PLMR Stock Near 52-Week High: Should You Add it to Your Portfolio Now?

Shares of Palomar Holdings PLMR closed at $97.48 on Wednesday, near a 52-week high of $100.29. New business, strong premium retention rates for existing business and renewals of existing policies, better pricing and effective capital deployment are driving shares higher.

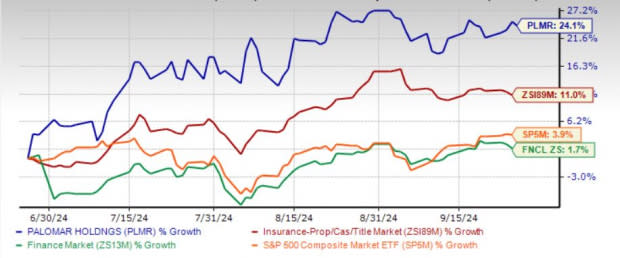

Shares of PLMR have gained 20% in the past three months, outperforming the industry’s growth of 11.1%, the Finance sector’s increase of 1.5% and the Zacks S&P 500 composite’s increase of 3.8%.

PLMR shares are trading well above the 50-day moving average, indicating a bullish trend.

PLMR Stock vs Industry, Sector, S&P 500 in 3 Months

Image Source: Zacks Investment Research

Average Target Price for PLMR Suggests an Upside

Based on short-term price targets offered by six analysts, the Zacks average price target is at $105.50 per share. The average suggests a potential 8.2% upside from Wednesday’s closing price.

PLMR’s Favorable Return

Palomar’s trailing 12-month return on equity was 20.8%, which came ahead of the industry average of 8%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders.

Also, the return on invested capital has been 19.2% over the trailing 12 months, outperforming the industry average of 6.1%. The company has raised its capital investment significantly, reflecting PLMR’s efficiency in utilizing funds to generate income.

Upbeat Analyst Sentiments

All six analysts covering the stock have raised estimates for 2024 and five of the six analysts have raised the same for 2025 over the past 60 days. The consensus estimate for 2024 and 2025 has moved 4.1% and 7.6%, respectively, in the past 60 days.

The Zacks Consensus Estimate for 2024 implies a 30.9% year-over-year increase, while the same for 2025 suggests a 20.1% increase. We estimate the 2026 bottom line to witness a three-year CAGR of 17.2%.

Factors Favoring Palomar

Increased volume of policies written across the lines of business, strong retention rates, strategic expansion of products’ geographic and distribution footprint and new partnerships should drive premiums for Palomar. We estimate 2026 gross premiums written to witness a three-year CAGR of 15.3%.

Net investment income is poised to benefit from high-quality fixed-income securities, a higher average balance of investments, and an increase in fixed-income yields. Though the Fed had lowered the interest rate by 50 basis points in its recently concluded FOMC meeting, PLMR’s solid investment portfolio should help 2026 investment income to rise at a three-year CAGR of 59.5%.

Palomar’s fee-generating PLMR-FRONT should fuel growth in the medium term. The addition of the fee-based revenue stream to the business is expected to strengthen its earnings base.

This insurer’s prudent underwriting expertise is reflected in its combined ratio, which has been under 95% since 2017, except in 2020. PLMR’s risk transfer strategy lowers exposure to major events, which, in turn, reduces earnings volatility.

Palomar boasts a debt-free balance sheet. Its continued operational excellence helps it maintain a strong capital position. As part of wealth distribution to shareholders, PLMR engages in share buybacks and has $43.5 million available for future repurchases.

Banking on operational strength, Palomar expects to generate adjusted net income between $110 million and $115 million in 2024.

PLMR Capital Shares Are Overvalued

PLMR shares are trading at a price-to-book multiple of 4.50, higher than the industry average of 1.60.

Shares of other insurers like Horace Mann Educators HMN, Lemonade LMND and Employers Holdings Inc. EIG are trading at a multiple lower than the industry average.

Conclusion

Palomar is poised to grow on the strength of its solid product portfolio as well as geographic expansion, appointment of new producers, strategic partnerships with other insurance carriers and rate increases. The fee-generating PLMR-FRONT should drive growth in the medium term and strengthen its earnings base. To prevent erosion of profitability, PLMR utilizes reinsurance in order to limit its exposure to losses and enable it to underwrite policies with sufficient limits to meet policyholder needs. All these together instill confidence in this specialty insurer.

Thus, despite premium valuation, this Zacks Rank #1 (Strong Buy) insurer is worth adding to an investor’s portfolio.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Employers Holdings Inc (EIG) : Free Stock Analysis Report

Horace Mann Educators Corporation (HMN) : Free Stock Analysis Report

Palomar Holdings, Inc. (PLMR) : Free Stock Analysis Report

Lemonade, Inc. (LMND) : Free Stock Analysis Report