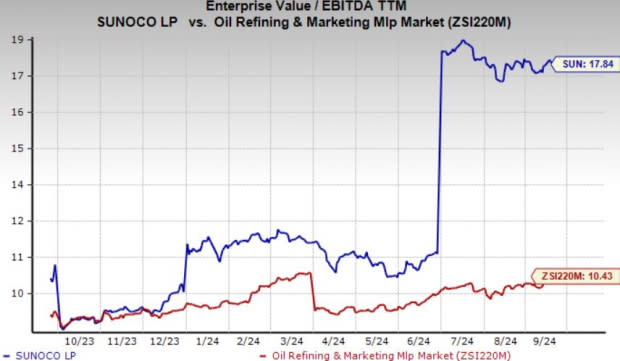

Sunoco LP SUN is currently considered expensive on a relative basis, with the stock trading at a 17.84x trailing 12-month enterprise value to earnings before interest, taxes, depreciation and amortization (EV/EBITDA), which is at a premium compared with the broader industry average of 10.43x. A premium valuation generally indicates that the market has strong confidence in the partnership’s prospects. However, this necessitates scrutiny to determine if this higher price is warranted.

Image Source: Zacks Investment Research

Therefore, a more thorough analysis is needed to determine whether SUN's premium valuation is justified based on its fundamentals, growth prospects and prevailing market conditions.

What Makes SUN’s Business Model so Resilient

Sunoco ranks among the leading independent fuel distributors in the United States, with an annual distribution of more than 8 billion gallons of fuel. The master limited partnership leverages its extensive midstream assets, including a pipeline network that spans more than 14,000 miles, to distribute fuel across more than 40 states. Sunoco's diverse customer base includes convenience stores, commercial customers and independent dealers, making it a key player in the nation's fuel distribution landscape.

In addition to its transportation networks, Sunoco operates 100 terminals located across the United States, Hawaii, Mexico and Puerto Rico, offering substantial product storage capacity. These diverse midstream assets contribute to the company's ability to generate stable cash flows, as they are secured with long-term contracts, minimizing exposure to commodity price fluctuations and reducing volume risks.

Permian JV and NuStar Deal Position SUN for Strong Growth

On July 16, Sunoco entered into a joint venture (JV) with Energy Transfer LP ET to consolidate their crude oil and produced water-gathering assets in the Permian, the most prolific basin in the United States. The JV, effective as of July 1, 2024, will immediately enhance the distributable cash flow per unit. This development is coupled with SUN’s stable business model and predictable fee-based cash flows, which suggests a promising outlook for the master limited partnership. Read our blog: Energy Transfer Forms JV With Sunoco in Permian Basin.

On May 3, Sunoco completed the $7.3 billion acquisition of NuStar Energy LP. With the acquisition of the leading independent liquids terminal and pipeline operator, SUN has diversified its operations and enhanced its credit profile. For more details, read our blog: Sunoco and NuStar Join Forces for a 7.3B All-Equity Merger.

Should Investors Pay the Premium for SUN’s Growth Potential?

The positive developments have led to SUN’s premium valuations, as investors have high expectations for the partnership’s prospects and profitability. Consequently, they are willing to pay a premium for the stock, believing it will outperform both its peers and the broader market in the coming months.

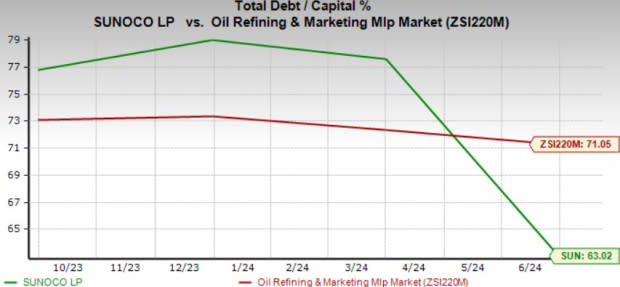

However, uncertainty surrounds the stock due to Sunoco's substantial reliance on debt, with a debt-to-capitalization of 63%. The industry average of 71.1% highlights the significant debt burden carried by other companies in the same sector, such as Western Midstream Partners LP WES, which has a debt-to-capitalization of 67.6%.

Image Source: Zacks Investment Research

Also, SUN's dependence on petroleum-based motor fuels could become a long-term risk because the world is slowly transitioning toward cleaner, alternative energy sources, like electric vehicles and hydrogen fuel. As more people and businesses adopt these alternative energy solutions, the demand for traditional petroleum-based fuels could decrease, potentially hurting SUN’s business over time.

The uncertainties are probably getting reflected in the stock’s year-to-date performance. Over the period, SUN has lost 6% compared with the 48.6% improvement of the industry’s composite stocks.

Image Source: Zacks Investment Research

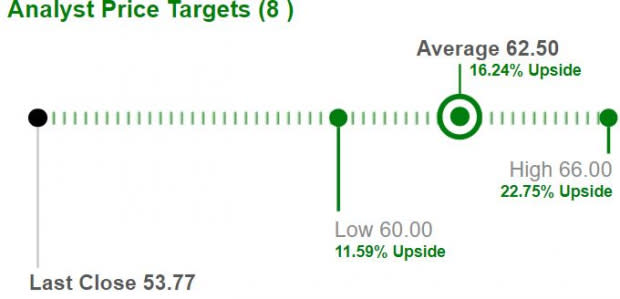

Despite these unfavorable business prospects, the partnership’s overall outlook remains positive. Leading brokers have raised SUN’s short-term price target by 16.2% from its recent closing price of $53.77, with the highest target set at $66, representing a potential upside of 22.8%.

Image Source: Zacks Investment Research

As a result, existing investors should hold onto their units to benefit from this upward price trend. However, for those considering a new investment in SUN, it might not be the best time. The stock, carrying a Zacks Rank #3 (Hold), is currently overvalued, so it’s wiser to wait for a more favorable entry point before investing. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sunoco LP (SUN) : Free Stock Analysis Report

Western Midstream Partners, LP (WES) : Free Stock Analysis Report

Energy Transfer LP (ET) : Free Stock Analysis Report