3 US Stocks Estimated To Be 12.8%-44.8% Below Intrinsic Value

After a volatile August, U.S. stocks ended the month with gains as major indexes rebounded from early declines, buoyed by easing economic fears and expectations of Federal Reserve rate cuts. This environment presents an opportunity to explore undervalued stocks, which can offer significant upside potential when markets stabilize. Identifying undervalued stocks involves assessing their intrinsic value relative to current market prices. In this article, we'll examine three U.S. stocks that are estimated to be between 12.8% and 44.8% below their intrinsic value, making them compelling considerations in today's market landscape.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

Name | Current Price | Fair Value (Est) | Discount (Est) |

Amdocs (NasdaqGS:DOX) | $86.97 | $173.25 | 49.8% |

Heartland Financial USA (NasdaqGS:HTLF) | $55.76 | $109.57 | 49.1% |

California Resources (NYSE:CRC) | $52.47 | $104.70 | 49.9% |

Tompkins Financial (NYSEAM:TMP) | $61.34 | $122.40 | 49.9% |

Progress Software (NasdaqGS:PRGS) | $58.15 | $115.14 | 49.5% |

Fluence Energy (NasdaqGS:FLNC) | $18.37 | $35.93 | 48.9% |

STAAR Surgical (NasdaqGM:STAA) | $33.09 | $65.37 | 49.4% |

WEX (NYSE:WEX) | $191.02 | $377.68 | 49.4% |

Bilibili (NasdaqGS:BILI) | $14.38 | $28.71 | 49.9% |

Alnylam Pharmaceuticals (NasdaqGS:ALNY) | $262.69 | $512.94 | 48.8% |

Here's a peek at a few of the choices from the screener.

GlobalFoundries

Overview: GlobalFoundries Inc., with a market cap of $25.76 billion, is a semiconductor foundry that offers a variety of mainstream wafer fabrication services and technologies globally.

Operations: The company generates $6.89 billion from its semiconductor segment.

Estimated Discount To Fair Value: 30.2%

GlobalFoundries (GF) appears undervalued based on cash flows, trading at US$46.68, below its estimated fair value of US$66.91. Despite a forecasted annual earnings growth of 23%, profit margins have declined from 19.1% to 11.8% over the past year. Recent strategic partnerships, including agreements with Finwave Semiconductor and Efficient for advanced semiconductor technologies, could enhance GF’s manufacturing capabilities and market position, potentially improving future cash flows and profitability metrics.

Zscaler

Overview: Zscaler, Inc. operates as a cloud security company worldwide with a market cap of $30.23 billion.

Operations: Revenue from subscription services to Zscaler's cloud platform and related support services totals $2.03 billion.

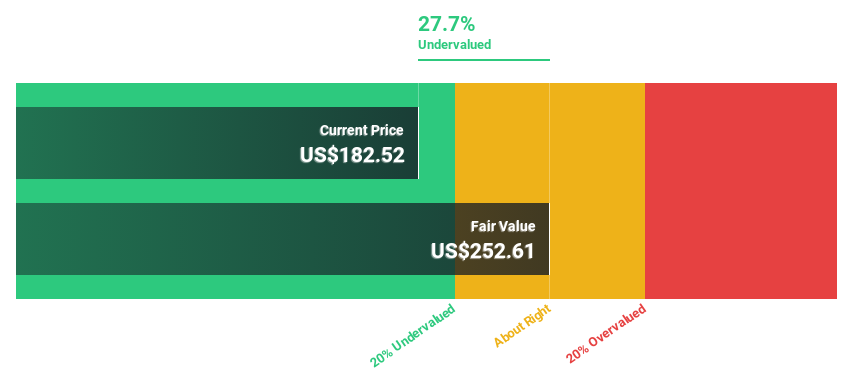

Estimated Discount To Fair Value: 44.8%

Zscaler, trading at US$199.98, is significantly undervalued with an estimated fair value of US$362.22. Despite recent shareholder dilution and insider selling, the company is forecast to achieve profitability in the next three years and boasts a high expected annual profit growth of 45.69%. Recent partnerships with SecureDynamics and Wipro enhance its cybersecurity offerings, potentially driving future revenue growth at 17.7% per year—outpacing the broader US market's growth rate.

Eli Lilly

Overview: Eli Lilly and Company discovers, develops, and markets human pharmaceuticals worldwide with a market cap of $864.43 billion.

Operations: The company's revenue primarily comes from the discovery, development, manufacturing, marketing, and sales of pharmaceutical products totaling $38.92 billion.

Estimated Discount To Fair Value: 12.8%

Eli Lilly, trading at US$960.02, is undervalued relative to its estimated fair value of US$1100.48. The company’s earnings are forecast to grow significantly at 28.8% annually over the next three years, outpacing the broader US market's growth rate of 15%. Recent positive results from the SURMOUNT-1 study for tirzepatide and an expanded distribution agreement for Emgality® bolster future revenue prospects, which are expected to grow faster than the overall market (16.8% vs 8.7%).

The growth report we've compiled suggests that Eli Lilly's future prospects could be on the up.

Unlock comprehensive insights into our analysis of Eli Lilly stock in this financial health report.

Key Takeaways

Click through to start exploring the rest of the 196 Undervalued US Stocks Based On Cash Flows now.

Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGS:GFS NasdaqGS:ZS and NYSE:LLY.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com