Post Holdings Surges 31% YTD: What Lies Ahead for the Stock?

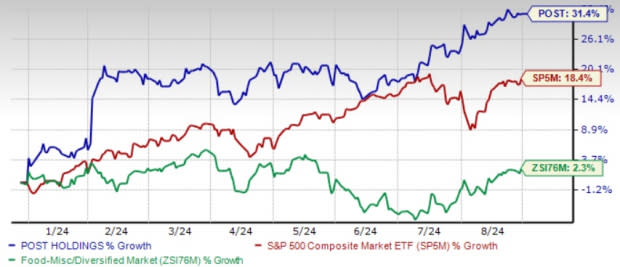

Post Holdings, Inc. POST has demonstrated impressive performance in the stock market this year. With a year-to-date (YTD) gain of 31.4%, POST has significantly outperformed the Zacks Food - Miscellaneous industry's growth of 2.3%. It has also surpassed the broader Consumer Staples sector, which increased 9.1% and the S&P 500, which grew 18.4% in the same period.

Closing at $115.77 on Friday, the stock stands close to its recently achieved 52-week high of $117.24, indicating impressive momentum.

In the past 30 days, the Zacks Consensus Estimate for earnings for the current fiscal year has risen 4.2% to $5.95 per share. The consensus mark implies a growth of 11.4% from the year-ago level, highlighting the company’s potential. The consensus estimated figure for the next fiscal year indicates year-over-year growth of 5.9%.

The Zacks Consensus Estimated figures for sales imply an increase of 12.7% and 1.2% for the current and next fiscal year, respectively.

The question that arises here is whether it is prudent to buy POST’s shares after the recent rally. Let’s take a look at the company’s underlying opportunities for growth and challenges that could impact its future trajectory.

Image Source: Zacks Investment Research

Uncovering the Opportunities for POST

The leading consumer-packaged goods company is reaping the benefits attributed to several factors, including strategic acquisitions, effective cost management and strong operational performance despite challenging market conditions. The company's ability to navigate inflationary pressures and enhance its portfolio through acquisitions and strategic investments has contributed to this bullish momentum.

Post Holdings has been benefitting from carryover pricing and operational efficiencies, particularly in the pet food and grocery divisions, which have been supported by strong manufacturing capabilities. This trend continued into the third quarter of fiscal 2024, as evidenced by year-over-year increases in both top and bottom lines’ performance.

The company is capitalizing on the robust performance of the Post Consumer Brands segment, with sales increasing 15.7% year over year in the third quarter of 2024. POST’s grocery business gained from carryover pricing and strong operating cost performance. The pet food business remained stable and consistent across all brands, with strong manufacturing performance being a key contributor to its results.

Strategic acquisitions have played a crucial role in expanding Post Holdings' market reach and strengthening its market position. Notable acquisitions in 2023, including Perfection Pet a portion of The J. M. Smucker Company’s pet food business and Deeside Cereals, have significantly diversified the company's revenue streams and enhanced its portfolio. These acquisitions have been pivotal in driving growth and reinforcing its competitive edge in the consumer packaged goods sector.

Understanding the Roadblocks for POST

While the company’s performance remains strong, Post Holdings is not without its difficulties in the current economic landscape. Increased SG&A costs, ongoing inflationary pressures, heightened competition and a downturn in the Refrigerated Retail Business pose notable obstacles. Addressing these issues will require careful management and strategic foresight to sustain growth and maintain a competitive edge.

Post Holdings’Refrigerated Retail segment recorded a 7.1% decline in net sales in third-quarter 2024. This segment saw a 0.5% decrease in volumes, with average net prices falling as a result of increased trade promotions and a shift in the portfolio toward dinner sides. The segment's adjusted EBITDA dropped 37%, reflecting the impact of lower net pricing and higher selling costs compared to the previous year.

POST’s Premium Valuation

With the stock steadily ticking up, the company is currently trading at a forward 12-month P/E multiple of 18.47X, exceeding the industry average of 16.61X. Currently, POST’s stock valuation seems pricey. Investors should carefully assess whether the company can continue to deliver results that justify the premium valuation, particularly in a potentially volatile market environment.

We believe investors should wait for a better entry point for Post Holdings, which currently carries a Zacks Rank #3 (Hold).

3 Staple Stocks to Consider

Here, we have highlighted three better-ranked food stocks, namely, The Chef's Warehouse CHEF, Pilgrim’s Pride PPC and Ollie's Bargain Outlet OLLI.

The Chef’s Warehouse, which engages in the distribution of specialty food products, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

CHEF has a trailing four-quarter earnings surprise of 33.7%, on average. The Zacks Consensus Estimated figure for The Chef’s Warehouse’s current fiscal year sales and earnings indicates growth of 9.7% and 12.6%, respectively, from the year-ago reported numbers.

Pilgrim’s Pride, which produces, processes, markets and distributes fresh, frozen and value-added chicken and pork products, currently sports a Zacks Rank #1. PPC delivered a positive earnings surprise of 27.3% in the trailing four quarters, on average.

The Zacks Consensus Estimated figure for Pilgrim’s Pride’s current financial-year earnings indicates growth of 183.43%, respectively, from the prior-year reported level.

Ollie's Bargain, the extreme-value retailer of brand-name merchandise, currently carries a Zacks Rank #2 (Buy). OLLI has a trailing four-quarter earnings surprise of 7.9%, on average.

The Zacks Consensus Estimated figure for Ollie's Bargain’s current financial-year sales and earnings indicates a rise of around 8.1% and 12.71%, respectively, from the year-earlier levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pilgrim's Pride Corporation (PPC) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

Post Holdings, Inc. (POST) : Free Stock Analysis Report

Ollie's Bargain Outlet Holdings, Inc. (OLLI) : Free Stock Analysis Report