Pilgrim's Pride Growth Playbook: Why is PPC a Solid Consumer Bet?

Pilgrim's Pride Corporation PPC has built a strong foundation in the chicken protein market. By diversifying its portfolio, focusing on branded offerings and building strategic partnerships, PPC is positioned to drive sustained growth. These strategies enable the company to capitalize on evolving consumer preferences and strengthen its competitive edge.

Focus on key customers is a pathway for refining its portfolio and creating competitive advantages over its peers. The company’s Case Ready business in the United States has experienced growth through strengthening key customer partnerships in retail. This growth has been driven by differentiated offerings, effective promotional activities and a focus on innovation, helping to maintain a competitive edge in the market.

Segments like Big Bird and Small Bird also outperformed the market with customized offerings to key customers in the second quarter of fiscal 2024. Innovation in Prepared Foods also expanded marketplace presence through branded, value-added items across retail and food service sectors during the same time frame.

PPC’s Strategic Attempt Bodes Well

Pilgrim's Pride has been reaping the benefits of substantial investments in expansion and operational efficiencies. In the United States, the protein conversion team successfully ramped up production at the new Douglas facility in South Georgia, driven by strong customer demand. Growth in the pet food category has created additional opportunities, leading to the expansion of the protein conversion facility at Sumter to capitalize on market potential.

In Europe, the company continues to make strides in profitability by optimizing the product mix through key customer partnerships and diversifying the portfolio with branded offerings and innovation. In Mexico, on the other hand, improved market balance and consistent execution drove double-digit sales growth with key customers in the second quarter of fiscal 2024. Enhanced operational efficiencies and a favorable market environment for private brands have been supporting overall performance.

In the second quarter of 2024, Pilgrim’s Pride experienced a notable improvement in financial performance, driven by a reduction in the cost of sales. This was due to decreased grain input costs and enhanced operational efficiencies. The company also benefited from a recovery in the commodity chicken market. These factors collectively contributed to stronger margins and overall profitability, especially in key segments such as Big Bird, where the reduction in production costs played a crucial role in driving financial success.

Pilgrim's Pride has sustained positive momentum in the food service distribution channel, with increased volume and sales across both commercial and non-commercial subchannels in the second quarter. The quick-service restaurant (QSR) category drove most of the volume growth, reflecting consumers' preference for affordable meal options. This robust performance highlights the company's resilience and effectiveness in catering to a diverse customer base in the food service industry.

What’s More for PPC Stock?

The focus on branded offerings, particularly through successful product lines like Just Bare and Pilgrim’s, has been instrumental in capturing consumer interest and growing the company’s footprint in the market. Additionally, Pilgrim's Pride’s diversified portfolio, which includes value-added and prepared foods, has been strategically designed to align with shifting consumer preferences, thereby driving incremental growth and reinforcing its market position.

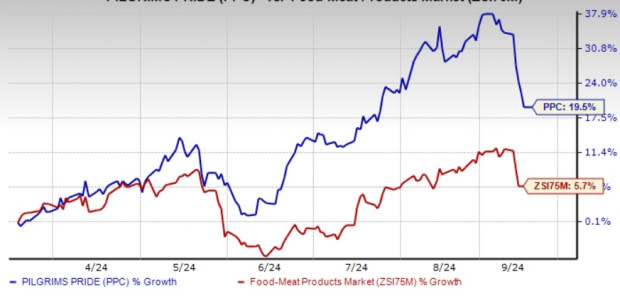

Buoyed by the aforesaid initiatives, PPC is well-poised for long-term growth objectives. Further, shares of this Zacks Rank #1 (Strong Buy) company have gained 19.6% over the past six months, outpacing the industry’s growth of 5.7%.

Image Source: Zacks Investment Research

Three Other Stocks to Consider

Here, we have highlighted three other top-ranked food stocks, namely, The Chef's Warehouse CHEF, Ollie's Bargain Outlet OLLI, and Flowers Foods FLO.

The Chef’s Warehouse, which engages in the distribution of specialty food products, currently sports a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

CHEF has a trailing four-quarter earnings surprise of 33.7%, on average. The Zacks Consensus Estimated figure for The Chef’s Warehouse’s current fiscal year sales and earnings indicates growth of 9.7% and 12.6%, respectively, from the year-ago reported numbers.

Ollie's Bargain, the extreme-value retailer of brand-name merchandise, currently carries a Zacks Rank #2 (Buy). OLLI has a trailing four-quarter earnings surprise of 7.9%, on average.

The Zacks Consensus Estimated figure for Ollie's Bargain’s current financial-year sales and earnings indicates a rise of around 8.7% and 12.71%, respectively, from the year-earlier levels.

Flowers Foods, one of the largest producers of packaged bakery foods in the United States, currently carries a Zacks Rank #2. FLO has a trailing four-quarter earnings surprise of 1.9%, on average.

The Zacks Consensus Estimate for Flowers Foods’ current financial-year sales and earnings indicates growth of 0.9% and 5%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

Pilgrim's Pride Corporation (PPC) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

Ollie's Bargain Outlet Holdings, Inc. (OLLI) : Free Stock Analysis Report