ADT (NYSE:ADT) Reports Q2 In Line With Expectations

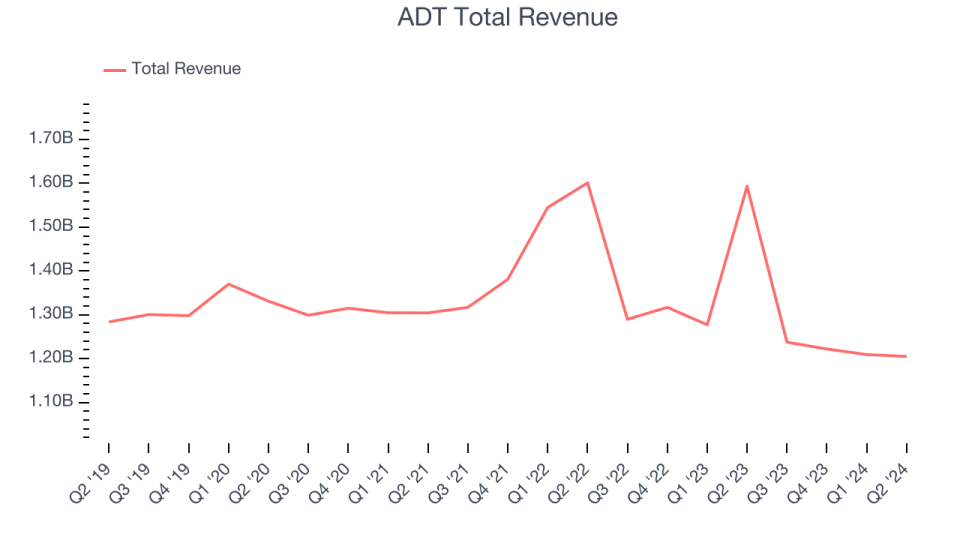

Security technology and services company ADT (NYSE:ADT) reported results in line with analysts' expectations in Q2 CY2024, with revenue down 24.4% year on year to $1.21 billion. It made a non-GAAP profit of $0.17 per share, down from its profit of $0.20 per share in the same quarter last year.

Is now the time to buy ADT? Find out in our full research report.

ADT (ADT) Q2 CY2024 Highlights:

Revenue: $1.21 billion vs analyst estimates of $1.21 billion (small miss)

EPS (non-GAAP): $0.17 vs analyst expectations of $0.17 (in line)

EPS (non-GAAP) Guidance for the full year is $0.70 at the midpoint, beating analysts' estimates by 1.4%

Gross Margin (GAAP): 83.7%, up from 69.6% in the same quarter last year

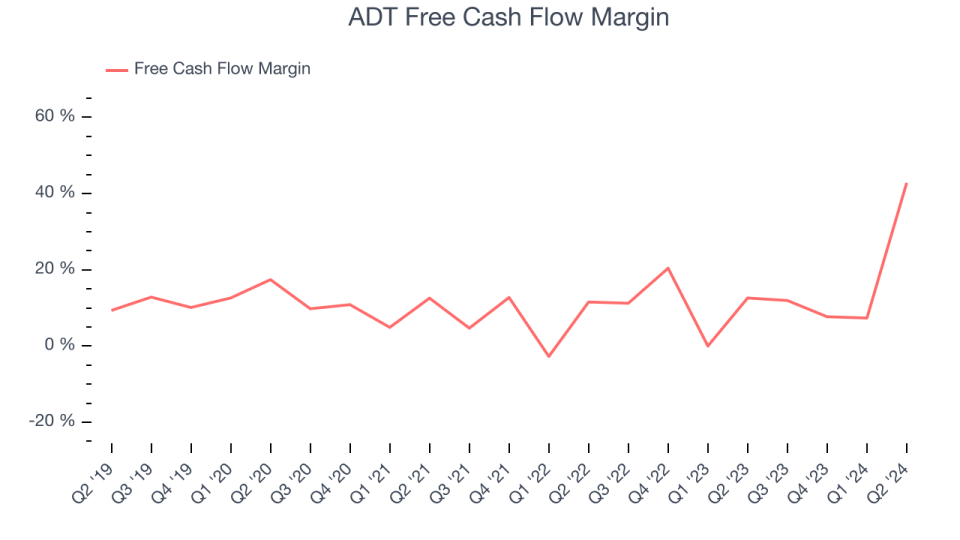

Free Cash Flow of $516 million, up from $89 million in the previous quarter

Market Capitalization: $7.01 billion

“ADT delivered a solid first half with continued revenue growth momentum, as well as strong operating profitability and cash flow generation. With our streamlined focus on the consumer and small business markets, we continue to expand and improve our innovative offerings, unrivaled safety, and premium experience for security and smart home customers,” said ADT Chairman, President, and CEO, Jim DeVries.

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE:ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Over the last five years, ADT's sales were flat. This shows demand was soft and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. ADT's recent history shows its demand has stayed suppressed as its revenue has declined by 8.7% annually over the last two years.

This quarter, ADT reported a rather uninspiring 24.4% year-on-year revenue decline to $1.21 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.4% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

ADT has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company's free cash flow margin averaged 14.1% over the last two years, better than the broader consumer discretionary sector.

ADT's free cash flow clocked in at $516 million in Q2, equivalent to a 42.8% margin. This quarter's result was good as its margin was 30.2 percentage points higher than in the same quarter last year, but we wouldn't read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Key Takeaways from ADT's Q2 Results

It was encouraging to see ADT slightly top analysts' full-year earnings guidance expectations. Zooming out, we think this was a decent quarter, showing the company is staying on target. The stock traded up 1.6% to $7.90 immediately following the results.

So should you invest in ADT right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.