Dole (NYSE:DOLE) Posts Better-Than-Expected Sales In Q2

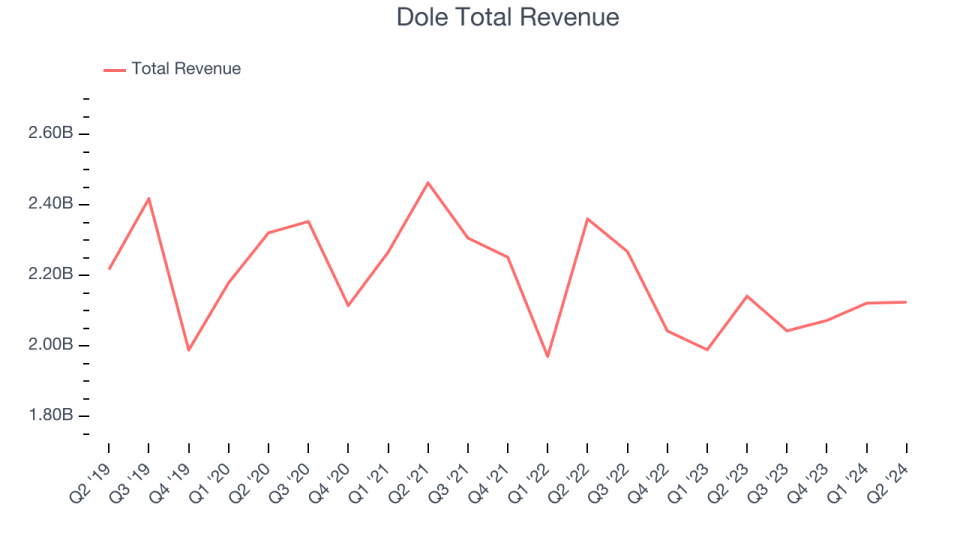

Fresh produce company Dole (NYSE:DOLE) reported Q2 CY2024 results topping analysts’ expectations , with revenue flat year on year at $2.12 billion. It made a non-GAAP profit of $0.49 per share, down from its profit of $0.51 per share in the same quarter last year.

Is now the time to buy Dole? Find out in our full research report.

Dole (DOLE) Q2 CY2024 Highlights:

Revenue: $2.12 billion vs analyst estimates of $2.10 billion (1.3% beat)

EPS (non-GAAP): $0.49 vs analyst estimates of $0.43 (15% beat)

EBITDA guidance for the full year is $370 million at the midpoint, in line with analyst expectations

Gross Margin (GAAP): 9.4%, in line with the same quarter last year

EBITDA Margin: 5.9%, in line with the same quarter last year

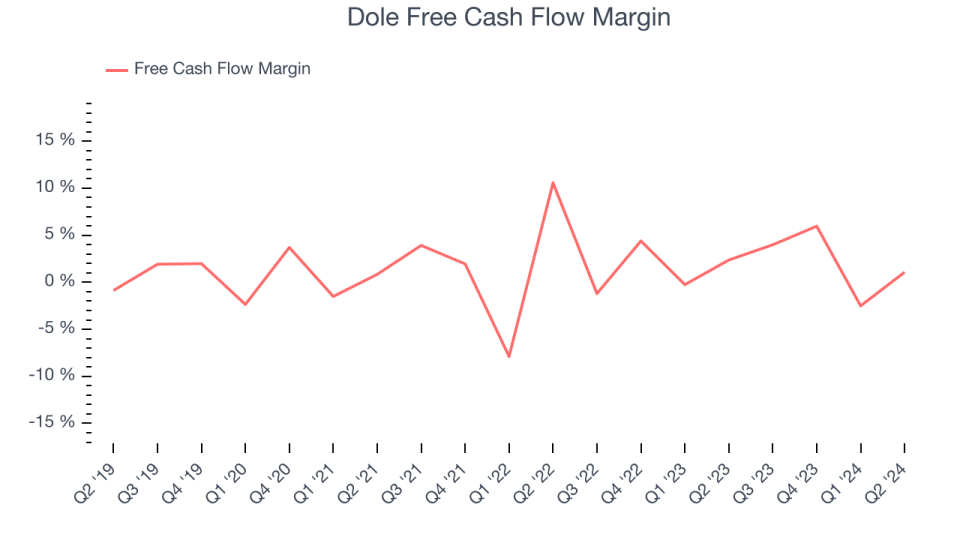

Free Cash Flow Margin: 1.1%, down from 2.4% in the same quarter last year

Market Capitalization: $1.38 billion

______________________ _ 1 Like-for-like basis refers to the measure excluding the impact of foreign currency translation movements and acquisitions and divestitures. 2 Dole plc reports its financial results in accordance with U.S. Generally Accepted Accounting Principles ("GAAP").

Cherished for its delicious, world-famous pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Sales Growth

Dole is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company’s revenue has declined over the last three years, dropping 3.1% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Dole’s revenue fell 0.8% year on year to $2.12 billion but beat Wall Street’s estimates by 1.3%. Looking ahead, Wall Street expects sales to grow 1% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Dole has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.7%, subpar for a consumer staples business.

Taking a step back, we can see that Dole failed to improve its margin during that time. Its unexciting margin and trend likely have shareholders hoping for a change.

Dole’s free cash flow clocked in at $22.76 million in Q2, equivalent to a 1.1% margin. The company’s cash profitability regressed as it was 1.3 percentage points lower than in the same quarter last year. This warrants extra attention because consumer staples companies typically produce more consistent and defensive performance.

Key Takeaways from Dole’s Q2 Results

It was good to see Dole beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. That the company guided full year EBITDA in line with expectations shows that it's very much on track. Overall, this quarter had some key positives. The stock traded up 3.1% to $15 immediately following the results.

Dole may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.