One of the more popular measures of stock market value, the forward price/earnings (P/E) multiple, is so high that one closely-followed economist warned that buying stocks now would be like “picking up nickels in front of a steam roller.”

Indeed, while stock prices (P) have surged, analysts’ published forecasts for earnings (E) have gone sideways.

But that is far from the whole story.

One narrative that’s been flying under the radar is how Donald Trump’s election is impacting the analysts’ forecasts for earnings. Keep in mind, the “E” in forward P/Es are 12-month forecasts for earnings. While most strategists agree that Trump’s proposals — should they be enacted — would be a big net positive for earnings, few have actually tweaked their earnings outlooks.

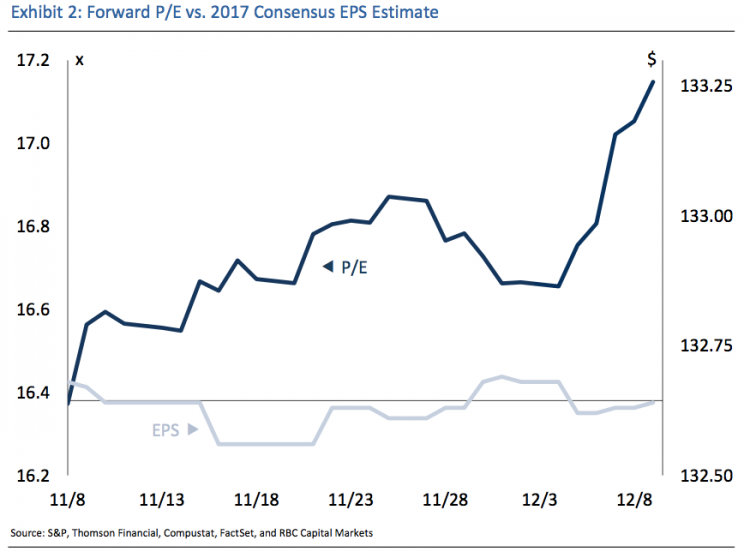

“The ‘P’ is up but the ‘E’ is effectively stale,” RBC Jonathan Golub said to Yahoo Finance. “[We have] a market that has a P/E lower than the stated number and an E that’s lower than the stated number.”

In other words, this forward P/E measure that has people freaked out is actually a bit of a mirage.

A similar phenomenon is occurring among economic forecasters who are calling for lackluster US GDP growth.

“The consensus essentially sees growth running in place at 2.2%, which is about how the US economy has fared since the end of the recession,” Renaissance Macro’s Neil Dutta said. “This is particularly conservative considering that data has generally been surprising on the upside over the last six months with GDP typically tracking above 2.5%. That is higher than the highest primary dealer estimate on Wall Street for 2017 – 2.4%. Nowcasts of economic activity suggest growth remains strong into the New Year. Thus, we see more room for upward revisions to the consensus.”

So, what gives?

“Analysts tend to be cautious in adjusting estimates following breaking news, acting only after ascertaining company-specific impacts,” Golub said. “Investors, by contrast, are quicker to respond to incomplete information.”

In other words, Golub is saying that investors are already pricing in the expectations for better earnings growth, which is driving up the “P.” Meanwhile, most analysts have yet to pull the trigger on their post-Election updated forecasts for earnings.

“This timing difference creates the false impression that valuations are stretched, and should correct as analysts catch up to the market,” Golub said.

So then, what’s taking so long?

Belski attributes this issues within the business of forecasting where, as he says, “analysts are almost always wrong.”

“We are so afraid of being wrong that we don’t wanna be right,” Belski said, speaking to the issue of career risk. This message is echoed in a recent Wall Street Journal story aptly titled, “Wall Street Strategists Feel Better Together in 2017.”

As Yahoo Finance’s Myles Udland reported on Wednesday, markets will be antsy as they await clarity on policy. Even the Federal Reserve is on watch for what may come of fiscal policy. And it certainly is no help that Wall Street’s forecasters are similarly awaiting clarity before they decide to offer more precise guidance.

Fortunately for some folks, there are a minority of Wall Street analysts willing to go out on a limb.

The conditional forecast

“[T]here is no reason not to expect President-elect Trump to accomplish many of his primary legislative goals such as pro-growth tax reform, which we believe is at the top of the new Administration’s list of policy priorities,” Deutsche Bank Chief US Economist Joe LaVorgna asserted on Wednesday.

“Unlike Presidents Reagan and Bush, neither of whom had control of both branches of Congress, President-elect Trump’s party has majorities in both the House and the Senate,” he continued. “Hence, it substantially raises the probability that the new president will be able achieve much of his tax goals.”

David Bianco, LaVorgna’s colleague and Deutsche Bank’s Chief US Equity Strategist, has told clients the bank’s clients that his official forecast is for the S&P 500 to rally to 2,350 by the end of 2017 on earnings of $130 per share. However, he also offered an alternative forecast of 2,400 on $140 EPS should the incoming administration get the statutory corporate tax rate cut to 25% from 35%.

Folks bidding up prices on the expectation for tax cuts will probably find some utility in Bianco’s scenario-based forecasts.

To their credit, Belski and Golub have their money where their mouths are. For 2017, Belski expects the S&P 500 to rally to 2,350 on EPS of $134, which is the highest official EPS forecast of strategists followed by Yahoo Finance. Meanwhile, Golub is the most bullish strategist we follow with an S&P target of 2,500 target on EPS of $128.

Both Belski and Golub expect 2017 to be a year where earnings estimates are gradually revised up.

This post includes large excerpts from a post published on January 3, 2017.

–

Sam Ro is managing editor at Yahoo Finance.

Read more: