3 Japanese Growth Stocks With Up To 36% Insider Ownership

Japan's stock markets recently experienced sharp losses as investors reacted to new political developments, with the Nikkei 225 and TOPIX indices showing declines despite a more dovish tone from the country's new leadership. Amid these fluctuations, growth companies with high insider ownership can offer unique insights into potential long-term value, as insider stakes may indicate confidence in a company's future prospects.

Top 10 Growth Companies With High Insider Ownership In Japan

Name | Insider Ownership | Earnings Growth |

Micronics Japan (TSE:6871) | 15.3% | 31.5% |

Hottolink (TSE:3680) | 26.1% | 61.5% |

Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 38.5% |

Medley (TSE:4480) | 34% | 30.4% |

Inforich (TSE:9338) | 19.1% | 29.5% |

Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

ExaWizards (TSE:4259) | 22% | 75.2% |

Money Forward (TSE:3994) | 21.4% | 68.1% |

Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

Soracom (TSE:147A) | 16.5% | 54.1% |

Let's review some notable picks from our screened stocks.

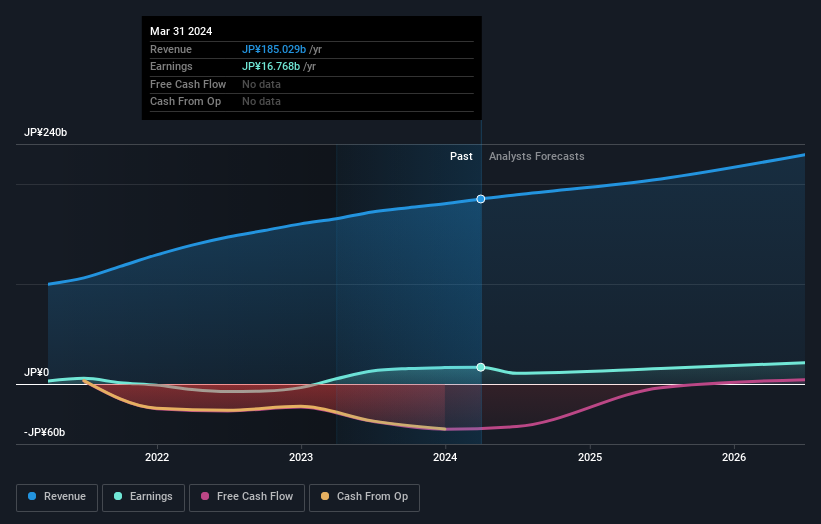

Kasumigaseki CapitalLtd

Simply Wall St Growth Rating: ★★★★★★

Overview: Kasumigaseki Capital Co., Ltd. operates in Japan's real estate consulting sector with a market capitalization of ¥174.34 billion.

Operations: Kasumigaseki Capital Co., Ltd. generates revenue through its real estate consulting operations in Japan.

Insider Ownership: 34.7%

Kasumigaseki Capital Ltd. demonstrates strong growth potential, with earnings forecasted to increase significantly at 38.54% annually over the next three years, outpacing the Japanese market average. Despite high volatility in its share price and past shareholder dilution, the company shows promising revenue growth of 26.3% per year. Recent expansions include a new luxury venture, seven x seven Ishigaki, enhancing its hospitality portfolio and potentially driving further revenue increases in this segment.

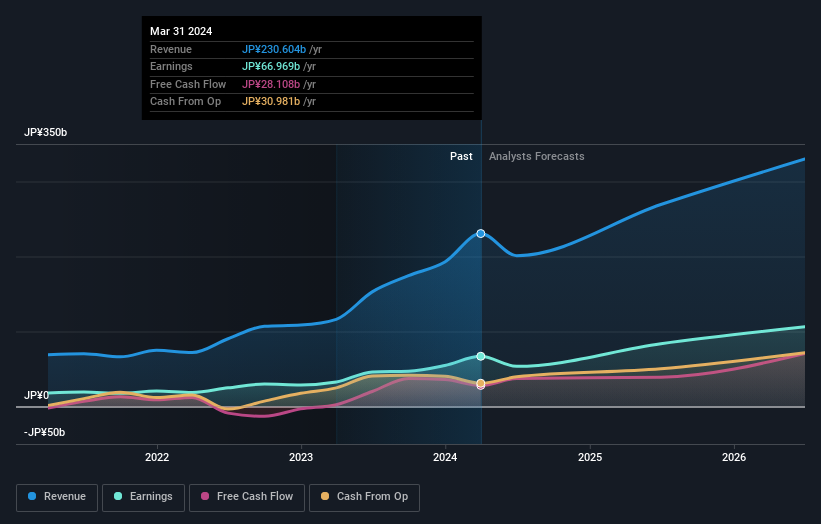

Mercari

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Mercari, Inc. is a company that plans, develops, and operates marketplace applications in Japan and the United States with a market cap of ¥434.96 billion.

Operations: The company generates revenue from its marketplace applications, with ¥43.65 billion from the United States and ¥138.11 billion from Japan.

Insider Ownership: 36%

Mercari, Inc. exhibits growth potential with earnings forecasted to rise 17.7% annually, outpacing the Japanese market average of 8.7%. Despite recent share price volatility and slower revenue growth at 6.9% per year compared to significant benchmarks, its core operating profit is projected between ¥22 billion and ¥25 billion for fiscal year ending June 2025. Mercari's strong return on equity forecast of 21.8% in three years underscores its financial health amidst high-quality earnings metrics.

Take a closer look at Mercari's potential here in our earnings growth report.

The valuation report we've compiled suggests that Mercari's current price could be inflated.

Lasertec

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lasertec Corporation designs, manufactures, and sells inspection and measurement equipment both in Japan and internationally, with a market cap of ¥2.18 trillion.

Operations: Lasertec's revenue primarily comes from its design, production, and distribution of inspection and measurement equipment across domestic and international markets.

Insider Ownership: 11.1%

Lasertec Corporation demonstrates growth potential with earnings expected to grow at 15.8% annually, surpassing the Japanese market's average of 8.7%. Despite high share price volatility, its revenue is forecasted to increase by 13.2% per year, faster than the market's 4.2%. Recent developments include the launch of SICA108 for SiC wafer inspection, enhancing quality and cost efficiency in production processes. The company's return on equity is projected to be very high at 41.4% in three years.

Next Steps

Reveal the 101 hidden gems among our Fast Growing Japanese Companies With High Insider Ownership screener with a single click here.

Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include TSE:3498 TSE:4385 and TSE:6920.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com