3 Companies On SIX Swiss Exchange That Might Be Trading Below Their Estimated Value

The Swiss market demonstrated resilience by recovering from a weak start, buoyed by the European Central Bank's decision to cut its key interest rate, which helped propel the SMI index to a notable gain. Amidst these shifting economic conditions and narrowing trade surplus, investors are increasingly interested in identifying stocks that may be trading below their estimated value on the SIX Swiss Exchange.

Top 10 Undervalued Stocks Based On Cash Flows In Switzerland

Name | Current Price | Fair Value (Est) | Discount (Est) |

Swissquote Group Holding (SWX:SQN) | CHF304.20 | CHF557.86 | 45.5% |

Georg Fischer (SWX:GF) | CHF55.50 | CHF108.11 | 48.7% |

lastminute.com (SWX:LMN) | CHF18.00 | CHF29.04 | 38% |

Julius Bär Gruppe (SWX:BAER) | CHF54.70 | CHF103.14 | 47% |

Komax Holding (SWX:KOMN) | CHF116.00 | CHF202.61 | 42.7% |

Clariant (SWX:CLN) | CHF12.35 | CHF21.37 | 42.2% |

Comet Holding (SWX:COTN) | CHF281.00 | CHF525.12 | 46.5% |

Dätwyler Holding (SWX:DAE) | CHF153.80 | CHF237.73 | 35.3% |

SGS (SWX:SGSN) | CHF97.40 | CHF150.84 | 35.4% |

Sensirion Holding (SWX:SENS) | CHF65.70 | CHF117.51 | 44.1% |

Here's a peek at a few of the choices from the screener.

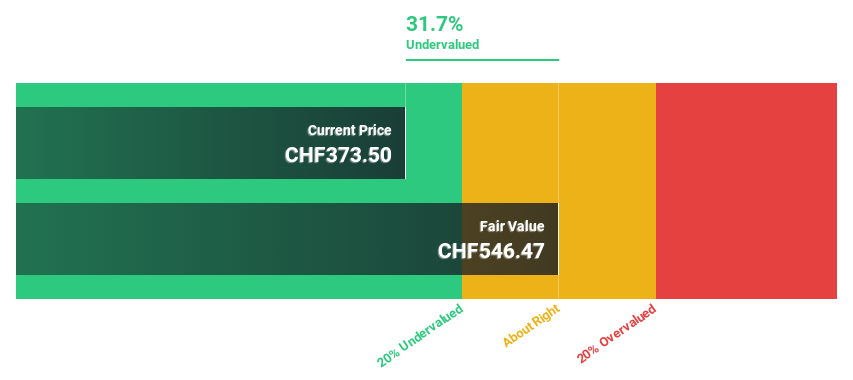

Comet Holding

Overview: Comet Holding AG, along with its subsidiaries, offers X-ray and radio frequency (RF) power technology solutions across Europe, North America, Asia, and globally, with a market cap of CHF2.18 billion.

Operations: The company's revenue segments include X-Ray Systems (IXS) at CHF115.34 million, Industrial X-Ray Modules (IXM) at CHF95.90 million, and Plasma Control Technologies (PCT) at CHF180.62 million.

Estimated Discount To Fair Value: 46.5%

Comet Holding is trading at CHF281, significantly below its estimated fair value of CHF525.12, indicating potential undervaluation based on cash flows. Despite a volatile share price recently, Comet's earnings are forecast to grow significantly at 47.8% annually over the next three years, outpacing the Swiss market's growth rate. The company reported improved net income for H1 2024 despite lower sales compared to last year, reflecting enhanced operational efficiency.

SGS

Overview: SGS SA offers inspection, testing, and verification services across Europe, Africa, the Middle East, the Americas, and the Asia Pacific with a market cap of CHF18.15 billion.

Operations: The company's revenue segments include Business Assurance, which generated CHF755 million.

Estimated Discount To Fair Value: 35.4%

SGS is trading at CHF97.4, well below its estimated fair value of CHF150.84, highlighting potential undervaluation based on cash flows. While the company's earnings and revenue are forecast to grow faster than the Swiss market, its high debt level and unsustainable dividend coverage pose concerns. Recent earnings show stable sales growth but a slight decline in net income for H1 2024, reflecting challenges in maintaining profitability amidst operational pressures.

Insights from our recent growth report point to a promising forecast for SGS' business outlook.

Click here and access our complete balance sheet health report to understand the dynamics of SGS.

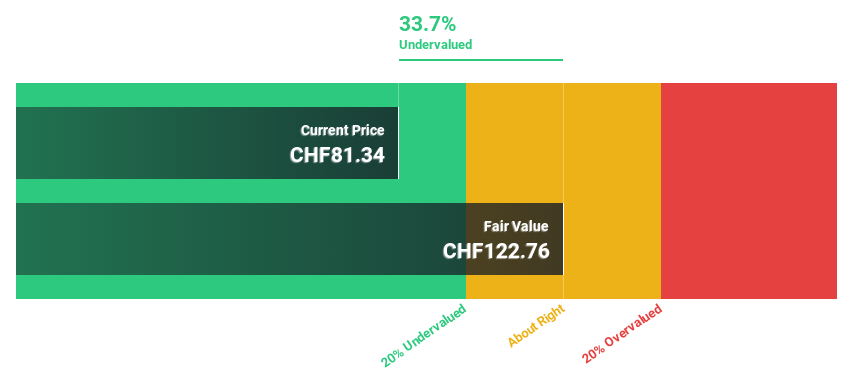

VAT Group

Overview: VAT Group AG, with a market cap of CHF11.06 billion, develops, manufactures, and supplies vacuum valves, multi-valve units, vacuum modules, and edge-welded metal bellows across Switzerland and internationally.

Operations: The company's revenue segments include Valves generating CHF783.51 million and Global Service contributing CHF163.83 million.

Estimated Discount To Fair Value: 28.9%

VAT Group, trading at CHF369, is significantly undervalued compared to its estimated fair value of CHF518.86. Despite recent volatility in share price, the company's earnings are expected to grow substantially at 22.6% annually, outpacing the Swiss market's growth rate. Recent financials show a rise in net income to CHF94 million for H1 2024 from CHF84.2 million last year, underscoring strong cash flow potential amidst steady revenue projections of 18.1% annual growth.

Summing It All Up

Unlock our comprehensive list of 17 Undervalued SIX Swiss Exchange Stocks Based On Cash Flows by clicking here.

Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SWX:COTN SWX:SGSN and SWX:VACN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com