BURL Stock Trading Above 200 & 50-Day SMA: What's Next for Investors?

Burlington Stores, Inc. BURL has demonstrated strong upward momentum, trading above its 200-day and 50-day simple moving averages (SMA). SMA is a key indicator of price stability and long-term bullish trends. BURL closed yesterday’s trading session at $274.76, ahead of its 200-day and 50-day SMA of $220.42 and $262.50, respectively, highlighting a continued uptrend.

This technical strength, along with sustained momentum, reflects positive market sentiment and investor confidence in BURL's financial health and growth prospects.

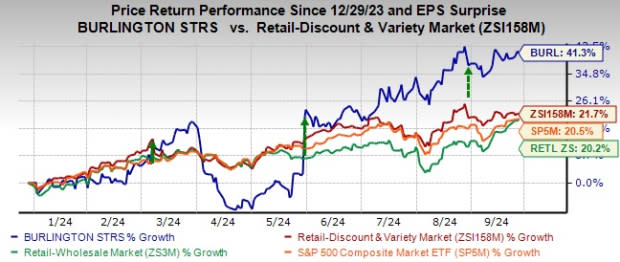

Image Source: Zacks Investment Research

Shares of the company have seen an impressive price surge over the year-to-date period, climbing 41.3% and surpassing the Zacks Retail-Discount Stores industry’s 21.7% growth. This is owing to its effective inventory management and focus on full-price selling, which has also helped it to outperform the broader Retail-Wholesale sector and the S&P 500 index’s respective growth of 20.2% and 20.5% in the same period.

This impressive uptick has left many investors wondering if they missed out on a lucrative opportunity or if there is still potential for growth. This leading off-price retailer is inching toward its 52-week high of $282.49 attained on Aug. 29, 2024, thus reflecting strong investor confidence and market optimism about its future.

Image Source: Zacks Investment Research

BURL Gains on Operational Optimization, Strategic Expansion

Burlington continues to thrive by offering quality merchandise at competitive prices. Its growth strategy revolves around rapid store expansion, operational optimization and strong inventory control, which are key factors in strengthening its market foothold. Burlington’s sustained investments in its supply chain further bolster its long-term growth potential.

In the second quarter of fiscal 2024, Burlington posted an impressive 13.4% year-over-year increase in total sales, exceeding the 9% growth seen in the previous year’s quarter. This performance was largely driven by the addition of 36 net new stores, increasing the total store count to 1,057. The company is on track to open 100 more stores and relocate 30 by the close of fiscal 2024.

Comparable store sales saw a robust 5% increase, surpassing the company’s projected range of flat to 2%. This success was fueled by a 7% rise in full-price sales and a reduction in markdowns during the quarter. Despite concerns regarding possible new store cannibalization, Burlington's focus on merchandising excellence and improved customer engagement helped sustain sales momentum.

Operating margins also expanded 160 basis points, supported by improvements in gross margins and supply-chain efficiencies. The gross margin increased 110 basis points to 42.8%, driven by faster inventory turnover and fewer markdowns.

Burlington’s Growth Prospects

Burlington has updated its fiscal 2024 guidance, signaling a stronger outlook. Total sales are now expected to rise between 9% and 10%, up from the previously estimated range of 8-10%. Comparable store sales are projected to grow in the band of 2-3%, an improvement from the earlier forecast of 0-2%.

The adjusted EBIT margin is forecasted to increase in the range of 50-70 basis points, higher than the prior estimated band of 40-60 basis points. Adjusted earnings per share (EPS) are now expected to be in the range of$7.66-$7.96, up from the previous guided band of $7.35-$7.75.

For the third quarter, Burlington anticipates a total sales increase of 10-12%, with comparable sales growth of 0-2% and an adjusted EBIT margin improvement of 60-80 basis points. In the fourth quarter, comparable sales are forecasted to remain flat or rise up to 2%, with total sales growth expected in the range of 5-7%.

Burlington Stock’s Attractive Valuation

From a valuation perspective, the stock presents an attractive opportunity, trading at a discount relative to the industry benchmark. With a forward 12-month price-to-sales ratio of 1.53, which is below the five-year industry average of 1.74, the stock offers compelling value for investors seeking exposure to the sector. It currently has a Value Score of A, further validating its appeal.

Image Source: Zacks Investment Research

Estimate Revisions Favor BURL Stock

The Zacks Consensus Estimate for EPS has been revised upward, reflecting the positive sentiment around Burlington. Over the past 30 days, analysts have increased their estimates for the current year by 21 cents to $7.91 per share and the next year by 24 cents to $9.55. These estimates indicate year-over-year growth of 30.5% and 20.7%, respectively.

Image Source: Zacks Investment Research

Conclusion

Investors should consider BURL stock due to its impressive performance and positive market sentiment. The company is trading above key moving averages, indicating strong upward momentum. BURL has significantly outperformed its industry peers, driven by effective inventory management and a focus on full-price selling. With strategic plans for store expansion and a revised fiscal outlook that signals continued growth, Burlington demonstrates robust growth prospects. Additionally, its attractive valuation and upward revisions in earnings estimates make it an appealing investment opportunity for those seeking to benefit from its operational excellence. It currently has a Zacks Rank #2 (Buy).

Other Stocks to Consider

Other top-ranked stocks are Nordstrom Inc. JWN, Abercrombie & Fitch Co. ANF and Crocs, Inc. CROX.

Nordstrom is a leading fashion specialty retailer in the United States. The company offers an extensive selection of both branded and private-label merchandise. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nordstrom’s fiscal 2024 sales indicates growth of 0.6% from the fiscal 2023 figure. JWN has a negative trailing four-quarter average earnings surprise of 17.8%.

Abercrombie is a specialty retailer of premium, high-quality casual apparel. It sports a Zacks Rank of 1 at present. ANF delivered a 16.8% earnings surprise in the last reported quarter.

The consensus estimate for Abercrombie’s fiscal 2025 earnings and sales indicates growth of 63.4% and 13.1%, respectively, from the fiscal 2024 levels. ANF has a trailing four-quarter average earnings surprise of 28%.

Crocs offers a wide variety of footwear products, including sandals, wedges, flips and slides that cater to people of all ages. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for Crocs’ 2024 earnings and sales indicates growth of 6.8% and 4%, respectively, from 2023’s figures. CROX has a trailing four-quarter average earnings surprise of 14.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Burlington Stores, Inc. (BURL) : Free Stock Analysis Report