Southwest Airlines Gains 13.2% in 3 Months: What Should Investors Do?

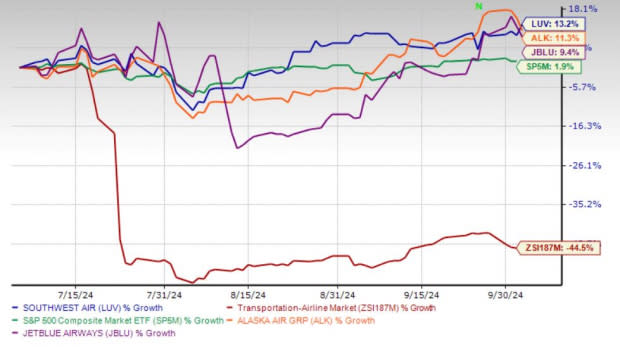

Shares of Dallas, TX-based airline heavyweight Southwest Airlines Co. (LUV) have had a good run of late, improving double digits over the past 90 days. The encouraging price performance resulted in LUV outperforming its industry in the said time frame, as well as the S&P 500, of which the airline is a key member. Additionally, LUV’s price performance compares favorably with that of fellow U.S. airline operators JetBlue Airways Corporation JBLU and Alaska Air Group, Inc. ALK in the same time frame.

Three-Month Price Comparison

Image Source: Zacks Investment Research

Currently trading at $30.51, the stock rebounded 39.25% from its 52-week low of $21.91 on Nov. 01, 2023. However, it still reflects a significant 13.27% discount from its 52-week high of $35.18, reached on Feb. 22, 2024.

Given the recent rally, the question that naturally arises is whether LUV stock can sustain its bullish price performance or should investors book profits now. Before that, let's delve deep to unearth the reasons behind this northward price movement.

LUV’s Improved Q3 View on Upbeat Summer Travel

LUV now anticipates its third-quarter revenues per available seat mile (RASM or unit revenues) to increase in the range of 2-3% on a year-over-year basis. This marks an improvement from the previous forecast of flat to down 2%. The upside in revenue performance was driven by the improving industry demand trends, along with the company's revenue management techniques.

Apart from the air travel demand strength, additional revenues in July related to the CrowdStrike CRWD induced disruptions across the industry also contributed to LUV’s top-line growth. The global technology outage on July 19, 2024, caused by security software provider CrowdStrike’s software update, has hit some of the major U.S. airlines, leading to multiple flight cancelations. LUV reaped the benefits from the troubles of its competitors’ flight cancelations.

For the remainder of 2024, LUV anticipates RASM to trend positive on a year-over-year basis.

Third-quarter capacity or available seat miles (ASMs) are still estimated to improve 2% from the year-ago reported figure.

Economic fuel cost per gallon for the third quarter is now expected to be in the range of $2.50-$2.60 (prior view: $2.60 to $2.70). Lower fuel costs should boost the company’s bottom line, as fuel expenses represent a key input cost for any transportation player.

Some Other Tailwinds Working in Favor of LUV Stock

Apart from issuing encouraging guidance, LUV also laid out an impressive roadmap for its growth and announced a new share buyback plan. As part of its growth strategy, LUV anticipates to deliver an estimated $500 million of run-rate cost savings in 2027. The company aims to achieve that by minimizing hiring, optimizing scheduling, improving corporate efficiency and capitalizing on supply chain opportunities. LUV also intends to upgrade its fleet and hopes to reach an average fleet age of five years in 2031. The airline intends to reduce average capital expenditures for aircraft to around $50 million through 2027.

LUV’s board of directors has authorized a new $2.5 billion share repurchase program. LUV has terminated and replaced its prior share repurchase program, authorized in May 2019, with the new share repurchase program.

Given this encouraging outlook, investors are keenly waiting for the third-quarter earnings releases of LUV, which is slated to be released on Oct. 24, 2024.

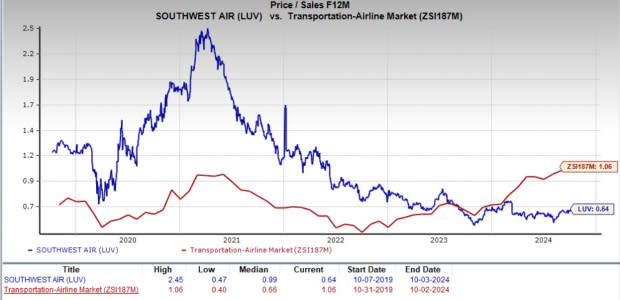

Impressive Valuation Picture for LUV Stock

From a valuation perspective, LUV is trading at a discount compared to the industry, going by its forward 12-month price-to-sales ratio. The reading is also below its median over the last five years. The company has a Value Score of B.

Image Source: Zacks Investment Research

Rising Expenses Weigh on Southwest Airlines Stock

A rise in labor and airport costs is also likely to dent bottom-line growth by resulting in a spike in operating expenses. Evidently, operating expenses were up 11.8% during the first half of 2024.

The surge in operating expenses was primarily caused by an increase in labor costs and fuel expenses. Expenses on salaries, wages and benefits increased 12.8% in the same period over 2022 actuals. Consolidated operating costs per available seat mile (excluding fuel and special items) rose 5.5% year over year to 11.86 cents in the first half of 2024.

For third-quarter 2024, LUV expects consolidated unit cost or cost per available seat mile (CASM), excluding fuel, oil and profit-sharing expenses, and special items, to increase 11-13% in the third quarter from the comparable period in 2023. For 2024, CASM, excluding fuel, oil and profit-sharing expenses, and special items, is anticipated to increase 7-8% from 2023.

Given the headwinds surrounding the stock, earnings estimates have been southbound, as shown below.

Image Source: Zacks Investment Research

To Conclude

It is understood that LUV stock is attractively valued, and upbeat air travel demand is contributing to its top line. However, investors should refrain from rushing to buy LUV now due to the headwinds that it faces.

Instead, they should monitor the company’s developments closely for a more appropriate entry point. For those who already own the stock, it will be prudent to stay invested. The stock’s Zacks Rank #3 (Hold) supports our thesis. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southwest Airlines Co. (LUV) : Free Stock Analysis Report

JetBlue Airways Corporation (JBLU) : Free Stock Analysis Report

Alaska Air Group, Inc. (ALK) : Free Stock Analysis Report

CrowdStrike (CRWD) : Free Stock Analysis Report