Can Chargepoint Cut Its Way to Profits? It's Trying!

Chargepoint (NYSE: CHPT) is something of a picks-and-shovels play in the electric-vehicle (EV) sector. Providing the things that a growing industry needs has long been a strong business model, but Chargepoint is struggling to earn a profit. That's why it just announced plans to cut costs.

Is this really a good idea?

Chargepoint is a vital cog in EV growth

Chargepoint supports the EV industry by building, selling, and operating EV charging infrastructure. The company covers everything from EV chargers people use at home to the charging systems used by auto fleets.

It operates over 300,000 charge ports, and via roaming agreements, has access to over 700,000. Its network spans across North America and Europe (or some 16 markets).

Although EV adoption is still fairly modest around the world, Chargepoint has built a fairly large network. That's important because EV adoption basically requires that this type of infrastructure be installed. Thus, Chargepoint is doing something very important.

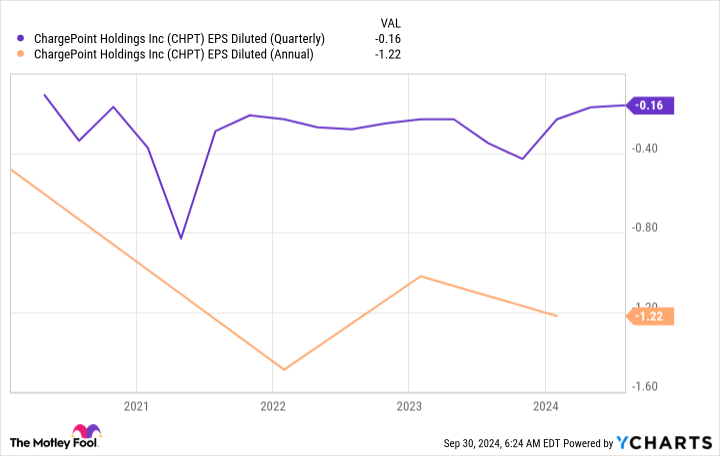

The problem is that building this infrastructure isn't cheap or easy, which is why Chargepoint has yet to turn a full-year profit. It hasn't even spent a single quarter in the black.

It costs a lot of money to build out a network to support an industry that isn't yet fully developed, and there's not much reward for taking on that challenge. Chargepoint's story is basically one of preparing today for a future that's dominated by EVs. You should only buy it if you believe that's what the future holds.

Chargepoint: Trying to make ends meet

The problem, of course, is that companies can't lose money forever. Investors eventually expect profits. A quick look at Chargepoint's stock graph shows exactly what you'd expect.

It came public to a great deal of excitement since it was going to help revolutionize the transportation industry by ushering in the EV revolution. When that revolution didn't happen quickly enough, investors lost interest and the stock plunged.

A low stock price and investors who have taken a show-me attitude is problematic for a developing company like Chargepoint. It makes it harder to raise capital via debt and equity sales.

In effect, Chargepoint has to either find a way to make a profit or at least convince Wall Street that there are profits on the horizon (and the company has the financial wherewithal to survive until that point). This is why Chargepoint just announced a cost-cutting plan.

The initiative will reduce the company's global workforce by 15% and is expected to save around $41 million a year on an annualized basis. That comes out to around $10 million a quarter, which wouldn't have been nearly enough to push Chargepoint into the black in the second quarter.

The company's loss from operations would have still tallied up to more than $50 million. And it's important to note that this isn't the first time Chargepoint has tried to cut its way to a profit, either.

What's a bit worrying about the current round of cuts is that they come from the company's sales and marketing team. During the conference call, management pitched it as increasing the ratio of selling to non-selling positions, which sounds like it's increasing revenue-generating opportunities.

But that isn't the same thing as hiring more people to sell since it could also be accomplished by simply letting more managers go than salespeople. It's particularly hard to cut your way to a profit when the cuts come from the sales team.

Chargepoint is an investment for aggressive investors

While it's good news that Chargepoint knows it has to get lean and mean if it wants to turn a profit, there are real problems here when it comes to cutting costs. For example, the fact that cost-cutting is impacting the division that actually generates revenue is a bit troubling.

Perhaps the sales and marketing team needed to be shaken up, but conservative investors should probably look at this current round of cuts with a show-me attitude. This EV infrastructure play remains a high-risk investment and may be even higher risk following the recent restructuring plan.

Should you invest $1,000 in ChargePoint right now?

Before you buy stock in ChargePoint, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ChargePoint wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $765,523!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 30, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Can Chargepoint Cut Its Way to Profits? It's Trying! was originally published by The Motley Fool