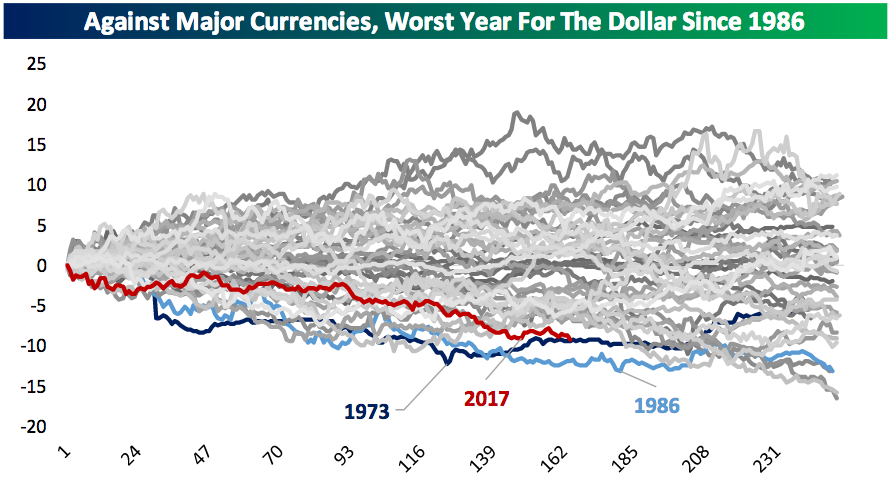

The drop in the U.S. dollar has been one of the defining trades in financial markets this year.

After rallying following the election of Donald Trump in November 2016 and hitting a 13-year high that same month, the dollar has been slammed this year, logging its worst year since 1986 against major currencies as of September 5, according to Bespoke Investment Group.

The most popular explanations for this year’s dollar decline revolve around two key players in Washington, D.C. — Donald Trump and Federal Reserve.

As Yahoo Finance’s Nicole Sinclair outlined last week, Trump’s failure to deliver on his major policy initiatives has in part led to a softening of the dollar. Hopes for fiscal stimulus (and in turn faster economic growth), and fears of more restrictive trade policies, both boosted the dollar’s outlook earlier in the year. Neither have materialized.

Then there is the Federal Reserve, which is no longer alone among major central banks in tightening — or preparing to tighten — monetary policy. The Bank of Canada has raised rates twice, the European Central Bank is jawboning towards the end of its asset purchase program, and the Bank of England has suggested rate hikes could take place later this year.

The transition from dollar to yuan has begun

But in a note to clients out Monday, Carl Weinberg, chief economist at High Frequency Economics, cast doubt on the veracity of arguments that a re-synchronization of global monetary policy is to blame for the dollar’s bad year.

Instead, Weinberg points east to China, citing the growing role of the world’s second largest economy on the global stage, and in particular the oil markets. And the most basic tenant of the global economy Weinberg sees being undermined is the dollar’s primacy as the currency used to facilitate international trade.

Weinberg notes that as of June, Russia accepts yuan — rather than dollars — as payment for oil sales to China. Russia now has 25% of China’s oil import market, up from 15% earlier this year. The significance here is that Russia has been rewarded by China, the world’s largest oil importer, for using its local currency rather than dollars to complete these transactions.

Saudi Arabia, the world’s largest oil exporter, has also been courted by China to break an arrangement under which Aramco, its state-run oil producer, prices oil only in U.S. dollars, Weinberg notes.

“The prospect of the world’s largest importers and exporters of oil pricing and trading crude in yuan is a big dollar-negative,” Weinberg writes.

“If oil trade moves to yuan, it will mean a potential loss of $800 billion per year in U.S. dollar transactions, and a similar reduction of $800 billion in re-cycling of petro-surpluses into U.S. dollar assets. That is not a pretty picture for either the dollar or U.S. securities in the longer term.”

To parse some of this language, most international trade is currently facilitated using U.S. dollars. Which means that it behooves big players in trade — like, for example Aramco — to hold lots of dollar-denominated assets, like Treasury securities. Aramco can then sell Treasuries for cash if it needs the liquidity or can use the proceeds of a deal to buy Treasuries in case it needs the liquidity down the line. This is a simple outline of what is meant when the dollar is spoken of as the world’s reserve currency.

And it is this move away from the dollar as the main facilitator of international commerce that Weinberg sees as driving the value of the greenback lower this year.

“[The dollar’s decline] is not about interest rates,” Weinberg writes.

“It is, instead, anticipation of the dollar being dethroned as the world’s reserve and transactions currency. To our eye, this transition has already begun.”

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland

Read more from Myles here: