3 Reasons to Buy ON Semiconductor Stock Like There's No Tomorrow

One of growth investors' biggest complaints is the need for more growth stock candidates at reasonable valuations. Such situations rarely arise when a company is firing on all cylinders.

Still, you can often buy a stock at a reasonable valuation when the market has fallen out of love with it due to temporary weakness in its end markets. That seems to be the case with ON Semiconductor (NASDAQ: ON). The stock deserves a closer look from growth-oriented investors, and here are three reasons why.

The long-term growth story

The investment case for the stock rests on management's pivot toward the automotive and industrial end markets. ON Semiconductor's intelligent technology is used in electric vehicles (EVs) and hybrid electric vehicles (HEVs), and helps reduce their weight, make them run longer, and charge more quickly.

Meanwhile, the company's advanced sensing technologies are vital to smart factories and facilities. They're also used in the automotive industry in advanced driver assistance systems (ADAS) and automated driver systems. Management continues to structure the company for long-term growth in these end markets.

The slowdown is temporary

It's fair to say that none of these end markets are in fighting shape in 2024 -- at least not relative to expectations going into the year. Relatively high interest rates have slowed EV sales, and automakers have cut back on development spending. The situation is similar in the industrial sector, with a marked slowdown in industrial automation orders.

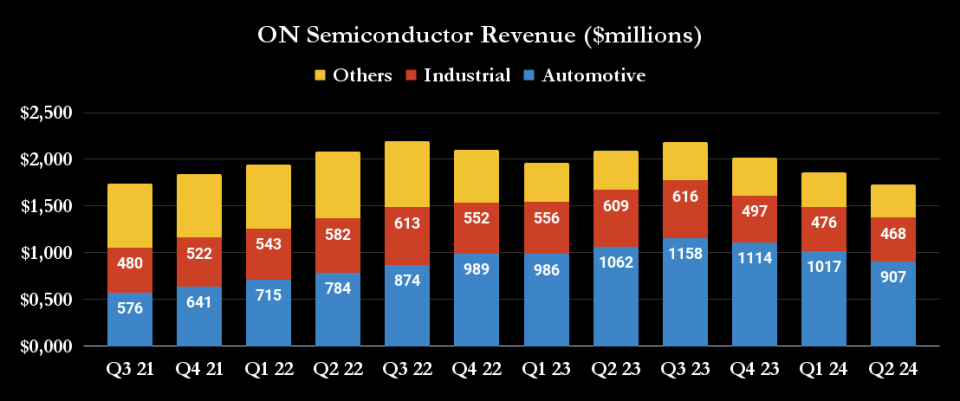

The chart below shows the nature of the decline in its key industrial and automotive end markets.

That said, the reasons for the revenue decline look temporary and relate to a high-interest-rate market. With lower interest rates on the way, EV/HEV sales should pick up, leading to investment flowing into expanding production. In a demonstration of the auto industry's commitment to investing in EVs, ON Semiconductor recently inked a multiyear deal with Volkswagen to be the primary supplier of power-box solutions.

In addition, there's been a slowdown in factory automation spending, evidenced by the order patterns of companies with exposure, such as Emerson Electric and Rockwell Automation. This combination of slowing growth and automation-product distributors running down inventory rather than placing new orders appears temporary.

There's a reason why companies like Emerson Electric, Siemens, and Honeywell are making automation a key focus of their growth plans. Factory automation allows developed countries to compete on cost with low-cost countries in manufacturing.

Attractive valuation

There's no way of avoiding the elephant in the room: ON Semiconductor's sales are declining and set to fall in 2024. Moreover, CEO Hassane El-Khoury is talking of an "L-shaped" recovery, meaning a slow and gradual recovery will follow the steep decline.

The good news is that a conservative outlook is baked into the stock's valuation.

To indicate the company's attractive valuation, here's a look at some standard valuation multiples using the Wall Street analyst consensus. They're excellent multiples for a growth stock passing through a trough in revenue and earnings in 2024, implying that the market doesn't believe in the Wall Street consensus. In the last case, EV is enterprise value (market cap plus net debt) divided by earnings before interest, taxation, depreciation, and amortization (EBITDA).

ON Semiconductor | 2023 | 2024Est | 2025Est | 2026Est |

|---|---|---|---|---|

Price/earnings | 17.1x | 19.4x | 15.5x | 12x |

Price/free cash flow | 91.7x | 22.1x | 15.1x | 12.6x |

EV/EBITDA | 11.4x | 11.5x | 9.6x | 7.6x |

Data source: marketscreener.com, author's analysis.

The market has reason to doubt the numbers. No one can feel entirely comfortable in a company with declining sales, but if the market is wrong, then the upside potential is significant.

A stock to buy?

Suppose you believe the automotive sector's future lies in EVs/HEVs, ADAS, and automated driving systems, rather than traditional internal combustion engines (ICE). In that case, you may believe that ON Semiconductor has a bright future -- not least because it generates significantly more content per vehicle on EVs than on ICE-powered vehicles.

Moreover, the stock will be attractive if you like the megatrend toward factory automation, renewable energy, and EV charging networks.

These industries aren't going to recover quickly. That said, the underlying drivers -- clean energy (EVs, etc.) and manufacturing productivity gains through automation investments -- are in place.

Should you invest $1,000 in ON Semiconductor right now?

Before you buy stock in ON Semiconductor, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ON Semiconductor wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $722,320!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Emerson Electric and Volkswagen. The Motley Fool recommends ON Semiconductor and Volkswagen Ag. The Motley Fool has a disclosure policy.

3 Reasons to Buy ON Semiconductor Stock Like There's No Tomorrow was originally published by The Motley Fool