FL Stock Looks Attractive With P/S Multiple of 0.29X: How to Play It?

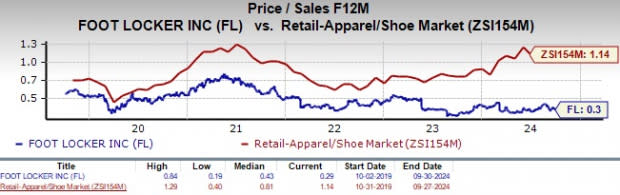

Foot Locker, Inc. FL is currently trading at a notable low price-to-earnings (P/E) multiple, which is below the Zacks Retail-Apparel and Shoes industry and the broader Retail-Wholesale sector’s averages. FL's forward 12-month P/S ratio is 0.29, lower than the industry's and the sector’s ratios of 1.14 and 1.44, respectively.

This stock is undervalued than its industry peers, thereby offering compelling value to investors looking for exposure to the sector. FL's Value Score of A underscores its appeal as an investment option.

Image Source: Zacks Investment Research

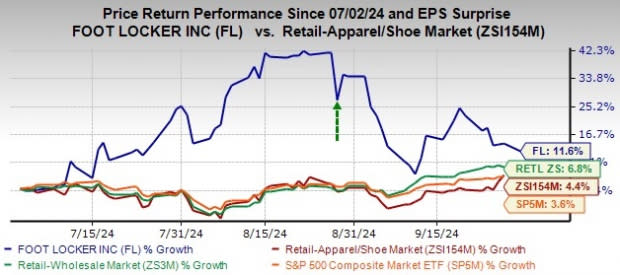

Shares of the company have experienced a decent price increase over the past three months. The stock has gained 11.6% compared with the industry’s 4.4% growth. The company’s ability to adapt to and innovate in challenging market conditions has enabled it to outperform the sector and the S&P 500 index’s rallies of 6.8% and 3.6%, respectively, during the same period.

FL closed yesterday’s trading session at $25.84, which is 27.4% below its 52-week high of $35.60 attained on Feb. 23, 2024. This discount could be seen as a potential entry point, given Foot Locker’s strategic initiatives to adapt to changing consumer behaviors.

Image Source: Zacks Investment Research

FL's Expansion & Customer-Centric Initiatives

Foot Locker is advancing its global footprint with a strong focus on high-growth regions. The company plans to enter the India market by late 2024, partnering with Metro Brands and Nykaa Fashion to capitalize on the rising demand for sneakers and premium footwear.

In another strategic move, Foot Locker has finalized agreements to transition its operations in Greece and Romania to the Fourlis Group, a leading retailer in Southeast Europe. This partnership is set to open more than 100 stores across the region, helping Foot Locker expand its international presence with minimal capital outlay and reduced operational complexities.

The company is also transforming the customer experience through its store redesign initiative. In the second quarter of fiscal 2024, Foot Locker opened five concept stores, revamped or relocated 14 locations, and modernized 67 stores. These upgrades have led to increased conversion rates, larger basket sizes and a boost in women’s footwear sales. The reopening of its flagship 34th Street store in New York, co-designed with Nike and Jordan brands, underscores this innovative approach.

Foot Locker reported a 2.6% increase in comparable sales in the fiscal second quarter, driven by strong performances in its global and Kids Foot Locker brands, which saw a 5.2% year-over-year rise. This growth was especially pronounced during the back-to-school season. The company’s Lace Up Plan further enhanced operations, projecting 2.1% comparable sales growth for fiscal 2024.

The relaunch of the FLX loyalty program in June 2024 boosted customer engagement and sales. Loyalty members accounted for 24% of total sales in the second quarter, a 200-basis-point increase over the previous year. With new features such as cash discounts for point redemptions, the program has driven higher average order values and increased transaction volumes. Foot Locker aims to increase loyalty membership to 50% by 2026, seeing it as a vital component for fostering repeat business and long-term customer loyalty.

Challenges for Key Banners of FL Stock

Despite positive overall sales growth, some key banners are struggling. Champs Sports reported a 3.9% year-over-year decline in comparable sales for the fiscal second quarter, signaling difficulties in repositioning. WSS experienced a 6.2% drop due to inflation and decreased discretionary spending, particularly in California. These setbacks highlight ongoing challenges within Foot Locker’s portfolio.

Although FL managed to expand its gross margin year over year in the second quarter of fiscal 2024, the company lowered its full-year gross margin guidance to 29.5-29.7% from 29.8-30%. This revision is attributed to increased promotional pressure on its international banners and the WSS banner, particularly in apparel.

Wrapping Up

FL offers a compelling investment opportunity due to its undervaluation over industry peers, strong global expansion initiatives and customer-centric innovations like store redesigns and loyalty programs. The company is adapting well to market challenges, showing resilience through partnerships and improved sales performance in key segments.

Despite hurdles in certain banners, FL's focus on growth markets and operational efficiency positions it for long-term success, making it an attractive option for investors seeking value in the retail apparel sector. The company currently carries a Zacks Rank #3 (Hold).

Stocks to Consider

Some better-ranked stocks are Nordstrom Inc. JWN, Abercrombie & Fitch Co. ANF and Steven Madden, Ltd. SHOO.

Nordstrom is a leading fashion specialty retailer in the United States. The company offers an extensive selection of both branded and private-label merchandise. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nordstrom’s fiscal 2024 sales indicates growth of 0.6% from the fiscal 2023 reported figure. JWN has a negative trailing four-quarter average earnings surprise of 17.8%.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It flaunts a Zacks Rank of 1 at present. ANF delivered a 16.8% earnings surprise in the last reported quarter.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and sales indicates growth of 63.4% and 13.1%, respectively, from the fiscal 2024 reported levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Steven Madden designs, sources, markets and sells fashion-forward name-brand and private-label footwear. It currently carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Steven Madden’s 2024 earnings and sales indicates growth of 6.9% and 12.6%, respectively, from the 2023 reported figures. SHOO has a trailing four-quarter average earnings surprise of 9.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Foot Locker, Inc. (FL) : Free Stock Analysis Report

Steven Madden, Ltd. (SHOO) : Free Stock Analysis Report