3 ASX Value Stock Picks That Could Be Undervalued

The Australian market has experienced a mixed trading day, with the ASX200 closing slightly down by 0.1% at 8,214 points amid concerns about a slowing US economy and fluctuating commodity prices. As investors navigate this period of uncertainty, identifying undervalued stocks becomes crucial for those looking to potentially capitalize on long-term growth opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

Name | Current Price | Fair Value (Est) | Discount (Est) |

Data#3 (ASX:DTL) | A$7.46 | A$13.46 | 44.6% |

Mader Group (ASX:MAD) | A$5.53 | A$10.42 | 46.9% |

MLG Oz (ASX:MLG) | A$0.635 | A$1.15 | 45% |

Ingenia Communities Group (ASX:INA) | A$4.98 | A$9.43 | 47.2% |

Treasury Wine Estates (ASX:TWE) | A$12.11 | A$24.19 | 49.9% |

Little Green Pharma (ASX:LGP) | A$0.085 | A$0.17 | 49.8% |

Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

IDP Education (ASX:IEL) | A$14.87 | A$27.65 | 46.2% |

Superloop (ASX:SLC) | A$1.74 | A$3.31 | 47.5% |

Mineral Resources (ASX:MIN) | A$50.94 | A$95.61 | 46.7% |

Let's explore several standout options from the results in the screener.

Duratec

Overview: Duratec Limited, along with its subsidiaries, provides assessment, protection, remediation, and refurbishment services for steel and concrete infrastructure in Australia and has a market cap of A$395.71 million.

Operations: The company's revenue segments include Energy (A$46.64 million), Defence (A$220.16 million), Buildings & Facades (A$111.33 million), and Mining & Industrial (A$155.64 million).

Estimated Discount To Fair Value: 33.3%

Duratec is trading at A$1.59, significantly below its estimated fair value of A$2.38, indicating it may be undervalued based on cash flows. The company has demonstrated strong earnings growth of 24.8% annually over the past five years and forecasts suggest continued earnings growth of 13.18% per year, outpacing the Australian market average. Recent inclusion in the S&P Global BMI Index and solid revenue guidance for fiscal 2025 further support its growth potential.

Lynas Rare Earths

Overview: Lynas Rare Earths Limited, with a market cap of A$7.24 billion, is involved in the exploration, development, mining, extraction, and processing of rare earth minerals in Australia and Malaysia.

Operations: The company's revenue is primarily generated from its Rare Earth Operations, amounting to A$463.29 million.

Estimated Discount To Fair Value: 41.5%

Lynas Rare Earths, trading at A$7.75, is valued significantly below its estimated fair value of A$13.24, reflecting potential undervaluation based on cash flows. Despite a decline in production and sales volumes, the company's revenue growth is expected to outpace the Australian market at 27.3% annually. Earnings are forecast to grow considerably by 40.7% per year over the next three years, though recent financial results show reduced profit margins and net income compared to last year.

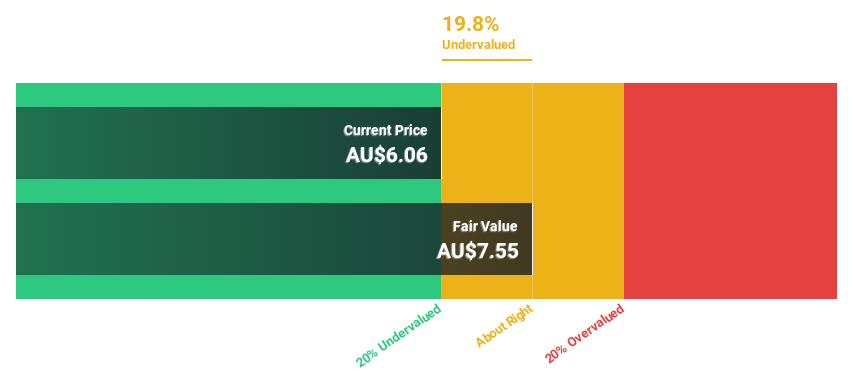

Treasury Wine Estates

Overview: Treasury Wine Estates Limited is a wine company with operations in Australia, the United States, the United Kingdom, and internationally, and has a market cap of A$9.83 billion.

Operations: The company's revenue is derived from three main segments: Penfolds at A$1.03 billion, Treasury Americas at A$1.03 billion, and Treasury Premium Brands at A$739.80 million.

Estimated Discount To Fair Value: 49.9%

Treasury Wine Estates, trading at A$12.11, is significantly undervalued with an estimated fair value of A$24.19. Despite a drop in net income to A$98.9 million from A$254.5 million last year, earnings are projected to grow substantially at 27.4% annually over the next three years, outpacing the Australian market's expected growth rate of 12.2%. However, profit margins have decreased and dividends remain inadequately covered by earnings or free cash flows.

Delve into the full analysis health report here for a deeper understanding of Treasury Wine Estates.

Make It Happen

Get an in-depth perspective on all 45 Undervalued ASX Stocks Based On Cash Flows by using our screener here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:DUR ASX:LYC and ASX:TWE.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com