REV Group (NYSE:REVG) Reports Sales Below Analyst Estimates In Q2 Earnings, Stock Drops 12.9%

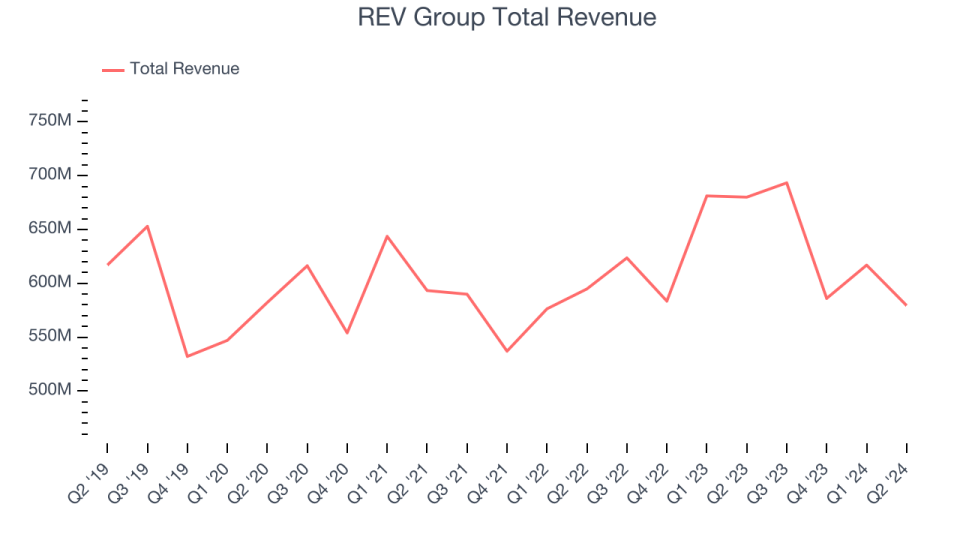

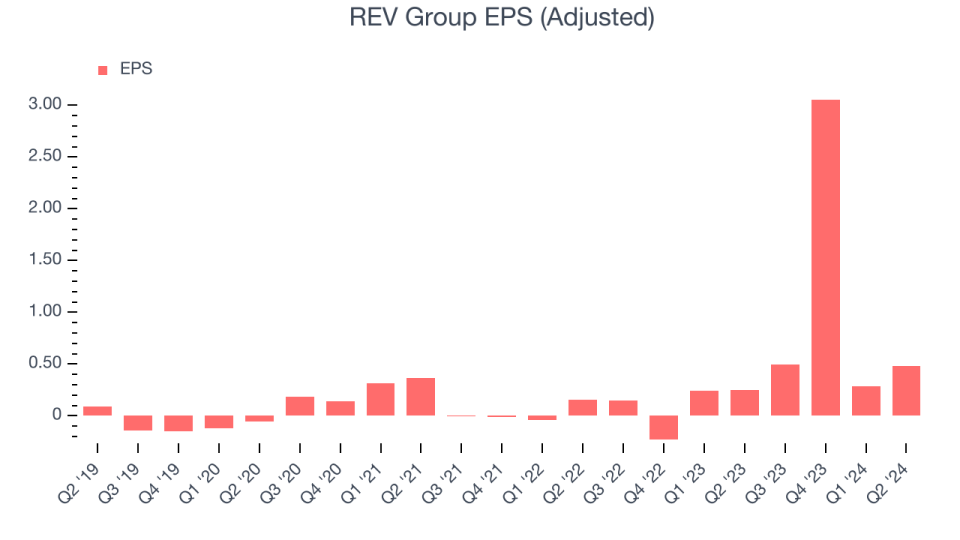

Speciality vehicle provider REV (NYSE:REVG) fell short of analysts’ expectations in Q2 CY2024, with revenue down 14.8% year on year to $579.4 million. The company’s full-year revenue guidance of $2.4 billion at the midpoint also came in 1.8% below analysts’ estimates. It made a non-GAAP profit of $0.48 per share, improving from its profit of $0.25 per share in the same quarter last year.

Is now the time to buy REV Group? Find out in our full research report.

