Flex Stock Up 14% in the Past Six Months: Will the Rally Last?

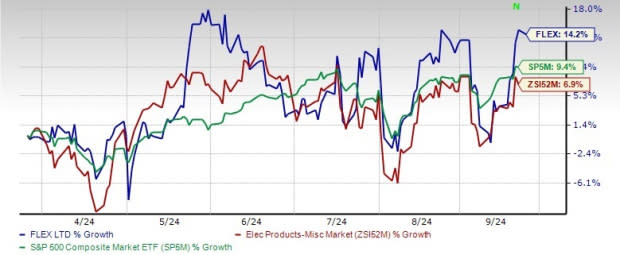

Flex Ltd FLEX has witnessed strong momentum in the past year, with its shares rising 14.2% compared with the S&P 500 composite and the subindustry’s growth of 9.4% and 6.9%, respectively.

The company’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters with an average surprise of 15%. The stock is still down 4% from its 52-week high level of $34.12 on May 30, 2024.

Flex has evolved into an end-to-end solutions provider where it is engaged in design, procurement, manufacturing and supply services for a broad range of products. In addition, the company offers value-added services in design, metal, components, supply chain management integration and aftermarket services, like circular economy. These additional capabilities and a diversified end-market are key positives for the company’s business model.

Six-month Price Performance

Image Source: Zacks Investment Research

Strengthening Demand Trends Bode Well for FLEX

FLEX’s performance is buoyed by healthy demand trends across cloud /AI, automotive and digital healthcare. The rapid AI proliferation in the data center vertical is driving increasing demand for cloud solutions.

New deal wins and accelerating content growth amid soft EV trends are powering the automotive unit. Also, the company’s digital healthcare segment is witnessing strong medical device demand, whereas the medical equipment market remains weak.

Synergies from the acquisition of FreeFlow augur well. FreeFlow offers services in global secondary markets, specializing in asset disposition, digital circular economy tracking and reporting capabilities. The initiative is likely to augment FLEX’s service footprint across emerging markets, such as data center, enterprise and lifestyle, unlocking new sources of revenues and fostering sustainability through second-life products.

The company is advancing cloud, power and automotive businesses by launching strategic programs, which is reflected in the top-line performance in the last reported quarter. The initiatives are likely to positively impact Flex’s performance in the fiscal second quarter as well as the latter half of the fiscal year. Its innovative suite of power products and services enhances customer satisfaction. All these factors favorably position Flex for the AI-powered technology shift, prevalent in the industry, from grid to chip and from the cloud to the edge.

FLEX’s Attractive Valuation

FLEX presents a compelling investment opportunity with its attractive forward 12-month price-to-earnings ratio of 12.65X, significantly lower than the industry average of 23.54X observed in the past year. Its forward 12-month price-to-earnings ratio positions FLEX as a value-driven choice with significant upside potential.

Image Source: Zacks Investment Research

FLEX Faces Headwinds

Flex expects macro headwinds to persist throughout 2024, adversely impacting various end markets. An increase in global tax rates is also concerning. Amid strength in data center power, a slowdown in the industrial sector, notably the renewable space, continues to pose headwinds. Slackening trends (except cloud) in enterprise IT and telco spending coupled with cautious consumer spending pose headwinds.

Affected by weak macro trends in core industrial, management expects revenues in Reliability Solutions to be down from high single-digit to mid-teens in the fiscal second quarter. A slowdown in enterprise IT spending will keep Agility Solutions revenues flat to slightly down.

For second-quarter fiscal 2025, Flex expects revenues to be between $6.2 billion and $6.8 billion, while adjusted earnings in the range of 52-60 cents per share.

Stiff competition and leveraged balance sheet remain concerns. As of June 30, 2024, the company’s cash & cash equivalents were $2.24 billion, while long-term debt (net of the current portion) was $2.6 billion.

A Look at Estimate Revision Activity for FLEX

FLEX’s earnings per share are expected to be $2.40 and $2.79 in fiscal 2025 and 2026, respectively, increasing 11.6% and 16.4% on a year-over-year basis.

The Zacks Consensus Estimate for fiscal 2025 and 2026 earnings per share has declined 2 cents and 1 cent, respectively, in the past 30 days.

For fiscal 2025, revenues are anticipated to decline 8.2% to $25.8 billion, while revenues for fiscal 2026 are expected to increase 4.2% to $26.9 billion.

FLEX’s Zacks Rank

Flex carries a Zacks Rank #3 (Hold) at present. Though healthy demand trends across cloud /AI, automotive and digital healthcare bode well, weakness in core industrial remains concerning amid rising global tax rates and a dynamic macro backdrop. Consequently, it might not be a prudent investment decision to bet on the stock right now. However, stakeholders and investors already owning the stock could stay put as long-term prospects for FLEX appear promising.

Stocks to Consider

Some better-ranked stocks worth consideration in the broader technology space are Seagate Technology Holdings plc STX, American Software, Inc. AMSWA and ANSYS ANSS. While Seagate sports a Zacks Rank #1 (Strong Buy), AMSWA and ANSYS carry a Zacks Rank #2 (Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for STX’s fiscal 2025 EPS is pegged at $7.41, unchanged in the past 30 days. STX’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters while missing in the remaining quarter with the average surprise being 80.9%. The stock has surged 64.3% in the past year.

The Zacks Consensus Estimate for American Software’s 2024 EPS is pegged at 38 cents, unchanged in the past seven days. AMSWA’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters while matching in the remaining quarter, with the average surprise being 84.53%. Its shares have declined 5.1% in the past year.

The Zacks Consensus Estimate for ANSS’ 2024 earnings is pegged at $9.96, unchanged in the past 30 days. ANSS’ earnings beat the Zacks Consensus Estimate in three of the last four quarters while missing the mark once, with the average surprise being 4.8%. Its shares have gained 6.5% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Seagate Technology Holdings PLC (STX) : Free Stock Analysis Report

Flex Ltd. (FLEX) : Free Stock Analysis Report

ANSYS, Inc. (ANSS) : Free Stock Analysis Report

American Software, Inc. (AMSWA) : Free Stock Analysis Report