Best Stock to Buy Right Now: Kraft Heinz vs. Hershey

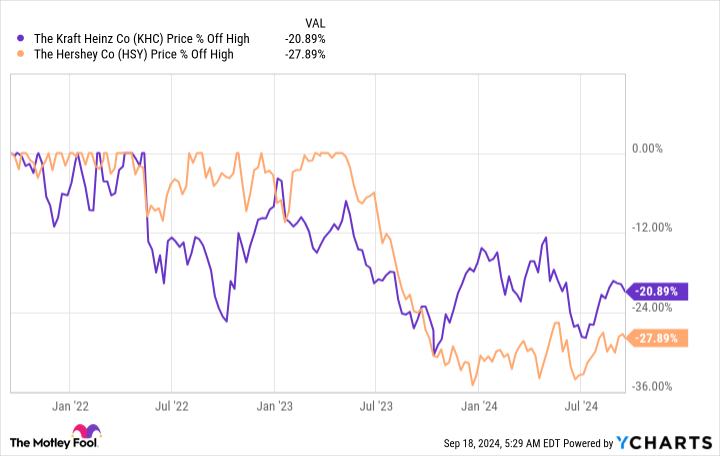

If you're looking at the consumer staples sector and trying to find bargains, you'll want to consider Kraft Heinz (NASDAQ: KHC) and Hershey (NYSE: HSY). Both own iconic brands, but their stocks have performed fairly poorly of late. Kraft Heinz is 20% below its three-year high, while Hershey is around 25% below its three-year peak.

Is this an opportunity to get in on two great companies, or is one of these food makers a better stock to buy right now?

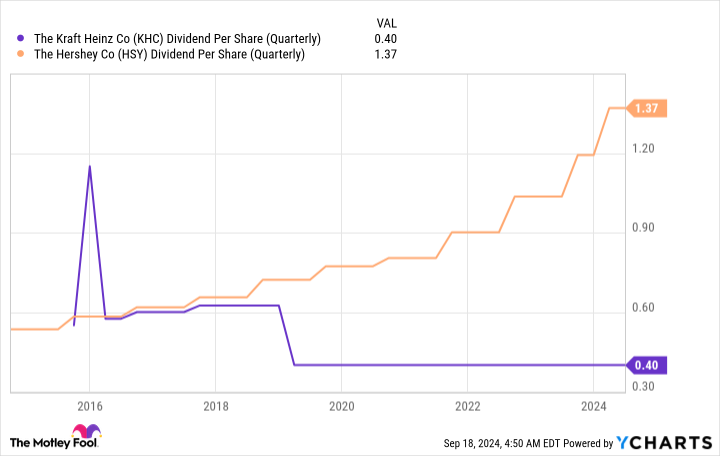

A comparison of dividends

If you are an income investor, the first thing you're likely to examine is a stock's dividend yield. On that front, Kraft Heinz is the standout, with a 4.5% yield. Hershey's yield is only 2.7%. The word "only" may be a bit excessive, given that the S&P 500 index yields a scant 1.2%.

It's also worth noting that the average consumer staples stock, using the Consumer Staples Select Sector SPDR Fund as a proxy, has a 2.6% yield. So Kraft Heinz does have a higher yield, but Hershey's dividend yield isn't exactly bad. In fact, it's toward the high end of its historic yield range.

After dividend yield, the next key factor to look at is the dividend backing that yield. Here Kraft Heinz doesn't look nearly as good, given the dividend cut just before the start of the 2020s. The dividend has flatlined since it was cut. (Kraft Heinz's yield range isn't really as relevant because of the recent cut.)

By contrast, Hershey's dividend has grown steadily for years, with an annual increase streak that's currently 15 years long. If dividend consistency is important to you, Hershey is the clear winner.

Why are investors so negative about Kraft Heinz?

The stocks of Kraft Heinz and Hershey are both down from their highs for good reasons. Investors need to understand why before buying.

In Kraft Heinz's case, the company was created via a merger of two iconic food makers. The plan was to cut costs to boost profits. That didn't pan out nearly as well as hoped, even though some very high-profile investors, specifically Warren Buffett of Berkshire Hathaway, were behind the deal.

In the end, cost cutting is a hard way to grow a business. Kraft Heinz had to shift gears, focusing on basics like innovation and brand building. It also needed to trim debt, which spiked thanks to the merger.

To be fair, a lot has been accomplished. Kraft Heinz's plan is now to slim down its portfolio and focus on its best brands. This is a good plan, but recent performance hasn't been great. For example, the key brands it's focusing on in North America, its largest market, saw organic sales drop 2.4% in the second quarter of 2024.

If that's the result from the company's new focus, you can understand why investors are taking a show-me attitude. To be fair, Kraft Heinz is better positioned today than it was just a few years ago, but this is still something of a turnaround story.

Why are investors so negative about Hershey?

Hershey's tale is a bit more complicated. First, the company just upgraded its distribution systems, which has caused a strange wrinkle in its earnings. Before the switch to the new system, inventory was built up so that retailers wouldn't be left high and dry if there was a problem. That boosted earnings. Now, after a successful switchover, that inventory is being worked off, which is depressing earnings.

Hershey's business is also highly seasonal. Holidays lead to demand spikes. But some of the most important holidays for Hershey move between quarters, which caused earnings to be a bit volatile. That was a negative in the most recent quarter, too. Neither of these two problems is likely to be a lingering issue.

Harder to define is the effect of rising cocoa prices, a key ingredient in the chocolates for which Hershey is known. Troubles in the cocoa supply chain suggest that this commodity might have permanently moved into a higher price range. However, Hershey has long dealt with inflation and commodity price fluctuations, notably by adjusting prices, products, and package sizes. It's doing that again and, in time, will probably be able to deal with higher cocoa prices. Note that chocolate is a relatively inexpensive luxury to a lot of people.

Even more difficult to assess is the effect of new weight loss drugs that may change consumer eating habits. But chocolate is, as noted, a low-cost indulgence that people really like to eat. It seems likely that demand won't disappear, particularly when you consider that people are generally bad at sticking to medication regimens over time. This is a bit of a wild card, but like all the other issues facing Hershey today, it seems likely that it won't derail the company over the long term.

In other words, investors may be unduly negative on Hershey today. That could make this a solid contrarian play for investors who think in decades and not days.

You should probably lean toward Hershey

If you are focused entirely on dividend yield, you will likely buy Kraft Heinz. But that company's problems seem to be a bit harder to deal with and, notably, self-imposed. That's not to suggest it won't turn its business around, only that the process could be a long one as management works to fundamentally change the way the business is run. With no dividend growth on the horizon, you could be missing out if you buy for yield.

Hershey's list of troubles is a bit longer. Two are temporary (system upgrade and seasonal sales swings). Two are a bit longer-term (cocoa prices and weight loss drugs). But none seem likely to be insurmountable, given the love people have for sweet treats. At this point, it doesn't look like Hershey needs to fundamentally change its business in any way.

Hershey seems like the more attractive investment. Despite all the headwinds, it's still growing its dividend steadily -- that's a statement about the expectations that the company has about its future.

Should you invest $1,000 in Kraft Heinz right now?

Before you buy stock in Kraft Heinz, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Kraft Heinz wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $710,860!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

Reuben Gregg Brewer has positions in Hershey. The Motley Fool has positions in and recommends Berkshire Hathaway and Hershey. The Motley Fool recommends Kraft Heinz. The Motley Fool has a disclosure policy.

Best Stock to Buy Right Now: Kraft Heinz vs. Hershey was originally published by The Motley Fool