Should Investors View SM's Cheap Valuation as a Buying Opportunity?

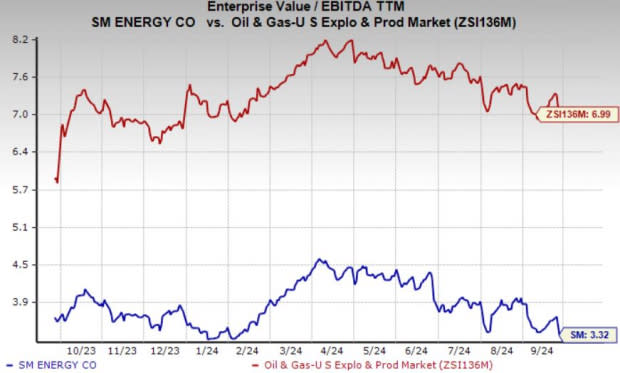

SM Energy SM is currently considered undervalued, trading at a 3.32x trailing 12-month enterprise value to earnings before interest, taxes, depreciation and amortization (EV/EBITDA), which is below the broader industry average of 6.99x. It is also cheaper than larger exploration and production players such as EOG Resources Inc EOG and ConocoPhillips COP, which have respective EV/EBITDA of 5.11X and 5.09X.

Image Source: Zacks Investment Research

While a discounted valuation can offer a potentially profitable opportunity for investors, it's crucial to assess whether the upstream company is dealing with any internal challenges. A deeper analysis is necessary to determine if SM’s lower valuation is warranted based on its fundamentals, growth outlook and current market conditions.

SM’s Established Position in the Oil-Rich Midland Basin

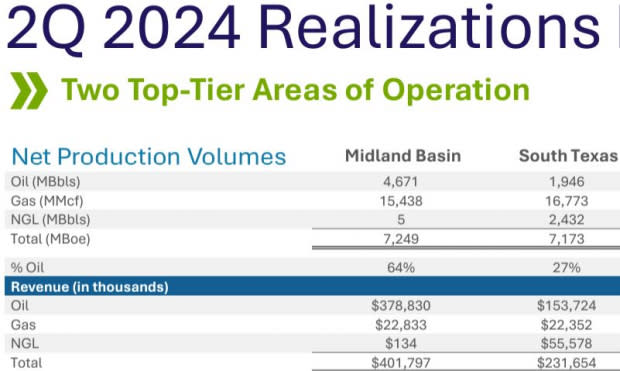

SM Energy generates most of its revenues from operations in the Midland Basin. In the second quarter, more than 60% of the company’s revenues came from its activities in this region, with production totaling 7,249 thousand barrels of oil equivalent, 64% of which was oil. With oil prices expected to remain strong, the business outlook for this upstream firm appears promising.

Image Source: SM Energy

In 2024, SM Energy plans to drill a net of 72 wells and complete a net of 71 wells in the Midland Basin, highlighting the company's strong commitment to this region. Its operations in the Midland Basin span across 111,000 net acres, reflecting its focus on maximizing production and growth in this area.

Uinta Basin Acquisition Agreement to Propel SM’s Growth

On June 27, SM Energy inked an accord to acquire 80% of Uinta Basin oil and gas assets owned by certain entities affiliated with XCL Resources for a net purchase price of $2.04 billion. Once the acquisition closes, it will add approximately 37,200 net acres to the company’s top-tier portfolio. This will not only increase oil production significantly but also add roughly 390 net drilling locations.

Many analysts believe that while the Uinta Basin is smaller, it might have the potential to outperform the Permian Basin due to its higher oil content and lower operating costs. This makes the Uinta Basin an attractive area for future development.

Once completed, likely by Oct. 1, the acquisition is expected to immediately enhance SM Energy's financials. This move will allow the company to maximize its return on capital while preserving its strong balance sheet. Supported by these positive developments, the board of directors has authorized an 11% increase in the fixed quarterly dividend, which is anticipated to begin in the fourth quarter.

Further, SM Energy’s board of directors has authorized a new $500 million share repurchase program, which will run through 2027 and replace the remaining portion of the existing program.

Should Investors Take a Chance on Undervalued SM Stock?

Despite these positive developments, the exploration and production company's price chart has not fully reflected them, as the stock is trading at a discount to its true value. Thus, it appears that SM Energy has the potential to outperform the industry once the stock market begins to acknowledge its true value.

However, there are near-term concerns related to SM’s rising debt levels. The company has raised $1.5 billion in new debt through senior note issuance to finance its acquisition in the Uinta Basin, which adds to its overall debt burden. As such, while the acquisition, which is still pending, is expected to improve production and inventory, it will be crucial for SM to prioritize debt reduction to alleviate financial strain moving forward.

Given the current debt risks and market uncertainty, it is prudent to hold SM stock rather than buy at this time. This strategy allows for greater clarity on the Zacks Rank #3 (Hold) company's financial health and debt management. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

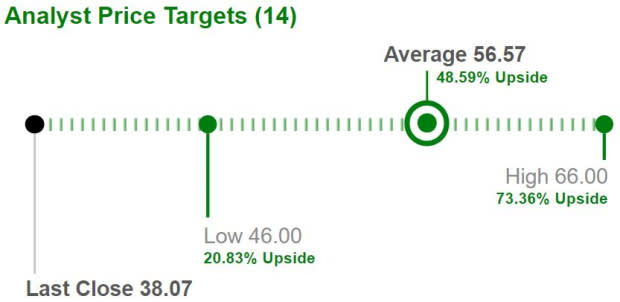

Major brokers have increased SM’s short-term price target by almost 49% from its recent closing price of $38.07, with the highest target set at $66, indicating a potential upside of 73.4%. Consequently, current investors stand to benefit from this upward price trend in the interim.

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ConocoPhillips (COP) : Free Stock Analysis Report

EOG Resources, Inc. (EOG) : Free Stock Analysis Report

SM Energy Company (SM) : Free Stock Analysis Report