The U.S.-China trade dispute may be top of mind for most investors, but it’s far from the only risk weighing on markets.

Signs of U.S. growth going by the wayside began even before the latest ramp-up of trade tensions ensued mid-May. The confluence of concerns could well be cues toward a large-scale slowdown both in markets and in the broader economy, according to at least one strategist.

“Durable goods, capital spending and Markit PMIs were disappointing last week. All reflect April data, which means it weakened before the re-escalation of trade tensions,” Morgan Stanley analyst Michael Wilson wrote in a note Tuesday (emphasis his own). “In addition, numerous leading companies may be starting to throw in the towel on the second half rebound.”

Last week, the Census Bureau reported that orders for durable goods – manufactured products meant to last at least three years – declined more-than-expected in April. The report added fuel to the notion that the domestic industrial sector – which is especially trade sensitive – was dropping in lockstep with that of other global economies.

Meanwhile, IHS Markit last week reported that business activity in the U.S. manufacturing sector dropped to a near 10-year low in May. The typically more resilient U.S. services sector slumped to a three-year low, nearly matching the softness in manufacturing. Taken together, the composite purchasing managers’ index measure fell to 50.9, hobbling just above the minimum level of 50 required to indicate expansion.

“Such a low reading on services and the composite measures have not been this low since the great recession,” Wilson said.

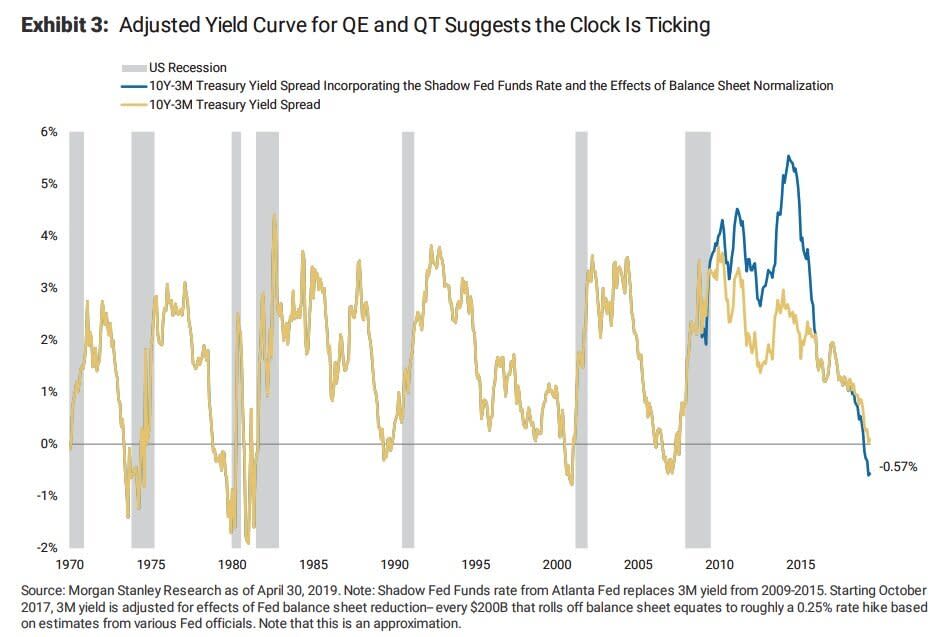

Yield curve inversion

Data from the bond market have flashed similar warning signs.

The brief inversion of the 10-year and 3-month Treasury yields in March triggered a wave of panic among investors. Many view a dip in yields of longer-term U.S. Treasurys below their shorter-term counterparts as a recessionary signal, as it suggests investors have a dimmer outlook for future growth.

But when viewed from another angle, the distress signals from fixed income securities actually came much earlier.

“Adjusting the yield curve for QE and QT shows a persistent inversion for the past ~6 months, suggesting recession risk is higher than normal,” Wilson said.

In other words, based on Morgan Stanley’s analysis, adjusting for the effects of the Federal Reserve’s large-scale asset purchases or reductions shows the downward slope in the yield curve began much sooner than many investors realized.

“The adjusted yield curve inverted last November and has remained in negative territory ever since, surpassing the minimum time required for a valid meaningful economic slowdown signal,” Wilson said. “It also suggests the ‘shot clock’ started 6 months ago, putting us ‘in the zone’ for a recession watch.”

Wilson noted that the initial adjusted curve inversion took place about the same time that the trade truce between the U.S. and China took place in early December – meaning the inversion persisted even amid positive trade rhetoric at the start of the year.

“We think this means the U.S. economic slowdown and rising recession risk is happening regardless of the trade outcome,” Wilson said.

Wilson, among Wall Street’s most bearish strategists, carries a bear-case 2,400 price target for the S&P 500 in 2019, and an upside bull case target of 3,000. His base case price target is 2,750, or 2.7% below Friday’s closing prices.

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Read more from Emily:

Tech companies like Lyft want your money – not ‘your opinion’

Levi Strauss shares jump more than 30% above IPO price at open

Facebook sued by Trump administration for alleged ‘discriminatory’ ad practices

Boeing 737 Max groundings ‘pressure’ U.S. economic data: Wells Fargo

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.