3 US Growth Companies With High Insider Ownership

As the Dow Jones Industrial Average reaches new highs and investors await a pivotal Federal Reserve decision, the focus on growth companies with high insider ownership becomes particularly relevant. In this environment, stocks with substantial insider stakes can be appealing due to their potential for aligned interests between management and shareholders, which may foster long-term growth and stability.

Top 10 Growth Companies With High Insider Ownership In The United States

Name | Insider Ownership | Earnings Growth |

Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 27.1% |

Hims & Hers Health (NYSE:HIMS) | 13.7% | 40.7% |

Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95% |

EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

Underneath we present a selection of stocks filtered out by our screen.

ChromaDex

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ChromaDex Corporation operates as a bioscience company focusing on developing healthy aging products, with a market cap of $270.16 million.

Operations: ChromaDex Corporation generates revenue from three main segments: Ingredients ($11.70 million), Consumer Products ($71.00 million), and Analytical Reference Standards and Services ($2.88 million).

Insider Ownership: 30.7%

Revenue Growth Forecast: 18% p.a.

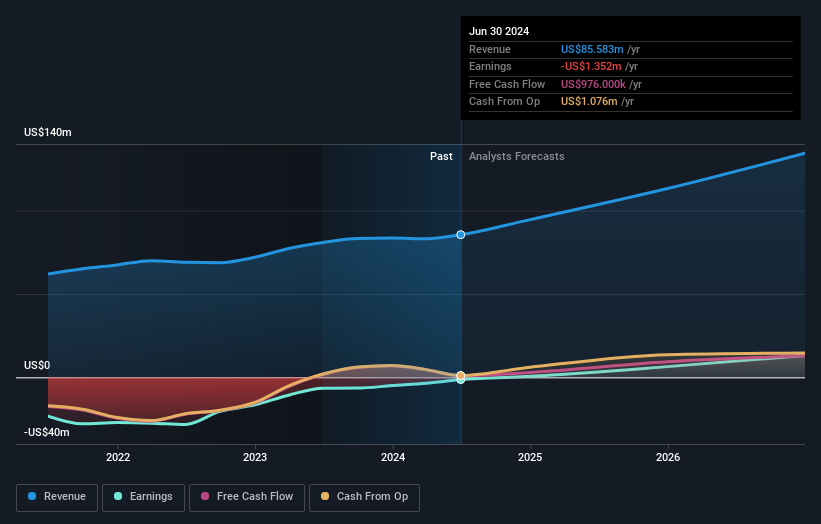

ChromaDex, a growth company with high insider ownership, is forecast to grow revenue at 18% per year, outpacing the US market. Despite recent volatility in its share price, it trades at 51.8% below fair value estimates and has shown consistent earnings growth of 29.3% annually over the past five years. The company aims for profitability within three years and recently secured $32 million through a private placement with Brilliant Dynasty Limited while reiterating its annual revenue growth guidance of 10%-15%.

Victory Capital Holdings

Simply Wall St Growth Rating: ★★★★★★

Overview: Victory Capital Holdings, Inc., along with its subsidiaries, operates as an asset management company both in the United States and internationally, with a market cap of approximately $3.37 billion.

Operations: The company generates revenue of $850.96 million through its investment management services and products.

Insider Ownership: 10.2%

Revenue Growth Forecast: 22.8% p.a.

Victory Capital Holdings is forecast to grow revenue at 22.8% per year, significantly outpacing the US market. The company's earnings have grown 14.4% annually over the past five years and are expected to increase by 32.3% per year moving forward. Despite a high level of debt and an unstable dividend track record, it trades at a substantial discount of 65.4% below fair value estimates and maintains strong insider ownership, enhancing alignment with shareholders' interests.

XPeng

Simply Wall St Growth Rating: ★★★★★☆

Overview: XPeng Inc. designs, develops, manufactures, and markets smart electric vehicles (EVs) in the People’s Republic of China with a market cap of $8.50 billion.

Operations: The company generates revenue primarily from its Auto Manufacturers segment, which reported CN¥36.24 billion.

Insider Ownership: 23.5%

Revenue Growth Forecast: 25.5% p.a.

XPeng Inc. embodies significant growth potential with high insider ownership, evidenced by recent substantial insider purchases. The company is forecast to achieve profitability within three years, outpacing average market growth. Revenue is expected to grow at 25.5% annually, significantly faster than the US market's 8.8%. Despite past shareholder dilution and a projected low return on equity of 6.2%, XPeng trades at a notable discount of 23.2% below estimated fair value, underscoring its strong growth trajectory and commitment to innovation in AI-driven smart EVs.

Click here and access our complete growth analysis report to understand the dynamics of XPeng.

Our expertly prepared valuation report XPeng implies its share price may be lower than expected.

Where To Now?

Investigate our full lineup of 175 Fast Growing US Companies With High Insider Ownership right here.

Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include NasdaqCM:CDXC NasdaqGS:VCTR and NYSE:XPEV.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com