European Equities: Evergrande, ECB President Lagarde, and U.S Stats in Focus

Economic Calendar

Tuesday, 28th September

GfK German Consumer Climate (Oct)

Wednesday, 29th September

Spanish HICP (YoY) (Sep) Prelim

Thursday, 30th September

French Consumer Spending (MoM) (Aug)

German Unemployment Change (Sep)

German Unemployment Rate (Sep)

Italian CPI (MoM) (Sep) Prelim

Eurozone Unemployment Rate (Aug)

German CPI (MoM) (Sep) Prelim

Friday, 1st October

German Retail Sales (MoM) (Aug)

Spanish Manufacturing PMI (Sep)

Italian Manufacturing PMI (Sep)

French Manufacturing PMI (Sep) Final

German Manufacturing PMI (Sep) Final

Eurozone Manufacturing PMI (Sep) Final

Eurozone CPI (YoY) (Sep) Prelim

The Majors

It was a bearish end to the week for the European majors on Friday, with the majors logging a 2nd loss of the week.

The DAX30 fell by 0.72%, with the CAC40 and the EuroStoxx600 seeing losses of 0.95% and 0.90% respectively.

Disappointing business sentiment figures from Germany pegged the majors back on the day.

Following Thursday’s Evergrande and FED driven relief rally, the mood soured at the end of the week. Uncertainty over Evergrande’s future remained going into the weekend.

The Stats

Germany’s IFO Business Climate Index fell from 99.6 to 98.8, with the Current Assessment sub-index down from 101.4 to 100.4. The Business Expectations sub-index declined from 97.5 to 97.3.

From the U.S

Economic data was limited to housing sector data for August, which had a muted impact on the majors.

The Market Movers

For the DAX: It was a mixed day for the auto sector on Friday. BMW slipped by 0.09% to buck the trend on the day. Daimler rallied by 1.80% to lead the way, however, with Continental and Volkswagen ending the day up by 0.02% and by 0.08% respectively.

It was a bullish day for the banks. Deutsche Bank and Commerzbank saw gains of 1.69% and 1.20% respectively.

From the CAC, it was a bullish day for the banks. BNP Paribas and Credit Agricole rose by 0.80% and by 0.24% respectively, with Soc Gen up by 1.11%.

It was also a bullish day for the French auto sector. Stellantis NV and Renault ended the day up by 0.12% and by 2.37% respectively.

Air France-KLM rallied by 3.09%, while Airbus SE fell by 1.10%.

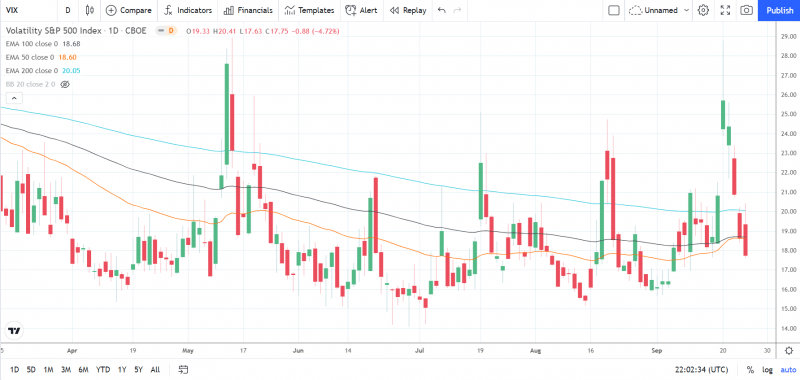

On the VIX Index

It was a 4th consecutive day in the red for the VIX on Friday.

Following a 10.73% slide from Thursday, the VIX fell by 4.72% to end the day at 17.75.

The NASDAQ slipped by 0.03%, while the Dow and S&P500 ended the day up by 0.10% and by 0.15% respectively.

The Day Ahead

It’s a quiet day ahead on the Eurozone’s economic calendar.

There are no material stats due out of the Eurozone to provide the majors with direction. On the monetary policy front, ECB President Lagarde is scheduled to speak. Expect any comments on the economic outlook and monetary policy to provide direction.

Later in the day, durable and core durable goods from the U.S will influence later in the day. A further pickup in core durable goods orders would deliver support.

Away from the economic calendar, Evergrande news will continue to be an area of interest.

The Futures

In the futures markets, at the time of writing, the Dow Mini was up by 144 points.

For a look at all of today’s economic events, check out our economic calendar.

This article was originally posted on FX Empire

More From FXEMPIRE:

The Crypto Daily – Movers and Shakers – September 27th, 2021

Evergrande Crisis: Financial Instability Containable at Risk of Slightly Slower Growth

AUD/USD and NZD/USD Fundamental Weekly Forecast – Investors Eyeing Risk Sentiment for Direction

Ethereum, Litecoin, and Ripple’s XRP – Daily Tech Analysis – September 27th, 2021