1 Incredibly Cheap Cloud Computing Stock to Buy Before It Soars Higher

This has been a forgettable year for DigitalOcean Holdings (NYSE: DOCN) investors so far, as shares of the cloud computing specialist are down 7%. Yet, its latest quarterly report has injected some life into the stock.

DigitalOcean, which provides on-demand cloud infrastructure and tools to small businesses and start-ups, reported second-quarter 2024 results on Aug. 8. The stock shot up 14% following the announcement, as its top and bottom lines easily surpassed Wall Street's expectations.

Let's take a closer look at the company's recent quarterly performance and why it may be a good idea to buy DigitalOcean stock while it remains beaten down.

DigitalOcean's growth is likely to improve

DigitalOcean's Q2 revenue increased 13% year over year to $192 million, beating the consensus estimate of $188.6 million. Its adjusted earnings increased 9% from the same period last year to $0.48 per share, which was again higher than the consensus estimate, $0.39 per share.

What's more, DigitalOcean has raised its full-year guidance. It is now expecting revenue to land between $770 million and $775 million in 2024, up from an earlier range of $760 million to $775 million. The midpoint of the updated revenue guidance range indicates that the company's revenue could jump just over 11%. Also, DigitalOcean is now expecting adjusted earnings of $1.65 per share in 2024, up from earlier guidance of $1.635 per share. That would translate into a small jump of 4% from 2023 levels.

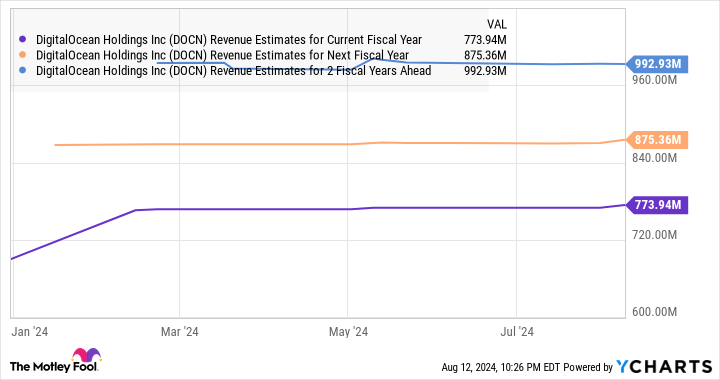

Now, the top- and bottom-line growth that DigitalOcean is forecasting for this year may not seem very attractive at first. However, investors would do well to note that the company's growth could accelerate thanks to a lucrative addressable market and an increase in customer spending.

DigitalOcean estimates that cloud spending by individuals and companies with fewer than 500 employees could jump from $114 billion this year to $213 billion in 2027, a compound annual growth rate of 23%. The company has experienced some headwinds of late thanks to a challenging macro environment, but it has managed to increase its customer base despite them.

For instance, DigitalOcean finished the previous quarter with 638,000 customers, up from 616,000 customers in the same period last year. More importantly, the average revenue per user increased 9% year over year to $99.45. This combination of a stronger customer base and an increase in revenue from each customer explains why DigitalOcean finished the previous quarter with an annual revenue run rate (ARR) of $781 million, a jump of 15% from the year-ago period.

DigitalOcean calculates its ARR "at a point in time by multiplying the revenue of the last month of the reported period by 12." So the stronger growth in this metric compared to the revenue growth it clocked last quarter suggests that the jump in customer base and spending could eventually lead to stronger growth.

It is also worth noting that DigitalOcean's ARR from artificial intelligence (AI)-related cloud offerings increased an impressive 200% year over year. This is another potential growth driver for the company, as the demand for AI solutions in the cloud is forecast to increase at an annual growth rate of 31% through the end of the decade.

DigitalOcean is offering cloud instances powered by popular chips such as Nvidia's H100 graphics processing unit (GPU), so it's not surprising that it is witnessing "very strong demand for our AI platform," as small businesses are looking to integrate this fast-growing technology into their operations. The immense opportunity in the cloud AI market could help accelerate DigitalOcean's growth and is probably one of the reasons analysts have increased their revenue growth expectations for the company.

DOCN Revenue Estimates for Current Fiscal Year data by YCharts

Its valuation makes the stock a solid buy right now

DigitalOcean is trading at just 4.3 times sales right now. Its forward earnings multiple stands at just under 20. Those multiples make the stock cheap compared to the U.S. technology sector's price-to-earnings ratio of 42 and sales multiple of 7.

Given that the company's growth is likely to get better, investors looking to add an attractively valued potential growth stock to their portfolios would do well to buy DigitalOcean before it could potentially jump higher following its latest quarterly results.

Should you invest $1,000 in DigitalOcean right now?

Before you buy stock in DigitalOcean, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DigitalOcean wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $763,374!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends DigitalOcean and Nvidia. The Motley Fool has a disclosure policy.

1 Incredibly Cheap Cloud Computing Stock to Buy Before It Soars Higher was originally published by The Motley Fool