MasterCraft’s (NASDAQ:MCFT) Q2 Sales Top Estimates But Stock Drops 12.4%

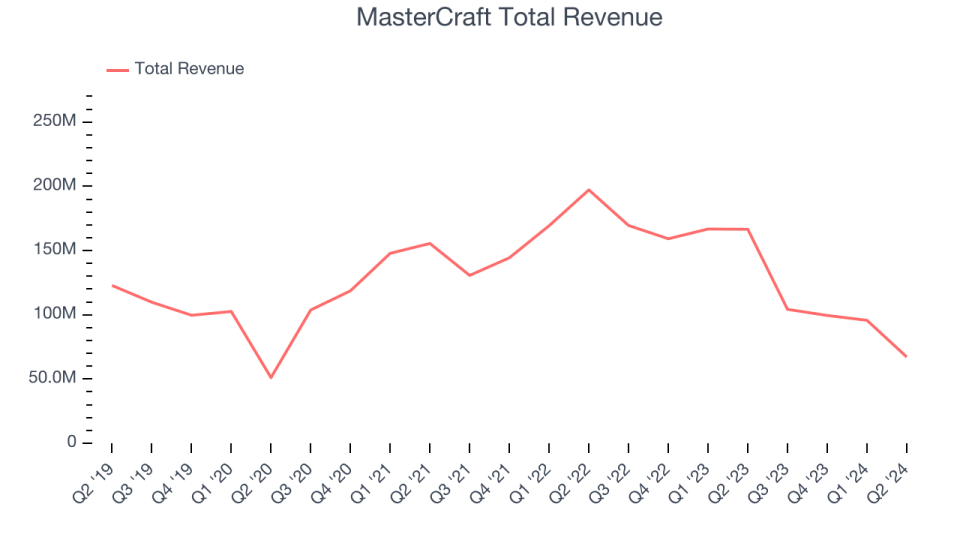

Sport boat manufacturer MasterCraft (NASDAQ:MCFT) beat analysts’ expectations in Q2 CY2024, with revenue down 59.7% year on year to $67.18 million. On the other hand, next quarter’s revenue guidance of $61 million was less impressive, coming in 22.8% below analysts’ estimates. It made a non-GAAP loss of $0.04 per share, down from its profit of $1.30 per share in the same quarter last year.

Is now the time to buy MasterCraft? Find out in our full research report.

MasterCraft (MCFT) Q2 CY2024 Highlights:

Revenue: $67.18 million vs analyst estimates of $63.09 million (6.5% beat)

EPS (non-GAAP): -$0.04 vs analyst estimates of -$0.22 ($0.18 beat)

Management’s revenue guidance for the upcoming financial year 2025 is $282.5 million at the midpoint, missing analyst estimates by 28.4% and implying -22.9% growth (vs -44.6% in FY2024)

EPS (non-GAAP) guidance for the upcoming financial year 2025 is $0.62 at the midpoint, missing analyst estimates by 61.4%

EBITDA guidance for the upcoming financial year 2025 is $20.5 million at the midpoint, below analyst estimates of $44.76 million

