Q2 Rundown: SPX Technologies (NYSE:SPXC) Vs Other Gas and Liquid Handling Stocks

Let’s dig into the relative performance of SPX Technologies (NYSE:SPXC) and its peers as we unravel the now-completed Q2 gas and liquid handling earnings season.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 11 gas and liquid handling stocks we track reported a mixed Q2. As a group, revenues missed analysts’ consensus estimates by 0.9%.

Stocks--especially those trading at higher multiples--had a strong end of 2023, but this year has seen periods of volatility. Mixed signals about inflation have led to uncertainty around rate cuts, and while some gas and liquid handling stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.7% since the latest earnings results.

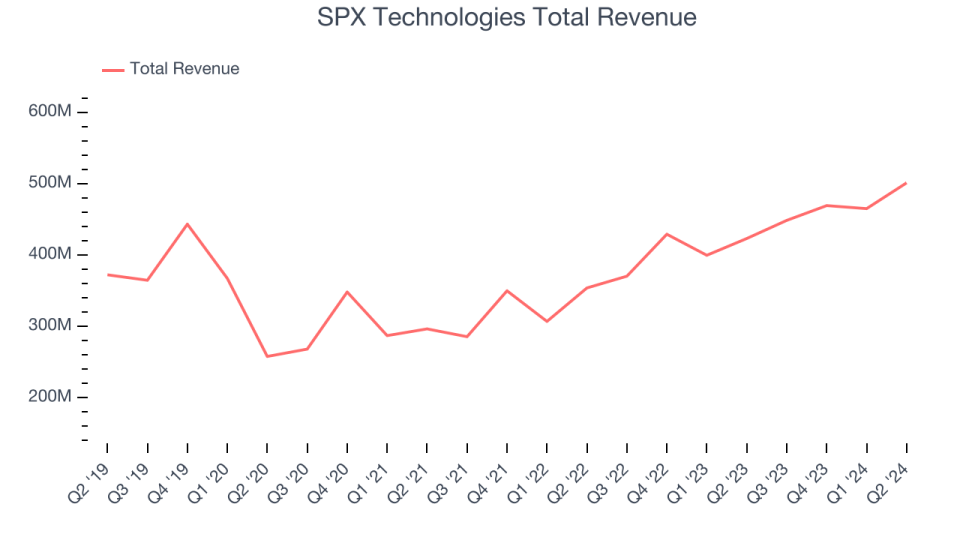

SPX Technologies (NYSE:SPXC)

SPX Technologies (NYSE:SPXC) is an industrial conglomerate catering to the energy, manufacturing, automotive, and aerospace sectors.

SPX Technologies reported revenues of $501.3 million, up 18.4% year on year. This print exceeded analysts’ expectations by 2.2%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ organic revenue estimates.

SPX Technologies scored the fastest revenue growth and highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 8.1% since reporting and currently trades at $154.74.

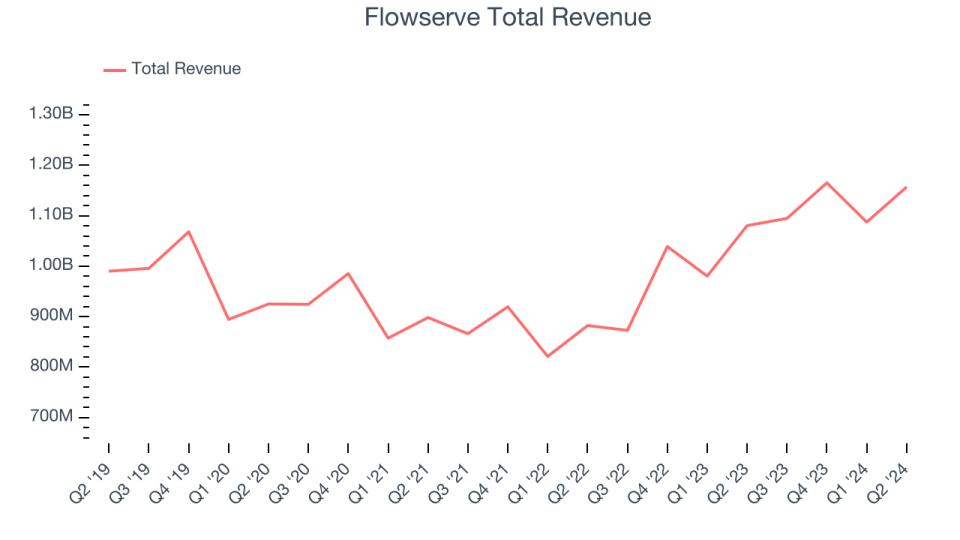

Best Q2: Flowserve (NYSE:FLS)

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE:FLS) manufactures and sells flow control equipment for various industries.

Flowserve reported revenues of $1.16 billion, up 7.1% year on year, outperforming analysts’ expectations by 2.4%. It was an exceptional quarter for the company with a solid beat of analysts’ earnings estimates.

Flowserve achieved the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 5.5% since reporting. It currently trades at $48.07.

Is now the time to buy Flowserve? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Gorman-Rupp (NYSE:GRC)

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE:GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

Gorman-Rupp reported revenues of $169.5 million, flat year on year, falling short of analysts’ expectations by 3.8%. It was a weak quarter for the company with a miss of analysts’ earnings estimates.

As expected, the stock is down 6.3% since the results and currently trades at $38.05.

Read our full analysis of Gorman-Rupp’s results here.

Parker-Hannifin (NYSE:PH)

Founded in 1917, Parker Hannifin (NYSE:PH) is a manufacturer of motion and control systems for a wide variety of mobile, industrial and aerospace markets.

Parker-Hannifin reported revenues of $5.19 billion, up 1.8% year on year, surpassing analysts’ expectations by 2%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and a decent beat of analysts’ earnings estimates.

The stock is up 14.4% since reporting and currently trades at $587.30.

Read our full, actionable report on Parker-Hannifin here, it’s free.

CECO (NASDAQ:CECO)

Started in a Cincinnati garage, CECO (NASDAQ:CECO) is a global provider of industrial air quality and fluid handling systems.

CECO reported revenues of $137.5 million, up 6.5% year on year, falling short of analysts’ expectations by 4%. Overall, it was a weak quarter for the company with a miss of analysts’ earnings estimates.

The stock is down 6.8% since reporting and currently trades at $27.98.

Read our full, actionable report on CECO here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.