Nordstrom (JWN) Gains 67% in a Year: Should You Buy or Hold the Stock?

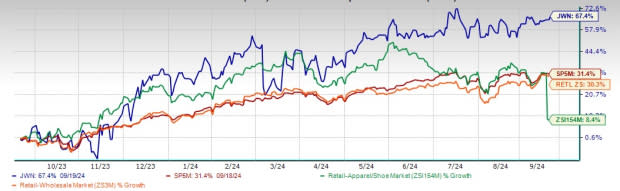

Shares of Nordstrom, Inc. JWN have surged 67.4% in the past year, outperforming the Zacks Retail - Apparel and Shoes industry’s 8.4% decline, the broader Retail-Wholesale sector’s 30.3% rise and the S&P 500 index’s 31.4% growth.

Its strategic efforts are on track. JWN is focused on driving the Nordstrom banner's growth, optimizing operations and building momentum at Rack. Digital efforts are also underway.

Currently priced at $22.91, the JWN stock is trading at 4.7% to its 52-week high of $24.03, reached on July 17, 2024. However, it is trading at a 77.9% premium to its 52-week low mark.

Strategies Support JWN’s Growth

JWN has been making notable efforts to drive efficiency and enrich the customer experience. The company is redefining its flagship brand to give it a trendy look, offering a style-driven and top-quality assortment. Increased focus on distribution capabilities and improved connectivity of physical and digital inventory are other tailwinds.

JWN's Stock Performance

Image Source: Zacks Investment Research

Nordstrom has been expanding its Rack banner, by increasing the brand penetration. It looks to strengthen Rack’s productivity throughout its network, reduce transportation costs and delivery times and enhance services via faster delivery. The company continues to focus on introducing more premium brands at Rack, better assortment and increased brand awareness. The Rack banner's digital channel is a differentiator to the off-price retail.

JWN has been making efforts to change the storage and access of data. This transformational change looks to improve data access and analysis capabilities, hence enhancing the ability to leverage generative AI solutions and services at a higher pace. In the most recent quarter, digital momentum continued with sales growth of 6% year over year. Growth at nordstrom.com was backed by an increase in the assortment across a balance of price points, improvements in search and discovery and high in-stock rates of its fastest-turning items.

Recently, a special committee of the board of directors said that it had received a proposal from Erik and Pete Nordstrom, members of the Nordstrom family, along with El Puerto de Liverpool, to buy the entire outstanding shares of the company, except shares held by them. This $3.8-billion buyout offer looks to take the fashion retailer private.

Long-Term Strategy to Benefit JWN

Nordstrom is focused on its long-term strategy, which builds on its market strategy to capitalize on its digital-first platform to better serve customers, gain market share and deliver profitable growth. It concentrates on winning in the most important markets, expanding the reach of Nordstrom Rack and enhancing its digital velocity.

JWN’s closer-to-you strategy, which aims to link stores and services to expedite deliveries, expand online offerings and adding cheaper merchandise at its Rack off-price stores, bodes well. Such catalysts aim at generating $2 billion in revenues in the long term.

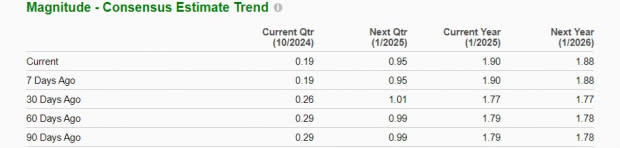

JWN’s Solid Earnings Estimate Revisions

Image Source: Zacks Investment Research

the positive sentiments regarding the stock, the Zacks Consensus Estimate for fiscal 2024 and 2025 has been northbound. In the past 30 days, the consensus estimate for earnings per share (EPS) for the current fiscal year has been revised 6.1% to $1.90 and 5.6% to $1.88 for fiscal 2025.

JWN Stock’s Valuation

Nordstrom stock is trading at an attractive valuation relative to the industry. Going by the price/earnings ratio, the JWN stock is currently trading at 12.17 on a forward 12-month basis, lower than 15.19 of the industry.

Image Source: Zacks Investment Research

Final Words on JWN Stock

Nordstrom’s robust strategies, including sturdy momentum at its Rack banner and digital endeavors, position it well for long-term growth. Its long-term growth strategies further demonstrate strength. Solid upward revisions in earnings estimates and attractive valuation for the stock seem encouraging. The company currently sports a Zacks Rank #1 (Strong Buy).

Other Key Picks

We have highlighted three other top-ranked stocks, namely Abercrombie ANF, Boot Barn BOOT and Deckers DECK.

Abercrombie & Fitch, a leading casual apparel retailer, presently flaunts a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie’s current financial-year sales indicates growth of 13.1% from the year-ago figure. ANF delivered an earnings surprise of 16.8% in the last reported quarter.

Boot Barn, a leading footwear, apparel and accessories retailer, currently sports a Zacks Rank of 1. BOOT delivered an average earnings surprise of 7.1% in the trailing four quarters.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales indicates growth of 11.6% from the year-ago figure.

Deckers, a footwear and accessories dealer, carries a Zacks Rank #2 (Buy) at present. DECK delivered an average earnings surprise of 47.2% in the trailing four quarters.

The Zacks Consensus Estimate for Deckers’ current financial-year sales indicates growth of 11.5% from the year-ago figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report