Here's Why Investors Should Add PRA Group Stock to Their Portfolio

PRA Group, Inc. PRAA is well-poised to grow due to higher recent portfolio purchases and improved pricing in the United States, coupled with better overall cash collections. The company's adeptness in managing diverse debt types positions it strategically for effective portfolio diversification.

PRA Group is a global financial and business services company in the Americas, Australia and Europe, with a market cap of $797.4 million. The company specializes in the acquisition, collection and management of non-performing loans, constituting its core business activities.

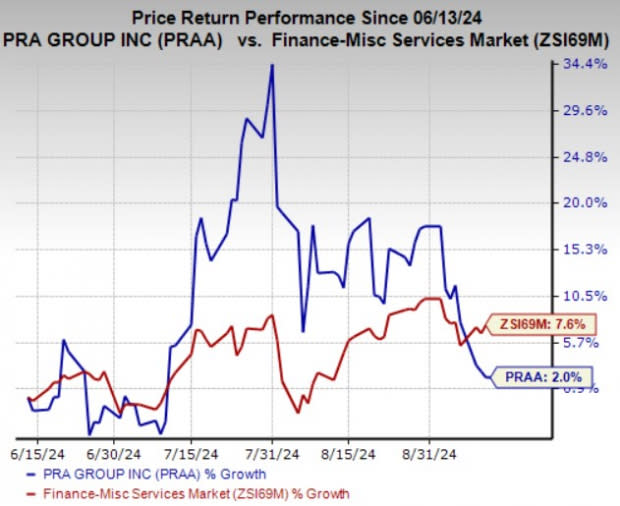

In the past three months, PRA Group’s shares have gained 2% compared with the industry’s 7.6% growth. However, higher purchase volumes at favorable pricing should push the stock upward in the future.

Image Source: Zacks Investment Research

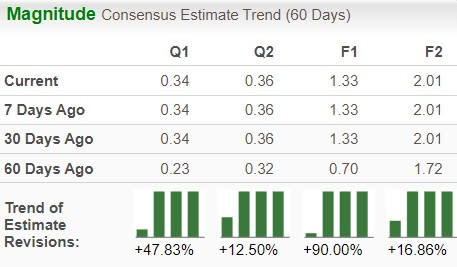

PRAA Estimate Revisions Trend

The Zacks Consensus Estimate for PRA Group’s 2024 bottom line indicates an improvement of more than one-fold. Its 2024 EPS estimate has been revised upward over the past 60 days, reflecting positive analyst sentiment. The company beat earnings estimates in each of the last four quarters.

Image Source: Zacks Investment Research

The consensus estimate for 2024 revenues is pegged at $1.1 billion, indicating a 33.8% rise year over year. The company’s performance is expected to improve in 2024 as it intends to make more profitable purchases, which will constitute a larger part of its portfolio.

PRAA’s Growth Prospects

PRA Group is expected to leverage improving portfolio supply and pricing in the United States amid ongoing credit normalization. This positive purchasing environment is a key factor contributing to the company's anticipated growth in the bottom line.

Moreover, rising industry credit card balances and higher charge-off and delinquency rates should fuel supply in the United States. Continued cash collection growth in its Europe business also bodes well. It expects cash collections to continue on its double-digit growth trajectory for the remainder of 2024.

In the second quarter, PRA Group made notable strides in its non-performing loan portfolio acquisitions, totaling $379.4 million. The company purchased portfolios worth $1.2 billion in 2023, up 36% year over year. Its focus on investments in boosting digital capabilities and technologies can play a major role in future performance.

With modernizing collections, the cash efficiency ratio is likely to grow. The company expects the cash efficiency ratio to be around 60% in 2024, up from 58% in 2023. Notably, its forward 12-month price-to-earnings ratio of 11.21X is lower than the industry average of 13.66X, indicating that the stock is more affordable. Courtesy of solid prospects, this Zacks Rank #1 (Strong Buy) stock is worth adding to your portfolio at the moment.

However, there are a few factors that can hold the stock back. Its total debt to total capital of 72.9% is much higher than the industry’s figure of 56.3%. Increased leverage is leading to higher interest expenses. Also, increasing legal collection costs and agency fees are denting margins. The metrics jumped 36.3% and 16.2% year over year, respectively, in the first half of 2024. However, we believe that a systematic and strategic plan of action will drive its long-term growth.

Other Stocks to Consider

Investors interested in the broader Finance space may look at some other top-ranked players like Aflac Incorporated AFL, Brown & Brown, Inc. BRO and Arthur J. Gallagher & Co. AJG. Each stock presently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Aflac’s current-year earnings is pegged at $6.73 per share, which indicates 8% year-over-year growth. It witnessed seven upward estimate revisions in the past 30 days against no downward movement. AFL beat earnings estimates in three of the past four quarters and missed once, with an average surprise of 8.2%.

The Zacks Consensus Estimate for Brown & Brown’s 2024 earnings indicates 31% year-over-year growth. During the past two months, BRO has witnessed six upward estimate revisions against none in the opposite direction. It beat earnings estimates in each of the past four quarters, with an average surprise of 9.8%.

The Zacks Consensus Estimate for Arthur J. Gallagher’s current-year earnings suggests a 16% year-over-year jump. During the past two months, AJG has witnessed six upward estimate revisions against none in the opposite direction. The consensus mark for current-year revenues indicates 14.5% growth from a year ago.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aflac Incorporated (AFL) : Free Stock Analysis Report

PRA Group, Inc. (PRAA) : Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG) : Free Stock Analysis Report

Brown & Brown, Inc. (BRO) : Free Stock Analysis Report