Purple (NASDAQ:PRPL) Reports Sales Below Analyst Estimates In Q2 Earnings

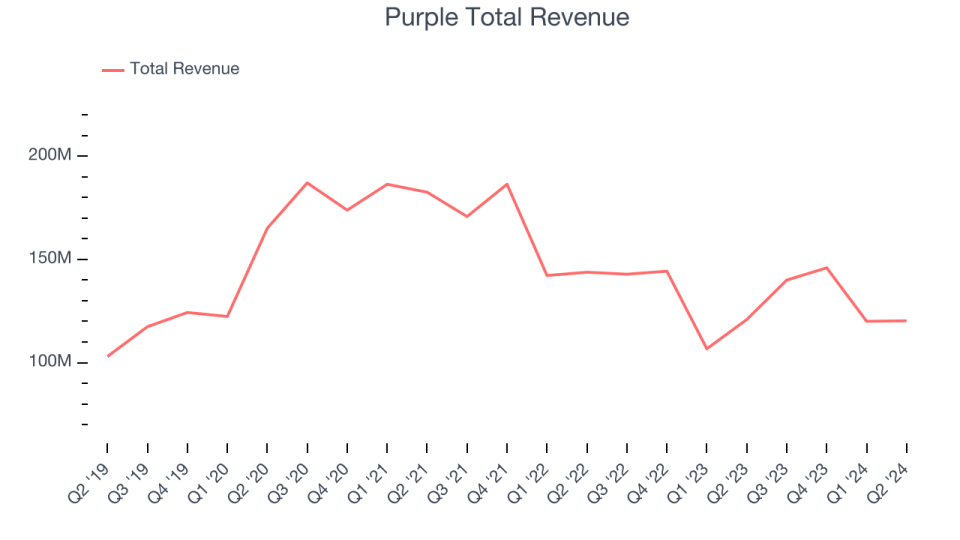

Bedding and comfort retailer Purple (NASDAQ:PRPL) missed analysts' expectations in Q2 CY2024, with revenue flat year on year at $120.3 million. The company's full-year revenue guidance of $500 million at the midpoint also came in 8.1% below analysts' estimates. It made a non-GAAP loss of $0.13 per share, improving from its loss of $0.36 per share in the same quarter last year.

Is now the time to buy Purple? Find out in our full research report.

Purple (PRPL) Q2 CY2024 Highlights:

Revenue: $120.3 million vs analyst estimates of $128.3 million (6.3% miss)

EPS (non-GAAP): -$0.13 vs analyst estimates of -$0.11

The company dropped its revenue guidance for the full year from $550 million to $500 million at the midpoint, a 9.1% decrease

Gross Margin (GAAP): 40.7%, up from 31.8% in the same quarter last year

Adjusted EBITDA Margin: -3.4%, up from -15.3% in the same quarter last year

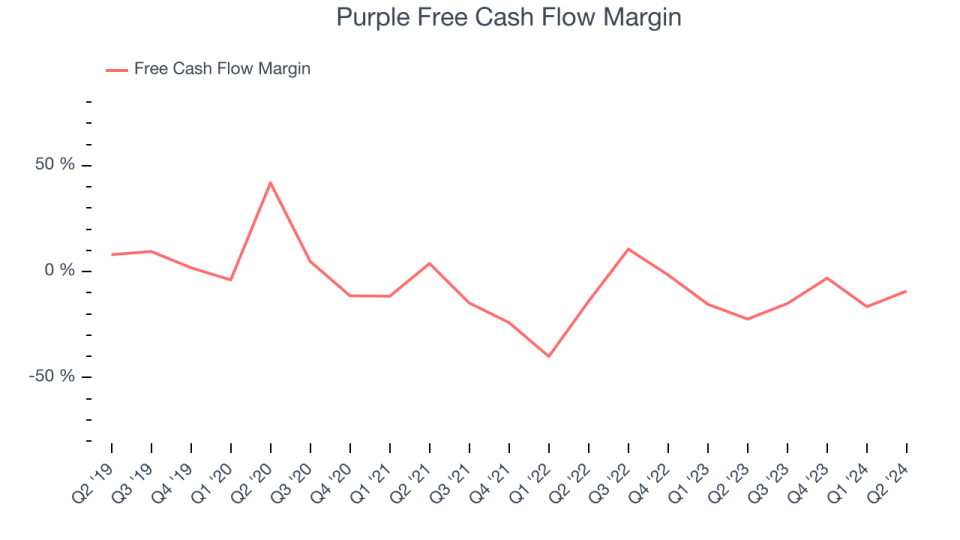

Free Cash Flow was -$11.02 million compared to -$19.85 million in the previous quarter

Market Capitalization: $134.4 million

"Our second quarter results underscore the progress we've made enhancing the financial profile of the Company," said Chief Executive Officer Rob DeMartini.

Founded by two brothers, Purple (NASDAQ:PRPL) creates sleep and home comfort products such as mattresses, pillows, and bedding accessories.

Home Furnishings

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Purple's 9.4% annualized revenue growth over the last five years was sluggish. This shows it failed to expand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Purple's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 9.6% annually.

This quarter, Purple missed Wall Street's estimates and reported a rather uninspiring 0.5% year-on-year revenue decline, generating $120.3 million of revenue. Looking ahead, Wall Street expects sales to grow 8.2% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Purple's demanding reinvestments to stay relevant have drained its resources. Its free cash flow margin was among the worst in the consumer discretionary sector, averaging negative 8.4%.

Purple burned through $11.02 million of cash in Q2, equivalent to a negative 9.2% margin. The company's cash burn decreased meaningfully year on year, showing it managed its cash more conservatively.

Key Takeaways from Purple's Q2 Results

We struggled to find many strong positives in these results. Its full-year revenue guidance missed, and its sales and EPS fell short of Wall Street's estimates. Overall, this quarter could have been better. The stock remained flat at $1.18 immediately following the results.

So should you invest in Purple right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.