3 US Growth Companies With High Insider Ownership Growing Earnings Up To 61%

As the U.S. stock market experiences a mixed performance with investors closely monitoring economic data and job reports, it's crucial to identify companies that demonstrate resilience and potential for growth. One key indicator of a promising investment is high insider ownership, which often signals confidence in the company's future prospects.

Top 10 Growth Companies With High Insider Ownership In The United States

Name | Insider Ownership | Earnings Growth |

Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

Hims & Hers Health (NYSE:HIMS) | 13.7% | 40.7% |

On Holding (NYSE:ONON) | 28.4% | 24.4% |

Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95.9% |

Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

BBB Foods (NYSE:TBBB) | 22.9% | 91.3% |

Let's explore several standout options from the results in the screener.

Vivid Seats

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vivid Seats Inc. operates an online ticket marketplace in the United States, Canada, and Japan, with a market cap of $963.43 million.

Operations: The company's revenue segments include $123.89 million from Resale and $651.72 million from Marketplace operations.

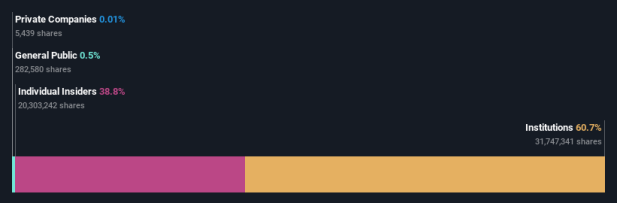

Insider Ownership: 10.7%

Earnings Growth Forecast: 30.1% p.a.

Vivid Seats Inc. showcases high insider ownership and notable growth potential, despite recent challenges. The company announced an exclusive media deal with I Am Athlete, enhancing its brand visibility and fan engagement. However, it revised its revenue guidance slightly downward to US$810-830 million for 2024. Despite a net loss in Q2 2024 and reduced profit margins, earnings are forecasted to grow significantly at 30% annually, indicating strong future profitability prospects.

Ameresco

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ameresco, Inc. (NYSE:AMRC) is a clean technology integrator offering energy efficiency and renewable energy solutions across the United States, Canada, Europe, and internationally with a market cap of approximately $1.53 billion.

Operations: Revenue segments for Ameresco, Inc. include $207.40 million from Europe, $410.94 million from U.S. Federal, and $137.13 million from Alternative Fuels.

Insider Ownership: 37%

Earnings Growth Forecast: 28.1% p.a.

Ameresco, Inc. exemplifies a growth company with high insider ownership, driven by its strategic focus on renewable energy projects and innovative solutions. Recent milestones include a significant solar PV canopy project in Pendleton and substantial battery energy storage system agreements with Southern California Edison and Snohomish County PUD. Despite recent earnings challenges, Ameresco's revenue is forecast to grow faster than the US market at 11% annually, with earnings projected to increase by 28.1% per year over the next three years.

Get an in-depth perspective on Ameresco's performance by reading our analyst estimates report here.

The valuation report we've compiled suggests that Ameresco's current price could be quite moderate.

Ryan Specialty Holdings

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ryan Specialty Holdings, Inc. provides specialty products and solutions for insurance brokers, agents, and carriers across the United States, Canada, the United Kingdom, Europe, and Singapore with a market cap of $16.74 billion.

Operations: Ryan Specialty Holdings generates $2.22 billion from its Insurance Brokers segment.

Insider Ownership: 18.2%

Earnings Growth Forecast: 61.1% p.a.

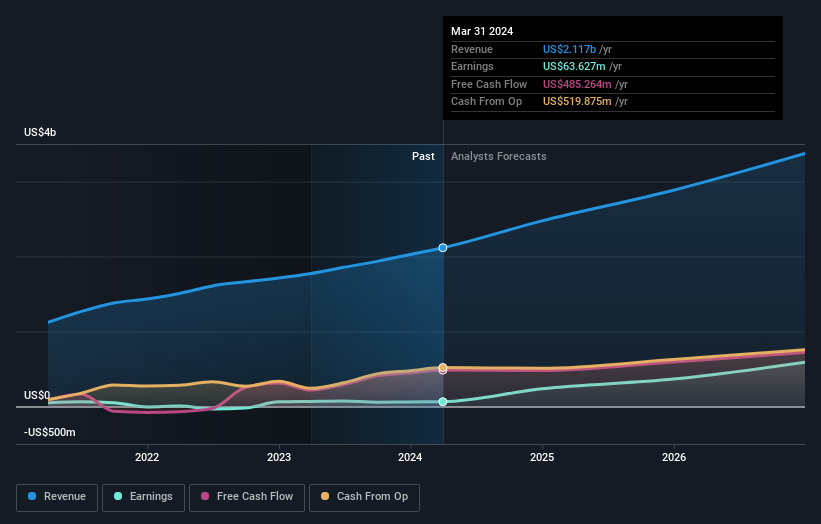

Ryan Specialty Holdings stands out due to its strong insider ownership and impressive growth prospects. The company's revenue grew to US$695.44 million in Q2 2024, up from US$585.15 million a year ago, with net income rising to US$118.04 million from US$83.82 million. Earnings are forecasted to grow significantly at 61% annually over the next three years, outpacing the broader market's 14.9%. However, high debt levels and recent substantial insider selling warrant caution despite robust financial performance and strategic partnerships like the one with Private Client Select Insurance Services LLC for exclusive distribution in high-net-worth markets.

Turning Ideas Into Actions

Dive into all 182 of the Fast Growing US Companies With High Insider Ownership we have identified here.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include NasdaqGS:SEAT NYSE:AMRC and NYSE:RYAN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com