REV Group (REVG) Q2 CY2024 Highlights:

Revenue: $579.4 million vs analyst estimates of $618.7 million (6.4% miss)

EPS (non-GAAP): $0.48 vs analyst estimates of $0.42 (13.6% beat)

The company dropped its revenue guidance for the full year to $2.4 billion at the midpoint from $2.45 billion, a 2% decrease

EBITDA guidance for the full year is $160 million at the midpoint, above analyst estimates of $157.7 million

Gross Margin (GAAP): 13.5%, up from 11.8% in the same quarter last year

EBITDA Margin: 7.8%, up from 5.8% in the same quarter last year

Free Cash Flow Margin: 1.5%, down from 8.3% in the same quarter last year

Market Capitalization: $1.57 billion

Offering the first full-electric North American fire truck, REV (NYSE:REVG) manufactures and sells specialty vehicles.

Heavy Transportation Equipment

Heavy transportation equipment companies are investing in automated vehicles that increase efficiencies and connected machinery that collects actionable data. Some are also developing electric vehicles and mobility solutions to address customers’ concerns about carbon emissions, creating new sales opportunities. Additionally, they are increasingly offering automated equipment that increases efficiencies and connected machinery that collects actionable data. On the other hand, heavy transportation equipment companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the construction and transport volumes that drive demand for these companies’ offerings.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. REV Group struggled to generate demand over the last five years as its sales were flat. This is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. REV Group’s annualized revenue growth of 3.8% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, REV Group missed Wall Street’s estimates and reported a rather uninspiring 14.8% year-on-year revenue decline, generating $579.4 million of revenue. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

REV Group was profitable over the last five years but held back by its large expense base. It demonstrated lousy profitability for an industrials business, producing an average operating margin of 1.9%. This result isn’t too surprising given its low gross margin as a starting point.

On the bright side, REV Group’s annual operating margin rose by 4.6 percentage points over the last five years

In Q2, REV Group generated an operating profit margin of 4.9%, up 1.2 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

REV Group’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. REV Group’s EPS grew at an astounding 533% compounded annual growth rate over the last two years, higher than its 3.8% annualized revenue growth. This tells us the company became more profitable as it expanded.

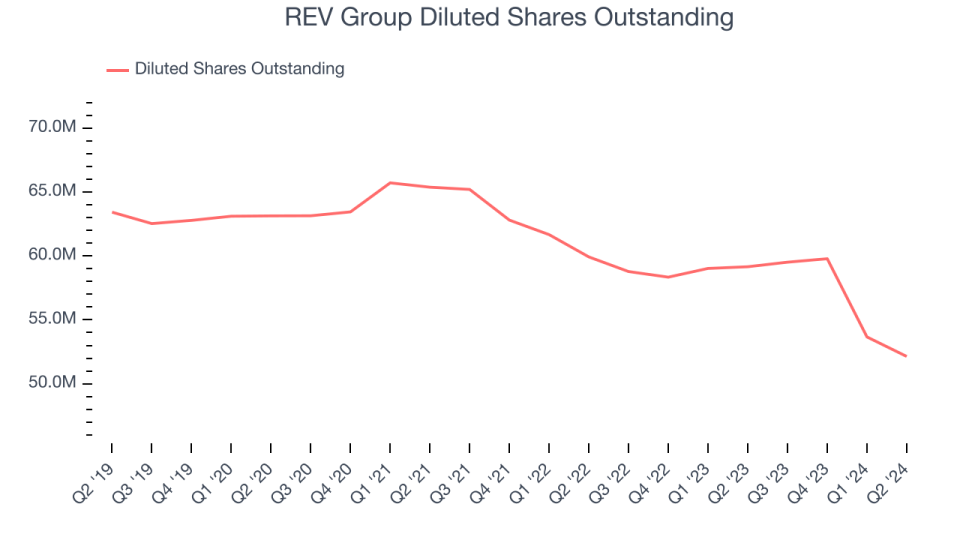

We can take a deeper look into REV Group’s earnings quality to better understand the drivers of its performance. REV Group’s operating margin has expanded 2 percentage points over the last two years while its share count has shrunk 13%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q2, REV Group reported EPS at $0.48, up from $0.25 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects REV Group to perform poorly. Analysts are projecting its EPS of $4.32 in the last year to shrink by 54.2% to $1.98.

Key Takeaways from REV Group’s Q2 Results

We enjoyed seeing REV Group exceed analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue unfortunately missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 12.9% to $26.32 immediately following the results.

REV Group may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.