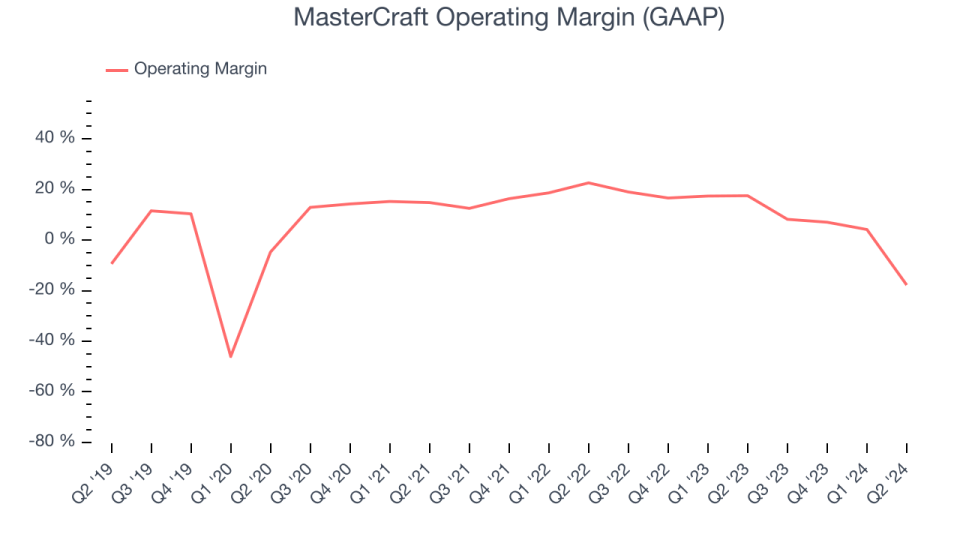

Gross Margin (GAAP): 12.2%, down from 25.8% in the same quarter last year

EBITDA Margin: 1.3%, down from 19.6% in the same quarter last year

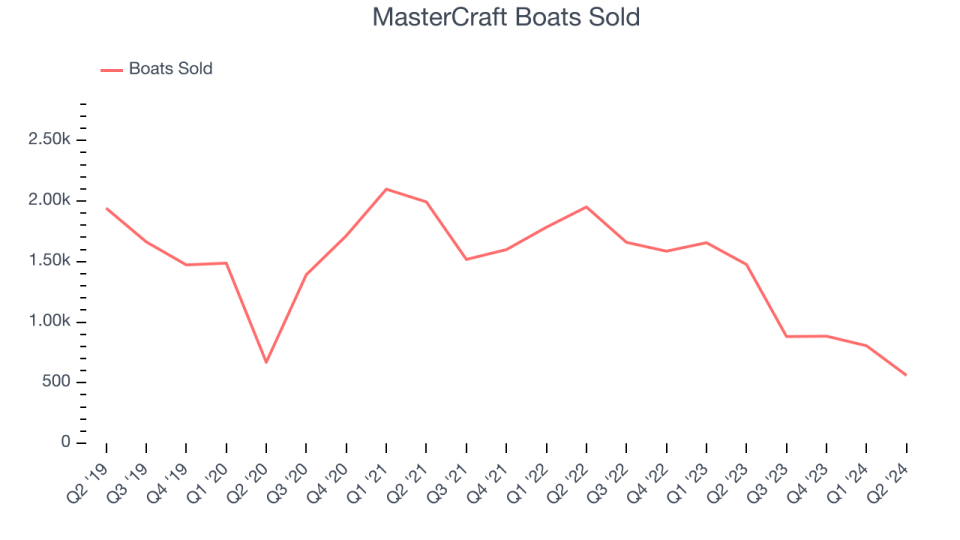

Boats Sold: 560, down 916 year on year

Market Capitalization: $337.2 million

Brad Nelson, Chief Executive Officer, commented, “MasterCraft delivered results ahead of our latest expectations as we navigated a challenging economic environment and a highly competitive retail landscape during the fourth quarter and fiscal year. We executed well against our strategic and operational priorities during the year as we destocked field inventory levels, advanced consumer-centric initiatives, and returned capital to shareholders, all while optimizing profitability and cash flow.”

Started by a waterskiing instructor, MasterCraft (NASDAQ:MCFT) specializes in designing, manufacturing, and selling sport boats.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. MasterCraft’s demand was weak over the last five years as its sales fell by 4.7% annually, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. MasterCraft’s recent history shows its demand has stayed suppressed as its revenue has declined by 24.4% annually over the last two years.

We can dig further into the company’s revenue dynamics by analyzing its number of boats sold, which reached 560 in the latest quarter. Over the last two years, MasterCraft’s boats sold averaged 28.5% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, MasterCraft’s revenue fell 59.7% year on year to $67.18 million but beat Wall Street’s estimates by 6.5%. The company is guiding for a 41.5% year-on-year revenue decline next quarter to $61 million, a deceleration from the 38.5% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 5.3% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

MasterCraft’s operating margin has been trending down over the last year, but it still averaged 12.1%, decent for a consumer discretionary business. This shows it generally does a decent job managing its expenses.

In Q2, MasterCraft generated an operating profit margin of negative 17.8%, down 35.3 percentage points year on year. This contraction shows it was recently less efficient because its expenses increased relative to its revenue.

Key Takeaways from MasterCraft’s Q2 Results

It was good to see MasterCraft beat analysts’ revenue and EPS expectations this quarter. On the other hand, its full-year revenue and earnings guidance missed Wall Street’s estimates. Overall, this was a mediocre quarter, and the weak outlook is weighing on shares. The stock traded down 12.4% to $17.40 immediately following the results.

MasterCraft may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.