Global Payments Stock Drops 6.5% as 2025 Outlook Spooks Investors

Shares of Global Payments Inc. GPN dropped 6.5% yesterday following its downbeat outlook. The company is planning to streamline its operations further to build a more unified operating business. GPN intends to concentrate its investments while maximizing the potential of the company’s portfolios. It expects 2025 to be a transition year for the company.

Now, let’s take a closer look at its outlook and strategic targets.

GPN’s Outlook vs. Consensus Estimates

Global Payments is aiming for adjusted net revenue growth, excluding dispositions, in the mid-single-digit percentage range for 2025. This is slightly below the Zacks Consensus Estimate, which was expecting around 7% growth year over year. The company expects elevated revenue growth of mid-to-high single digits for the 2026-2027 period.

In terms of profitability, it expects adjusted earnings per share growth of around 10% for 2025. In contrast, the consensus estimate predicts a 13.1% year-over-year increase for the same year. It anticipates the bottom line to grow by low teens percentage in the 2026-2027 period.

For 2025, GPN expects the adjusted operating margin to expand more than 50 basis points (bps). Adjusted operating margin for the 2026-2027 period is expected to increase 50-100 bps.

GPN’s Divestures

The company doesn’t shy away from getting rid of non-core operations. GPN sold Netspend business back to its founders for $1 billion last year to move away from the consumer side of the business and focus on business-to-business or B2B clients. Looking ahead, Global Payments has identified potential divestitures, which account for annual adjusted net revenues of $500-$600 million. Also, some limited tuck-in merger and acquisition activities are expected from the company.

GPN foresees its transformation and streamlining efforts to deliver more than $500 million of run-rate operating income benefits by the first half of 2027. While 30% of the benefits are expected to be achieved next year, the rest will likely come in the 2026-2027 period. However, the company expects the one-time costs to be two-thirds of the benefits.

GPN’s Other Targets

The company is likely to keep capital expenditure in the 7-8% range of its adjusted net revenues.

Investors are noticing its shareholder value boosting efforts. GPN is aiming at more than $2 billion of share buybacks per annum. It plans to return more than $7.5 billion of capital in the next three years. GPN bought back shares worth $900 million in the first half of 2024.

Global Payments’ cash-generating ability will support its shareholder-friendly moves. This Zacks Rank #3 (Hold) company expects to generate $8.5-$9 billion in cumulative free cash flow in the next three years. It generated $2.5 billion in adjusted free cash flow last year.

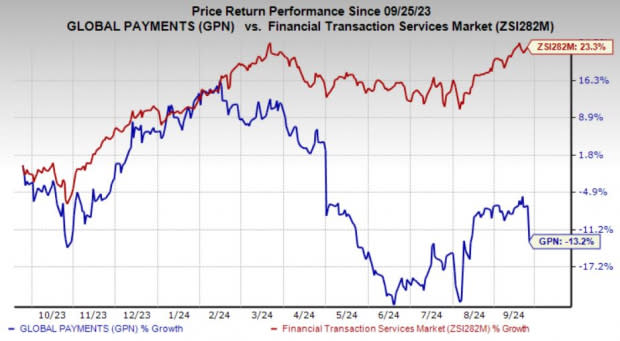

GPN’s Price Performance

Investors will continue to keep a close eye on how successfully the company manages its costs and margins during this transition period. In the past year, Global Payments’ shares have lost 13.2% against the industry’s 23.3% growth.

Image Source: Zacks Investment Research

Better-Ranked Picks

Investors can look at some better-ranked stocks from the broader Business Services space, like Fidelity National Information Services, Inc. FIS, Paysign, Inc. PAYS and Remitly Global, Inc. RELY. While Fidelity National currently sports a Zacks Rank #1 (Strong Buy), Paysign and Remitly Global each carry a Zacks Rank # 2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Fidelity National’s current-year earnings indicates a 50.7% year-over-year increase. FIS beat earnings estimates in two of the trailing four quarters and missed twice. The consensus estimate for current-year revenues is pegged at $10.2 billion.

The consensus estimate for Paysign’s current-year earnings indicates 75% year-over-year growth. The consensus estimate for PAYS’ current-year revenues is pegged at $58 million, implying 22.6% year-over-year growth.

The Zacks Consensus Estimate for Remitly Global’s current-year earnings indicates a 53.9% year-over-year improvement. RELY beat earnings estimates in two of the trailing four quarters and missed twice, with the average surprise being 8%. The consensus estimate for current-year revenues implies 31.8% year-over-year growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fidelity National Information Services, Inc. (FIS) : Free Stock Analysis Report

Global Payments Inc. (GPN) : Free Stock Analysis Report

Remitly Global, Inc. (RELY) : Free Stock Analysis Report

Paysign, Inc. (PAYS) : Free Stock Analysis Report