Can STM's Partnership With Qualcomm Subsidiary Push the Stock Higher?

STMicroelectronics STM announced its collaboration with Qualcomm Technologies, a subsidiary of Qualcomm Incorporated, for the next generation of industrial and consumer IoT solutions developed by edge AI.

This strategic collaboration will facilitate the blend of Qualcomm’s AI-powered wireless connectivity technologies, starting with Wi-Fi/Bluetooth/Thread combo system-on-a-chip with the microcontroller (MCU) ecosystem from STM.

Developers will enjoy smooth connectivity software integration into STM32 general-purpose MCUs, including software toolkits, enabling faster and broad adoption via STM’s worldwide sales and distributor channels.

STM’s Prospects Rides On Expanding Portfolio

Despite constant product releases and collaborations, STMicroelectronics shares have plunged 43.7% on a year-to-date basis, underperforming the Zacks Computer & Technology sector’s return of 22.8%.

Over the same time frame, it lagged behind industry peers NVIDIA NVDA, Amtech Systems ASYS and Texas Instruments TXN, shares of which have gained 148.1%, 37.4% and 18.4%, respectively. The industry has appreciated 103.6% year to date.

However, the recent launches is expected to help the STM stock recover.

STM’s introduction of the second-generation industrial microprocessors, the STM32MP2 series, to enable enhanced edge performance in smart factories, smart healthcare, smart buildings and smart infrastructure is a notable move for its Industrial end market.

The latest launch of ultra-low-power STM32 MCUs that can reduce energy consumption by up to 50% is a plus for its Industrial end. It reduces the frequency of battery replacements and the impact of discarded batteries, allowing designs to operate without batteries and using energy-harvesting systems like solar cells.

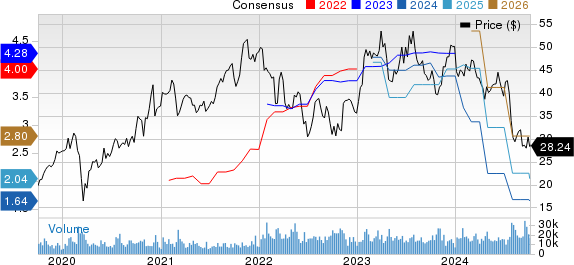

STMicroelectronics N.V. Price and Consensus

STMicroelectronics N.V. price-consensus-chart | STMicroelectronics N.V. Quote

STM’s recent introduction of ISM330BX 6-axis energy-efficient autonomous inertial measurement unit (IMU) built to last in industrial settings is considered a positive move.

This IMU integrates edge-AI processing, an analog hub for sensor expansion, and ST’s Qvar electric charge variations sensing designed to provide product-longevity assurance for energy-efficient industrial sensing and motion tracking applications.

STM's launch of ST Edge AI Suite, a consolidated collection of software tools uniquely created to enhance the development and deployment of embedded AI applications, is a major development.

Expanding the Automotive End Market to Aid STM’s Prospects

In the automotive space, STM’s introduction of a 6-axis module facilitates a cost-effective solution for functional safety applications, such as accurate positioning and navigation systems and digitally stabilizing cameras, LiDARs and radars is a notable development.

The release of the ASM330LHBG1 automotive 3-axis accelerometer and 3-axis gyroscope module with a safety software library that enables a cost-effective solution for functional safety applications is a plus.

STM’s Q3 and FY24 Guidance Not So Bright

For the third quarter of 2024, STM expects revenues of $3.25 billion at the midpoint, indicating a year-over-year decline of 26.7% and sequential growth of 0.6%. The Zacks Consensus Estimate is pinned at $3.22 billion. This indicates a year-over-year decline of 27.3%.

Gross margin is expected to be about 38% at the midpoint, impacted negatively by about 350 basis points, mainly due to the combination of product mix and sales price and higher unused capacity charges.

The consensus mark for earnings is pegged at 32 cents per share, suggesting a 41% decline in the past 60 days. This indicates a year-over-year decline of 72%.

Full-year 2024 revenues are expected in the range of $13.2-$13.7 billion, indicating a decline of about 22% at the midpoint compared with 2023. The gross margin is expected to be about 40%.

During the second half of 2024, STM expects a significant downturn in the Industrial market due to decreasing demand for industrial goods and a rapid drop in inventory throughout the supply chain.

Hence, it anticipates a delayed recovery in the Industrial end market and a lower-than-expected increase in Automotive end market revenues in the second half of the year versus the first half.

Zacks Ranks and Valuation

STM’s shares are cheap at this moment, as suggested by a Value Score of B.

The stock is trading with a forward 12-month Price/Sales of 1.82X compared with the industry’s 15.68X.

STM currently carries a Zacks Rank #4 (Sell), implying that investors should stay away from the stock.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Instruments Incorporated (TXN) : Free Stock Analysis Report

STMicroelectronics N.V. (STM) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Amtech Systems, Inc. (ASYS) : Free Stock Analysis Report