Millennials have more education under their belts than previous generations. But the hard reality is that they are lagging behind their parents’ and grandparents’ generations when it comes to wealth accumulation.

The Peter G. Peterson Foundation commissioned Brookings Institution’s report, How Will Retirement Saving Change by 2050?, which compared the median net worth among millennial households who were 25 to 35 years old in 2016 to that of baby boomers who were the same age in 1995. The difference is stark: net worth was $18,200 in 2016, vs. $31,273 two decades ago – a difference of 41%.

A notable advantage for millennials (defined in the report as those born between 1981 and 1996) is their level of education. According to the Brookings report, “over 60% of adult Millennials have attended at least some college, compared to 46% of the baby boomer generation when they were the same age. Rising educational attainment among women drives this difference.” And, generally speaking, more education will make it easier to save for retirement (of course, it also generally means more student loan debt).

Putting millennials at a disadvantage, though, is an accident of timing. The Great Recession that lasted from 2007 to 2009 handicapped the start of people’s careers for this generation and they still haven’t recovered.

“The weak job market and low overall labor force participation that existed at the beginning of their careers has probably adversely affected Millennials’ career earnings paths,” the report says.

Median net worth for those aged 20-35 in 2010 was $11,235. And that number stayed pretty stagnant for the following six years, inching up to just $12,100, according to the report.

“People who come into the labor market in bad years tend to show the effects of that over time,” says Brookings Institution economist William Gale, a co-author of the report.

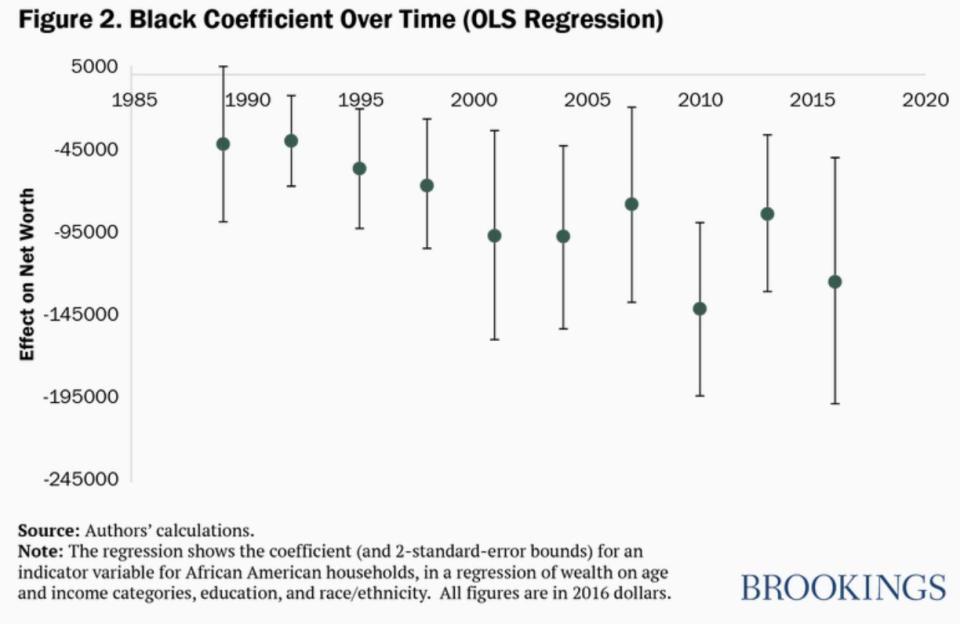

Racial factors

After taking a snapshot of millennials’ current financial picture, the report also looked into their future earning prospects and how much wealth they’ll be able to accumulate by the time they retire.

The racial composition of the millennial generation turns out to be a major factor here. As much as 44% of the millennial generation identifies as a minority, compared to 25% of baby boomers who identified as such in the mid-80’s. The fact that minorities accumulate less wealth is an important issue highlighted by the report given that minorities are a greater share of the millennial population today.

By analyzing surveys of consumer finances from 1989 to 2016, the report found that minority status is negatively associated with net worth and that the gap between the wealth of black households relative to whites is increasing.

“I thought that the result was going to be that the difference had shrunk over time, but it turned out it really hasn’t since 1989,” Gale says. “If anything, for black households the difference has gotten bigger. To what extent is it discrimination, to what extent is it something else? It’s an enormously complicated set of circumstances, and I don’t want to pretend we have any new insights on the why.”

Outliving assets

The Peterson report notes that the shift from pensions to retirement savings accounts – from a system in which employers contributed to workers’ retirements to one in which the individual has the responsibility – is also weighing on younger generations.

“That puts more burden on them, planning how much to save, how to allocate it, when to take the money out, how much money to take out,” Gale says. “There’s much more responsibility placed on an individual in a defined-contribution plan like a 401(k) than there would be if there’s just a defined-benefit plan.”

The fact that millennials are delaying major life milestones such as buying a house, getting married, and starting a family could spell trouble for their retirement plans.

“Delays in all those life cycle events would cause them to delay the onset of retirement saving,” says Gale. The millennial generation will almost certainly live longer than their predecessors.

“From the perspective of trying to save enough for retirement, living longer makes it harder. So they have an increased risk of outliving their assets,” he says.

Follow Sibile Marcellus on @SibileTV

More from Sibile:

More households subscribe to a streaming service than pay TV now: Deloitte

Trump isn’t worries about rising government debt, and neither are voters

Workers threatened by automation shift their skills to become drivers, electricians: LinkedIn

Two-thirds of US millennial women say they’re in ‘poor or fair’ shape