Flowers Foods Stock at a 0.96X P/S Multiple: Is Now the Time to Buy?

Flowers Foods, Inc. FLO is currently trading at an attractive valuation, considering its price-to-sales (P/S) multiple, which is significantly lower than both the Zacks Food – Miscellaneous industry and the broader Consumer Staples sector. FLO’s forward 12-month P/S ratio is 0.96, lower than the industry average of 1.48 and the sector average of 8.53.

Image Source: Zacks Investment Research

This discrepancy in valuation suggests that the stock may be undervalued relative to its peers, presenting a compelling opportunity for investors seeking value in the consumer staples space. With a Value Score of B, Flowers Foods strengthens its investment appeal, reflecting a favorable risk-reward profile.

Technical indicators are supportive of Flowers Foods’ performance. The stock is trading above both its 50-day and 200-day moving averages, indicating robust upward momentum and price stability. This technical strength reflects positive market perception and confidence in the company’s financial health and prospects.

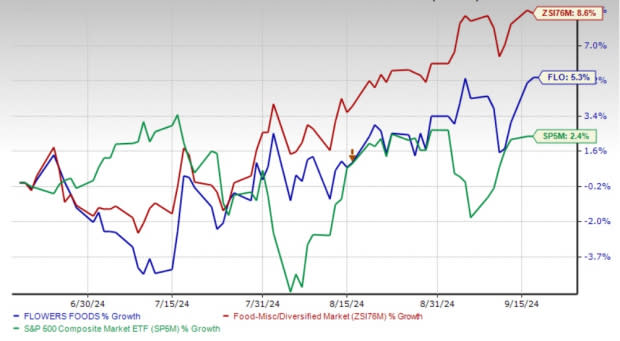

While its recent price performance slightly trails industry peers, FLO has managed to outperform the broader market, reflecting its steady performance amid macroeconomic uncertainty. Shares of FLO have risen 5.3% in the past three months compared with the industry’s 8.6% growth and the S&P 500’s gain of 2.4%. Investors may find this combination of value, technical strength and relative market outperformance a good reason to consider Flowers Foods as a long-term investment opportunity.

Image Source: Zacks Investment Research

FLO on Track With Strategic Priorities

The company has been on track with its core priorities, which include developing its team, concentrating on brands, prioritizing margins and looking out for prudent mergers and acquisitions. To this end, management has been shifting its focus toward becoming a more brand-focused company. Flowers Foods expects its optimized portfolio to drive market share gains through innovation.

Flowers Foods has been benefiting from its portfolio strategy, aimed at transitioning a larger part of its sales to higher-margin branded retail products, alongside enhancing the profitability of the private label and away-from-home business. The company has been solidifying its brands via innovation and marketing investments. In the second quarter of 2024, branded retail increased 0.3% year over year and formed 64.4% of sales, driven by the favorable shift toward more premium-priced products. By emphasizing branded products with higher margins, FLO aims to drive top-line growth and expand gross margins, contributing to overall profitability.

Moving to margins, the company is undertaking pricing and saving measures and efforts to enhance business efficiency. Flowers Foods has been boosting its cost structure and increased its expected annual savings from $30-40 million to $40-50 million in the second-quarter 2024 earnings release. This was achieved through targeted initiatives, including workforce reductions, reduced third-party spending and optimization of the Direct-Store-Delivery network.

Innovation & Acquisitions Drive Flowers Foods’ Growth

Innovation remains at the core of Flowers Foods' strategy, with several new product launches contributing to growth. The introduction of DKB Amped-Up Protein Bars and the expansion of DKB Snack Bites highlight the company’s ability to extend its brand into adjacent categories like snacking, which offers substantial growth potential. By leveraging Dave’s Killer Bread’s brand equity, Flowers Foods is driving incremental revenues and diversifying its product portfolio, setting the stage for sustained growth in 2025 and beyond.

Acquisitions play a crucial role in Flowers Foods' growth strategy, allowing the company to expand its brand lineup, geographic coverage and product offerings. By seeking potential acquisitions and investments that align with its strategic priorities, Flowers Foods aims to strengthen its position in core categories and pursue opportunities in emerging markets. The company’s most recent acquisition of Papa Pita Bakery (concluded in February 2023) has been contributing to its results.

What to Expect From FLO in 2024?

For fiscal 2024, Flowers Foods expects sales in the range of $5.091-5.172 billion, suggesting flat to a 1.6% increase year over year. Adjusted EBITDA is likely to be in the range of $524-$553 million compared with $501.7 million recorded in fiscal 2023. For fiscal 2024, the adjusted EPS is envisioned in the range of $1.20-$1.30 compared with $1.20 delivered in fiscal 2023.

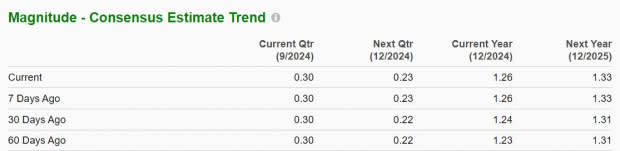

Reflecting the positive sentiment around Flowers Foods, the Zacks Consensus Estimate for earnings per share has seen upward revisions. Over the past 30 days, analysts have increased their estimates for the current and next fiscal year by 2 cents each to $1.26 and $1.33 per share, respectively. These estimates indicate expected year-over-year growth rates of 5% and 5.4%, respectively.

Image Source: Zacks Investment Research

Investors’ Playbook for FLO Stock

Flowers Foods presents a compelling investment opportunity, driven by its attractive valuation, solid technical performance, and strategic focus on innovation and brand expansion. With sales and earnings forecasts indicating a steady improvement in fiscal 2024, coupled with upward revisions in earnings estimates, Flowers Foods is well-positioned for continued success. As the company continues to execute its strategic priorities, FLO remains an excellent choice for those looking to capitalize on growth within the food industry. The company currently carries a Zacks Rank #2 (Buy).

Other Solid Food Stocks

The Chef’s Warehouse CHEF, which engages in the distribution of specialty food products, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

CHEF has a trailing four-quarter earnings surprise of 33.7%, on average. The Zacks Consensus Estimate for The Chef’s Warehouse’s current fiscal year sales and earnings indicates growth of 9.7% and 12.6%, respectively, from the year-ago reported numbers.

McCormick MKC is a leading manufacturer, marketer and distributor of spices, seasonings, specialty foods and flavors. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for McCormick & Company’s current fiscal-year sales and earnings indicates advancements of 0.1% and 5.6%, respectively, from the year-ago reported figures. MKC has a trailing four-quarter earnings surprise of 8.3%, on average.

Ingredion Incorporated INGR, which manufactures and sells sweeteners, starches, nutrition ingredients and biomaterial solutions, currently carries a Zacks Rank #2. INGR has a trailing four-quarter earnings surprise of nearly 11%, on average.

The Zacks Consensus Estimate for Ingredion Incorporated’s current financial-year earnings implies growth of 5.6% from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

Ingredion Incorporated (INGR) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report